War risk becomes a ‘toll’… ‘risk insurance premiums’ drive up global logistics costs [Global Money X-File]

Summary

- It reported that geopolitical risk has entrenched the war risk premium (AWRP) at more than six times the peacetime level, acting like a constant toll on global logistics costs.

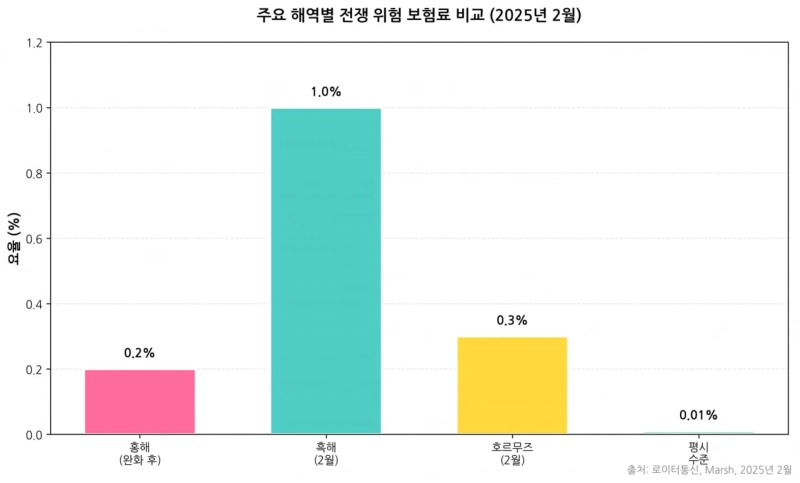

- It said that despite easing in the Red Sea, risks in the Black Sea and the Strait of Hormuz have driven premiums up to around 1.0% of vessel value, undermining the price competitiveness of Ukrainian corn, Russian crude, and oil prices.

- It reported that while high premiums and Red Sea detours have helped South Korean shipping companies and the shipbuilding industry defend earnings and provided tailwinds, export manufacturers are seeing weaker price competitiveness as logistics costs and surcharges (WRS) rise.

Forecast Trend Report by Period

Geopolitical risk in global trade has recently been pushing up logistics costs. That is because what used to be a variable cost—“war and marine risk insurance premiums”—has become entrenched as a structural expense.

Additional marine insurance premiums on rebel risk

According to Reuters and others on the 5th, the risk posed by Yemen’s Houthi rebels, which threatened the Red Sea in 2024–2025, has shown signs of easing somewhat this year. As ceasefire talks and multinational naval escort operations have taken hold, the Additional War Risk Premium (AWRP), which at one point exceeded 1% of a vessel’s value, fell to around 0.2%.

However, that is still more than six times higher than the pre-crisis peacetime rate (0.03%). The risk has come down to a manageable level, but the cost has not returned to the past. An “additional war risk premium” of 0.2% means a weekly cost of $200,000 for a $100 million vessel. It has become a permanent “toll” attached to all cargo transiting the Suez Canal.

Global marine insurance premiums are largely set in private insurance markets in London and Bermuda. They cannot be rolled back by treaty or administrative order. Even after physical threats fade, premiums tend to display “downward rigidity,” sustained by market fear and the instinct to preserve capital. Freight rates often show resilience, returning to normal tracks relatively quickly after a market shock. War risk premiums, by contrast, rarely come down once they rise.

Marine insurance is often viewed as a negligible fee tacked onto each container. But in a geopolitical crisis, war risk insurance can become a cost driver that overwhelms freight rates themselves in both scale and the way it is levied. The key reason it acts much like a tariff is that it is not calculated based on cargo weight or volume. Instead, it is based on the vessel’s asset value. Regardless of cargo volume, newer and more expensive ships pay more.

The charge is levied not for an entire voyage but in base units tied to time spent in a risk zone (typically seven days). If port congestion or the threat of attack keeps a ship in a risk area for eight days, the owner must immediately pay a second seven-day premium.

For example, suppose a modern LNG carrier valued at $200 million transits a high-risk zone near the Black Sea or Hormuz in February. If the rate is 1.0%, a bill of $2 million (about KRW 2.7 billion) would be charged for just seven days of “toll.” That amount far exceeds the vessel’s daily operating costs by dozens of times. A substantial share of freight revenue is eaten up—or passed straight on to shippers.

Who pays war risk premiums

In practice, however, shipowners do not usually bear the cost in the end. The shipping market’s contract structure is designed so the cost is immediately and mechanically passed on to cargo owners. In spot charter contracts, the AWRP (additional war risk premium) is typically borne by the charterer. This is reflected at once in shippers’ effective costs regardless of declines in freight indices. Even if shippers negotiate lower freight rates, they cannot avoid a separate insurance bill. Container carriers charge shippers under the label “war risk surcharge.”

Another view is that global maritime risk hotspots have shifted. As threats in the Red Sea ease, the Black Sea is heating up again. Last month, drone attacks between Russia and Ukraine directly targeted merchant vessels and port infrastructure, sending premiums sharply higher. Port-call premiums for the Black Sea, which were around 0.6–0.8% late last year, jumped to as high as 1.0% of vessel value last month.

As Greek-flagged tankers became targets of drone attacks, risk ratings for energy transport ships—previously considered relatively safe—were revised upward. The Black Sea is a major gateway for global grain and energy. An insurance premium of 1% of vessel value can seriously erode the export price competitiveness of Ukrainian corn or Russian crude.

The most worrying flashpoint is rising tensions in the Strait of Hormuz, through which 20% of the world’s crude flows. Recently, Iranian small craft approached a U.S.-flagged tanker. Premiums are said not to have surged to Black Sea levels (1%) yet. But the market has already priced in a “war warning” premium. Citigroup assessed that Iran-related geopolitical risk could add a $7–$10-per-barrel premium to oil prices.

Even as freight rates fall, premiums stay put

For the industry, another burden is that insurance premiums are less volatile than freight rates. This year’s shipping market shows container spot rates stabilizing lower amid excess capacity. Yet premiums have barely moved. Typically, when a major incident occurs, insurers raise rates sharply to recoup capital losses. They do not, however, cut rates immediately just because incidents subside. They keep rates elevated, citing uncertainty that “attacks could resume at any time.”

Primary insurers pass the risk on to reinsurers. Reinsurance contracts are typically annual. If losses last year lead to higher 2026 reinsurance rates, primary insurers have little choice but to maintain high premiums throughout this year even if no accidents occur on the ground. This structural lag makes premiums respond far more slowly than the pace of recovery in the real economy.

S&P Global data analyzing transport costs for LR1 tankers (65,000-ton class) from the Middle East to Europe found stretches where the Red Sea route—though physically shorter than the Cape of Good Hope detour—was assessed as more expensive or similar in cost. Via the Red Sea, the cost was $52.31 per ton; via the Cape of Good Hope detour, $50.77 per ton. The reason the shorter route is more expensive is “insurance.”

For South Korean shipping companies, this “invisible tariff” is paradoxically acting as a buffer for earnings. The Cape detour prompted by Red Sea risk (longer sailing distances) has absorbed capacity, reportedly preventing a sharper drop in freight rates. It may also be favorable for shipbuilders: the higher the risk, the more shippers prefer newer vessels that are faster, safer, and eligible for insurance discounts, rather than old and slow ships.

For export manufacturers, however, it is a cost burden. Various surcharges (WRS) embedded in logistics costs to Europe could erode the price competitiveness of Korean products. The lower the share of local production in Eastern Europe for a given product category, the larger the hit from these marine insurance premiums.

Reporter Kim Joo-wan kjwan@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.