"The index is calm—so why only me?"…Why perceived volatility has become extreme [Bin Nan-sae’s Wall Street Without Gaps]

Summary

- It said that as algorithm-driven funds and the spread of CTA, vol control, leveraged ETFs and 0DTE options expand, indices look stable while volatility in individual stocks has widened to extremes.

- It said that multi-strategy funds and market-neutral approaches, along with reduced share buybacks, have weakened downside shock absorbers for the indices, structurally making sharp swings across individual stocks and sectors more frequent.

- It said that in the recent tape, with momentum, flows and positioning driving short-term prices, opportunities could open up in themes such as memory semiconductors, data-center infrastructure, power equipment, metals and mining companies, and undervalued value stocks.

Forecast Trend Report by Period

The headline index looks calm

But individual stocks and sectors are on a roller coaster

Algorithms, hedge funds, leveraged ETFs, etc.

Flows and momentum—not fundamentals—are driving prices

The ‘safety valve’ of buybacks is weakening

The U.S. stock market these days really feels like a roller coaster. Repeated sharp sell-offs and rebounds led by tech stocks have pushed perceived volatility to extremes. It has become commonplace for mega-cap giants such as Amazon, Oracle and Microsoft to swing by around 10% in a single day, with sector-by-sector winners and losers diverging starkly session after session.

But the picture looks a bit different if you focus only on the major indices. As sectors whip back and forth, the S&P 500 has still held up, remaining up 1.2% year to date, while the Dow has been notching fresh record highs day after day. The volatility index (VIX), often dubbed the “fear gauge,” also stayed well below its long-run average even on the 10th (local time), when the S&P 500 closed down a modest 0.3%. For many retail investors with heavy allocations to tech, it is an easy market in which to complain: “The index is quiet, but only my stocks are getting tossed around.”

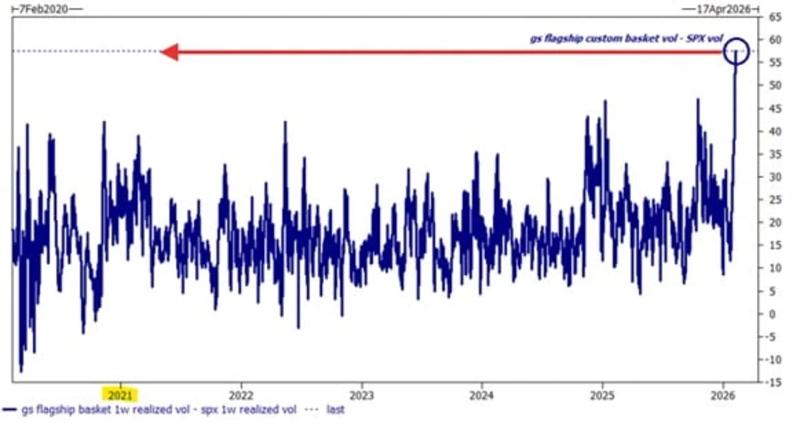

In fact, according to Goldman Sachs, realized volatility over the past week for its flagship large-cap basket jumped to 80, the highest level since the tariff announcement in April last year. By contrast, realized volatility for the S&P 500 index was just 20. In other words, war-like volatility was unfolding at the single-stock and theme level, while the index itself remained relatively subdued.

In the past, when equities sold off sharply, the broader market tended to cascade in the same direction. But now the market’s operating regime has changed: correlations across sectors have fallen, while volatility in individual names has been amplified. Even without major shifts in the market’s underlying fundamentals, mechanical forces beneath the surface are making investors’ felt volatility greater.

Charlie McElligott, Nomura Securities’ cross-asset macro strategist, says it is the combined effect of algorithm-driven funds and hedge funds that fuel trends (momentum), an options market increasingly optimized for short-term trading, and leveraged ETFs.

