A rod instead of a liquidity feast?…Fed warned of 'shadow banking' risk [Bin Nansae's No-Gaps Wall Street]

Summary

- The U.S. central bank (Fed) officially warned about excessive credit expansion and leverage risks in nonbank financial institutions (shadow banking), including private credit and hedge funds.

- Recent market unease linked to dollar liquidity shortages, high leverage, and distressed loans has dampened risk asset appetite, including bitcoin, and some private credit portfolios have shown actual poor performance.

- The Fed is expected to lean toward regulatory stances rather than accommodative policies like quantitative easing (QE) to maintain financial stability, so investors should temper expectations for more liquidity and leverage expansion.

Over the past week, the U.S. stock market was the epitome of volatility that trapped both bulls and bears. In the never-ending AI bubble narrative, there were Nvidia's earnings, the first official employment data release since the longest U.S. federal government shutdown in history, and the largest-ever November options expiration (options expiry) of $3.1 trillion. Markets sensitive to liquidity conditions and investor sentiment swung wildly.

In particular, on the 20th (local time), the day after Nvidia's "earnings surprise," the S&P 500, which had opened up more than 1.5%, finished the day down more than 1.5%. According to Bespoke Investment Group, aside from that day, the S&P 500 has shown that degree of one-day volatility on only three other occasions in history: April 8 (mutual tariffs day) this year, and October 7 and 9 during the 2008 financial crisis.

Behind such sharp volatility is a structurally worsening shortage of dollar liquidity. The cryptocurrency market, which is most sensitive to liquidity and investor sentiment, had already reversed into a decline before U.S. markets opened on the 20th. The crypto market still bears the scars of the massive liquidation event on October 10 and has been hit directly by institutions' deleveraging amid the recent dollar liquidity shortage. As a result, Bitcoin at one point slid into the $80,000s, further weakening risk asset appetite. (※Related article: The AI bubble is an excuse?...The real reason for the recent weakness in stocks and crypto)

In this context, markets have been waiting for the U.S. central bank (the Fed) to ease the liquidity shortage. A single comment from Fed officials has swung the probability of a December rate cut and caused wild moves in risk asset prices.

On the 20th, Fed Governor Lisa Cook and Cleveland Fed President Beth Hammack expressed concern about high asset valuations and the excessive credit expansion and leverage in the nonbank sector represented by private credit and hedge funds, prompting a sell-off in risk assets on worries about a "hawkish Fed." The very next day, however, John Williams, the New York Fed president and de facto number two at the Fed, said "there is room for rate cuts in the short term," a dovish remark that provided a catalyst for a rebound in risk assets.

Could private credit be the epicenter of the next financial crisis?

Frankly, market fickleness is hard to predict or even keep up with. Attempts to explain price movements caused by countless variables, imperfect investor psychology, and algorithmic trading are often post hoc rationalizations. Nonetheless, asking "why the market is like this" and seeking reasons is necessary to sift through noise and identify real variables, structural risks, and signals that will continue to affect markets.

Among the noise last week, the expansion of the nonbank sector — private credit, hedge funds, etc. — that the Fed has begun to focus on, namely the shadow banking risk, may be one of those "real variables." The warning voices are growing because, even if not immediate, these could become vulnerabilities capable of threatening the financial system.

Nonbank risks shook markets once last month. When subprime auto lender Tricolor and auto parts maker First Brands filed for bankruptcy in quick succession, U.S. regional banks and even JPMorgan suffered losses, sparking a market plunge over fears of more failures. At that time, JPMorgan CEO Jamie Dimon said, "I've seen a few more cases like First Brands, which raised funds heavily through private credit and then failed. If you saw one cockroach, there are likely more," heightening market caution. More recently, Jeffrey Gundlach, CEO of DoubleLine Capital and the so-called 'new bond king,' labeled private credit "junk loans" and warned, "the next financial crisis will originate in private credit."