The algorithmic backlash that feeds on momentum

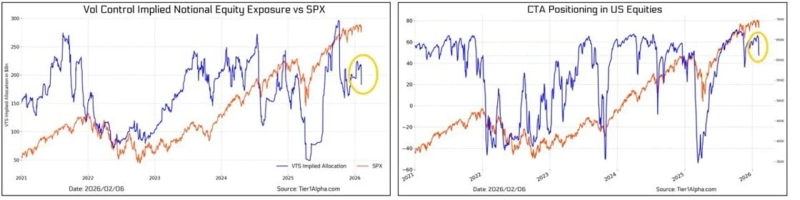

The first factor amplifying single-name volatility is algorithmic funds. These funds move according to trend-following strategies (CTAs) and strategies that automatically adjust leverage based on volatility (volatility control), executing systematic trades down to the second. That is, they buy and sell mechanically based on price volatility and momentum, regardless of fundamentals.

Such systematic strategies add exposure as trends strengthen, and mechanically cut leverage as volatility rises. When a downturn begins, they automatically dump risk faster, creating a “self-reinforcing” structure that deepens the drawdown.

McElligott explains: “As more funds adopt these strategies, the market structure is shifting into one that ‘lives off momentum.’” That is, flows and trend, rather than fundamentals, increasingly determine the market’s direction and speed.

These algorithmic funds also played a role in the recent sell-off. During the low-volatility regime, they accumulated large positions in momentum themes, and those positions grew so extreme that there was little incremental buying power left. McElligott says that just before the plunge began, Nomura’s internal quant exposure was at the 99.7th percentile versus five years of data. By Goldman Sachs’ hedge-fund dataset as well, it reached the 100th percentile over the past five years.

McElligott said: “When signs appear that it’s ‘now at an absurd level,’ money starts to leave, and algorithms that judge the trend has broken begin to unwind positions all at once,” adding that “from that point, the unwind becomes non-linear—like a waterfall.” Recently, fears that “AI will eat software” triggered profit-taking in tech and then served as the trigger for a trend reversal.

This is also why Goldman Sachs and Bank of America have warned that “CTA selling is still left” and that “short-term volatility will likely persist for a while,” despite the recent rebound. Tier1Alpha likewise cautioned that “vol-control funds have shifted into a structure that requires net equity selling after the rebound on the 6th,” adding that “we still need to be on guard for sharp swings.”

The evolution of ‘market-neutral’ hedge funds

A shift in the hedge-fund mainstream strategy is another reason single-name volatility is larger than in the past. Until 10–15 years ago, the dominant approach was the traditional long/short fund. Based on managers’ views and discretionary judgment on specific industries and stocks, they often bought good companies (long) and sold bad ones (short), while keeping net market exposure positive.