The Fed has joined these concerns. On the 19th, Lisa Cook, who chairs the Fed's Financial Stability Committee, identified △ the rapid expansion of private credit and △ the surge in Treasury trading by leverage-based hedge funds as structural threats to financial stability. Cook pointed out that private credit has roughly doubled in size over the past five years and called it a "potential vulnerability to watch going forward." While she said it did not look likely to cause an unexpected credit squeeze similar to the asset-backed commercial paper (CP) market that helped trigger the 2008 crisis, she warned it should be closely monitored.

Fed paying attention to private credit risk

On the same day, Cleveland Fed President Beth Hammack issued a stronger-toned warning about the private credit market. While saying "the overall financial system is broadly sound," she named private credit as the top financial stability risk to watch going forward.

Commenting on a series of recent bankruptcies among companies linked to private credit, she warned that "considering a structural environment where low rates and abundant credit pushed investors to seek higher returns, it is difficult to call these isolated cases," and said, "the riskiest loans tend to be revealed at the end of credit cycles." She went further to say, "further rate cuts in the current accommodative financial conditions could encourage risk-taking," arguing for caution on rate cuts to preserve financial stability.

Such concerns are increasingly felt across the Fed. The October FOMC minutes released on the 18th show this. An analysis of FOMC minutes from March to October this year shows mentions of private credit rose from 0 in March → 1 in May → 1 in June → 2 in July → 1 in September → 6 in October. The tone changed sharply.

In May there was a sentence noting that "some participants mentioned concerns about hedge funds' high leverage and private credit and equity markets," but it also concluded that "overall credit performance remained stable." By the October meeting, however, phrasing pointing to private credit risks had increased markedly.

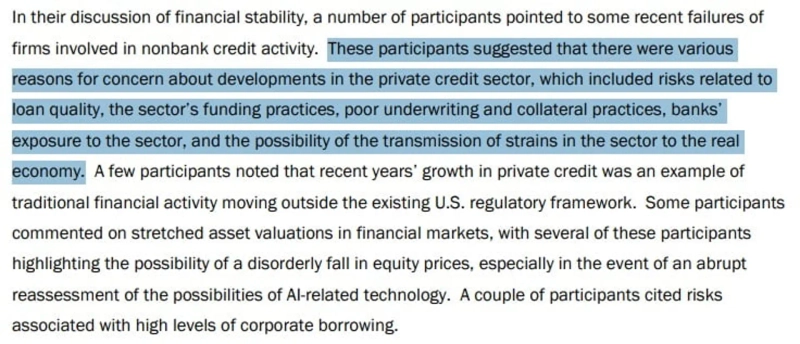

Notably, the minutes included lines such as "borrowers in private credit are frequently using payment-in-kind (PIK) (paying interest in assets like bonds/equities instead of cash)," "although the rapid growth of private credit has somewhat eased, recent bankruptcies have increased concerns about credit quality and hidden leverage in this market," and "several participants expressed concerns about loan quality, funding practices, weak underwriting/collateral practices, banks' exposures, and the possibility that stress in the nonbank sector could spill over into the real economy."

What is the private credit market like?

Private credit refers to lending conducted through nonbank financial firms such as investment companies, asset managers, and private equity firms. This market surged after the 2008 financial crisis as stringent bank regulations reduced bank lending, leaving a gap that private credit filled. Positively, it supplies credit to startups and unlisted companies that can't meet banks' high lending thresholds, and it helps match maturities between institutions with long-term capital (pension funds, insurers) and unlisted companies needing long-term financing.

But because it is "private," it has lower transparency and fewer regulations compared to banks. This is why the nonbank market is called shadow banking. Private credit investments lack transparent information and external price discovery, making risk assessment difficult. When things are good, there may be no visible problems, but once distress is exposed, these areas can quickly become problematic. Gundlach warned that "private credit prices are either zero or 100," adding "you might think it's safe because you can sell anytime, but that's not true. When you want to sell amid trouble, prices will be falling every day."