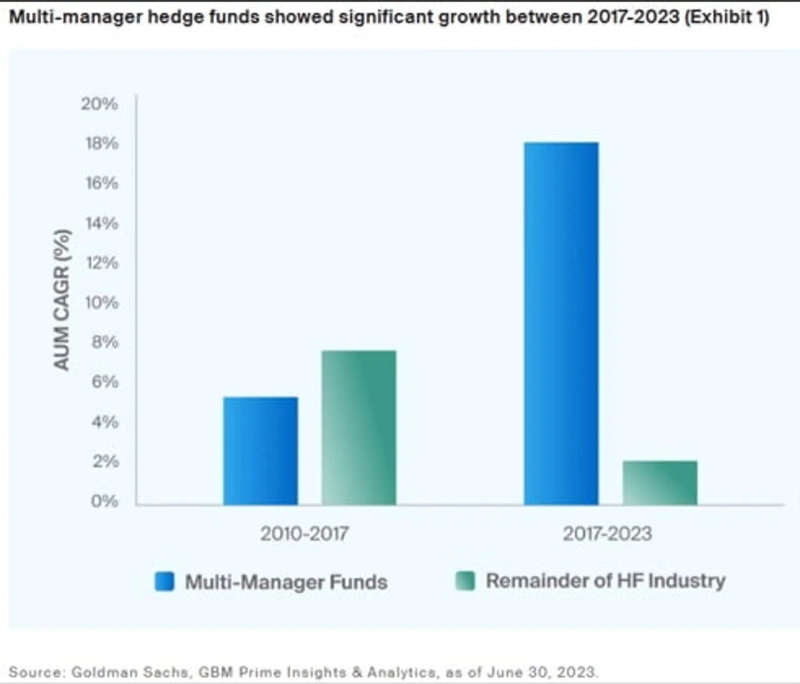

Today’s mainstream “multi-strategy funds” are different. These platform-style hedge funds run multiple strategies simultaneously within one fund—long/short, options trading, event-driven, and more. Rather than betting on market direction, they seek returns regardless of whether the market rises or falls, and are therefore also called “market-neutral” funds. According to McElligott, 80% of new money flowing into hedge funds over the past 5–10 years went into these multi-strategy funds.

They do not bet on market direction; to minimize volatility, they buy some stocks while shorting others to drive overall market exposure to “0.” Risk management is especially strict: even a 1–2% loss in a day can trigger mechanical liquidation. They sell the stocks they held and simultaneously buy back the stocks they had shorted. As a result, indices can look stable on the surface even as violent moves play out within individual stocks and themes.

McElligott says that whereas the past often saw broad risk-on and risk-off swings across all risky assets, it has become harder to see that pattern because market-neutral multi-strategy funds now dominate with overwhelming capital and leverage. This is also the backdrop to the recent, frequent tape in which tech collapses while previously neglected sectors such as energy, consumer staples and basic materials rally strongly.

Retail tools turning into volatility bombs

Leveraged ETFs and zero-day-to-expiry (0DTE, same-day expiration) options—favorites among retail investors—are also cited as factors amplifying single-stock volatility.

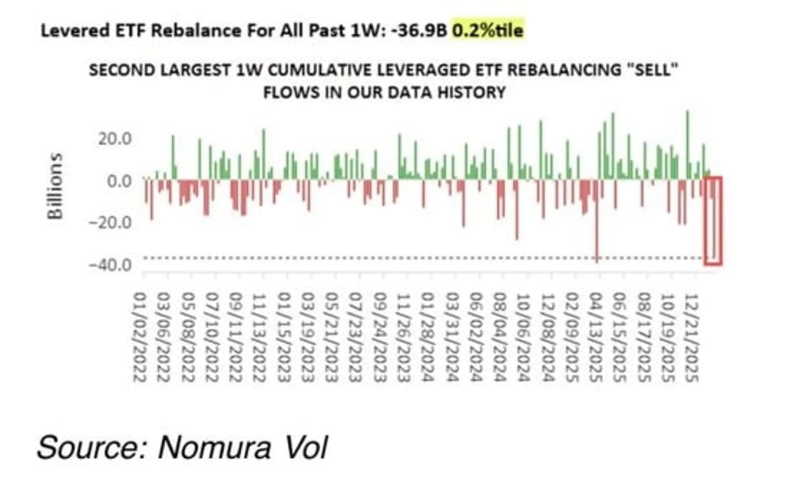

In particular, in down markets, leveraged ETFs can magnify declines in the underlying asset. That is because leveraged ETFs must rebalance each day to maintain their stated multiple at the close. For example, if the underlying stock falls 5%, a 2x leveraged ETF must sell more shares late in the session to reach -10%. Nomura Securities estimates that rebalancing by leveraged ETFs alone generated $369.0 billion of selling over the past week.

Same-day options are similar. When retail buys these options in size, dealers (market makers) who sold them must mechanically buy and sell the underlying stock to hedge risk. This can also amplify volatility in individual names by triggering mechanical dealer trading that forces them to “sell more” when the market falls.

These same-day options are becoming increasingly popular among U.S. retail investors and now account for more than half of total options trading. Exchanges, seeking more fee revenue, are continuing to expand the variety and expiration schedules of same-day options (once a week → three times a week). That means volatility bombs can go off more often.

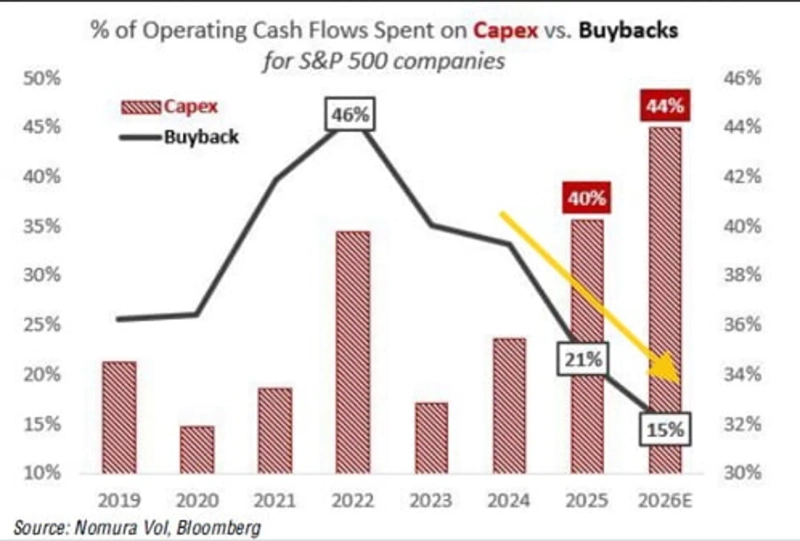

The weakening of the buyback ‘safety valve’

Share repurchases—once a safety valve in down markets—are also weakening. Over the past 15 years, U.S. corporate buybacks have been by far the largest source of bid and a suppressor of volatility.

But as the market enters an “AI arms race” phase, the capacity for buybacks is shrinking. Big Tech and large AI firms, which accounted for one-third of S&P 500 buybacks, have jumped into an astronomical capital-expenditure (CAPEX) race to secure AI leadership, pouring free cash into infrastructure investment rather than buybacks.

According to Nomura Securities, S&P 500 companies plan to allocate only 15% of operating cash flow to buybacks this year and spend 44% on capital expenditure. The share devoted to buybacks has continued to fall from 46% in 2022 and 21% in 2025.

Buybacks have supported the downside by having companies directly purchase shares whenever prices fall. As this shock absorber weakens, the market has become structurally more sensitive to downside shocks.

“What would Buffett buy?”

McElligott says the market’s “mean reversion” is no longer working well in the short term. As mechanical forces gain dominance, value investing’s principle of selling what is expensive and buying what is cheap based on fundamentals is becoming more difficult in the near term. That is because short-term prices have become driven by momentum, flows and positioning.

Ultimately, retail investors too are entering an era in which, when making short-term trades, they must stay more alert to flows, supply/demand dynamics and momentum. Especially when sector rotation and sharp swings repeat as they have lately, it is also necessary to check which stocks and themes are holding their trend without breaking down. Themes such as memory semiconductors, data-center infrastructure, power equipment, and metals and mining companies that found support even during the recent sell-off may offer clues.

Of course, from a long-term investing perspective, the principle of mean reversion should still hold. In particular, in the recent market in which capital crowded into AI growth stocks is dispersing into previously neglected sectors, bets on undervalued value stocks could be rewarded for the first time in years. On the 10th in New York as well, shares in previously overlooked areas such as REITs (real estate investment trusts), homebuilders and freight transportation rose further.

Goldman Sachs trader Brian Garrett said: “We’re at the beginning of a phase in which business models are being re-rated because of AI,” adding: “There are still opportunities in this market, but it feels like one of the first times in a very long while that you can look for them somewhere other than mega-cap tech.” In other words, “this is a market where you should ask: What would Warren Buffett buy right now?” The AI-led innovation and long-term investment narrative remains intact, but as stock-picking within AI names intensifies, it can be read as meaning that relatively more opportunities appear to lie in undervalued value stocks.

New York=Correspondent Bin Nan-sae binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.