Institutions likely understand these risks when they invest. The question is whether nonbank risks can spread into a financial crisis. Here the Fed is worried that the rapid growth of private credit has increased the likelihood that vulnerabilities will transmit into the banking system and the real economy. Banks like JPMorgan have already taken losses from loan defaults originating in the nonbank sector.

So far the scale has been small. The problem is that if the economy slows and defaults rise, it is unclear how far the damage could spread. As the Fed noted, a high share of PIK in private credit may look healthy on the books but could indicate many loans that are not truly sound.

In practice, Wall Street has recently been abuzz that BlackRock waived management fees after poor performance in its private credit portfolio. That portfolio included a large number of bad loans tied to recently bankrupt companies like Renovo Home Partners and Astra Acquisition. Until a few weeks ago BlackRock had valued its loan to Renovo at par (100%), but it recently wrote it down to zero (0). It unfolded just as Gundlach warned.

Of course, not all private credit is problematic. There is intense debate about whether private credit is risky enough to trigger a systemic crisis. Still, many worry we are entering a late-credit-cycle phase where leverage has increased, loan quality has deteriorated, and narrow credit spreads combined with a hunt for yield lead to looser lending standards — a vicious cycle that raises vulnerability to shocks.

The recent rise in loans to finance astronomical AI infrastructure investment is another factor increasing the burden. Blue Owl, a leading private credit player, is also a partner in financing Meta's large data center investments.

Will the Fed curb hedge fund leverage?

Another major nonbank actor is hedge funds. Central banks worldwide, including the Fed, the Bank of Japan, and the Bank of England, are wary that hedge funds, which employ massive leverage, are gaining influence across markets for Treasuries, currencies, and equities.

Hedge funds engage in basis trades in the Treasury market, exploiting tiny price differences between cash and futures. Although differences can be as small as 0.01%, they use enormous leverage to multiply returns. In normal times they supply liquidity, but under stress their high leverage can force liquidations that cause Treasury price crashes and further liquidity shortages, creating a vicious feedback loop. In particular, as hedge funds increasingly borrow in the repo market to finance leveraged positions, recent repo rate increases have contributed to short-term funding market strains.

To address these issues, the Fed discussed at the October FOMC introducing a central clearing function into its standing repo facility (SRF). The SRF is an emergency lending window where financial institutions can temporarily borrow from the Fed using U.S. Treasuries as collateral when they need cash urgently.

With a central clearinghouse, nonbank institutions like hedge funds or money market funds (MMFs) could indirectly borrow liquidity from the Fed through dealers. However, under central clearing rules, participants must post margin daily. Positions with higher leverage, especially during volatile market conditions, require more margin. This would be unfavorable to highly leveraged hedge funds engaging in basis trades or carry trades. In short, the Fed's intent appears to be to ease the use of the SRF to relieve short-term funding market stress while placing margin discipline to prevent nonbank financial institutions from engaging in unfettered "debt parties."

Fed vs. Wall Street: "What has to break for you to act?"

These developments have dampened Wall Street's hopes for a Fed-led "liquidity party." Some highly leveraged institutional investors, who suffered from recent short-term liquidity shortages, had hoped the Fed would not only cut rates in December but also accelerate the end date for quantitative tightening (QT) scheduled to end on December 1, or even start quantitative easing (QE).

But a Fed emphasizing financial stability and shadow banking risks does not seem inclined to hurriedly provide such accommodative measures. Assessing the risks in the nonbank sector is necessary for financial system stability. Nevertheless, Wall Street and investors who favor more liquidity, leverage, and higher returns are dissatisfied with this Fed stance.

Goldman Sachs analyzed on the 16th that "Fed policy shifts have historically occurred only after market stress accumulates and erupts to a certain level," noting that the market, where risk asset sentiment is depressed, is asking, "what exactly has to break for the Fed to act?"

New York = Correspondent Bin Nansae binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.