"Scarier than the Iran war"… Wall Street gripped by fear of a $1.8 trillion time bomb [Bin Nansae’s Wall Street, No Gaps]

Summary

- Wall Street is said to view AI’s high valuations and the risk of distress in the $1.8 trillion private-credit market as a bigger threat than the Iran war variable.

- It said signs of outflows and structural fault lines are appearing in private-credit funds, highlighted by MFS’s bankruptcy and $3.8 billion of redemption requests at Blackstone’s BCRED.

- With UBS citing a possible 15% distress rate, weakening in credit markets and concerns about an AI bubble, some are discussing scenarios in which a private-credit crisis could hit AI investment and broader risk-asset markets if it becomes reality.

Forecast Trend Report by Period

After a punishing February, U.S. stocks are now confronting a major geopolitical risk: the Iran war. U.S. President Donald Trump has unnerved investors hoping for a quick end, saying of military operations against Iran, "I don't care how long it takes. We'll get it done no matter what."

Even so, U.S. equities are holding up better than the worry would suggest. On the 3rd (local time), the three major New York stock indexes all plunged more than 2% early in the session, but pared losses to close down around 1%. Some of the market has begun to price in concern that if the war drags on, a surge in energy prices could reignite inflation, disrupt the Federal Reserve’s rate-cut path and the growth trajectory, and tip into stagflation. That helps explain why the dollar jumped and risk-off sentiment spread while selling pressure in Treasuries eased (a smaller rise in Treasury yields).

Still, many participants are betting the Iran war won’t become prolonged. Citi said that given a more accommodative global monetary-policy backdrop than in past market crises, "a major risk-asset collapse right now is not our base case." UBS assessed, "The Iran situation is geopolitically significant, but given the current military response, the conflict is likely to be short-lived." In fact, Wall Street’s real worry lies elsewhere: the structural shift driven by AI, and the risk of distress in private credit.

Why did Trump strike Iran now?

First, Wall Street’s view that the Iran war won’t drag on. Behind Trump’s decision to hit Iran now, beyond the stated aim of eliminating nuclear and ballistic-missile threats, are several strategic calculations.

One is the achievement of being the president who "toppled Iran’s 37-year theocratic rule"—something previous U.S. presidents, including Barack Obama and Joe Biden, failed to do. According to the New York Post and The Atlantic, as Trump planned the operation he repeatedly told aides, "Only I can make this decision," and "It would be the greatest foreign-policy achievement—doing what previous presidents failed to do." Israeli Prime Minister Benjamin Netanyahu, who has wanted to draw the U.S. in to bring down the Iranian regime, played that angle well.

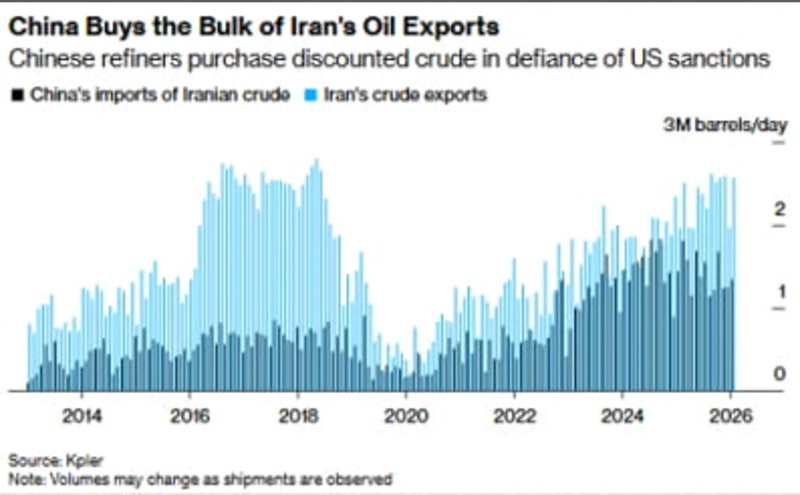

The bigger picture is the Trump administration’s strategy to isolate China and cement U.S. primacy. China has been buying about 1.6 million barrels a day of crude—around 15% of its total oil imports—from sanctions-hit Iran at bargain prices. By moving to remove pro-China regimes in Iran after Venezuela, the U.S. has disrupted two of China’s core crude supply lines in just two months.

If this military operation ultimately enables Washington to control supply of Iranian crude as well, China would lose a major source of cheap energy. That could hit an economy already suffering from a property slump and weak consumption. It also appears intended to pressure Beijing and strengthen U.S. leverage ahead of the U.S.-China summit scheduled for later this month.

Another factor is that the U.S. is now better positioned than in the past to absorb the oil-price risks of Middle East military action. After the shale revolution of the 2000s, the U.S. became the world’s largest oil producer, significantly reducing its dependence on Middle Eastern crude. Bloomberg commodities specialist Javier Blas said, "Even if an Iran operation increases turmoil in the Middle East, the likelihood of a repeat of the oil shocks the U.S. experienced in the past has fallen," adding that by securing Venezuelan crude as well, the U.S. has become relatively freer of oil-price risk—removing a major constraint on overseas military action.

"Ignore the Iran risk"

There are three main variables left: (1) whether this war turns into a prolonged conflict, (2) whether there is a material disruption to crude supply due to a closure of the Strait of Hormuz or strikes on energy infrastructure in the Middle East, and (3) how and how quickly any power vacuum inside Iran is resolved. The key is that if the war drags on, high oil prices could persist, reigniting inflation fears, forcing a repricing of rate-cut expectations and risk premia, and tightening liquidity in risk-asset markets.

For now, the market is betting it won’t turn into a long war. Above all, Trump’s political base ahead of the midterm elections doesn’t want that. Prominent economic historian Niall Ferguson predicted that, drawing lessons from the Iraq war, Trump would not spend more time and resources than needed for a short military operation. Ed Yardeni of Yardeni Research also argued it would remain short, without deploying ground forces.

Of course, it could last longer than the market’s optimism implies. But from a financial-market perspective, the key variable is ultimately energy prices. Because the U.S. now exerts greater direct and indirect price influence in the oil and natural-gas markets than in the past, upside in energy prices may be capped—potentially easing market anxiety. In fact, through the 3rd, Brent crude rose as much as 14% yet remained around mid-2024 levels, and European gas prices—up 40%—are still only about one-sixth of their 2022 peak.

Steve Eisman, who became one of the real-life models for the film 'The Big Short' after predicting the 2008 subprime-mortgage collapse and global financial crisis, said investors should ignore the U.S.-Iran war. Asked whether the conflict had prompted any portfolio changes, he flatly replied, "Not one." He said, "People reacted to the situation and oil jumped, but if things work out, it’ll be back to where it was in two months."

He added that "over the long term, (this decline) is very positive." If fundamentals haven’t changed, it could be a buying opportunity. Morgan Stanley CIO Michael Wilson likewise said, "Unless oil spikes to a historically meaningful level and stays there, the U.S. recovery cycle—and the bullish outlook for equities that comes with it—doesn’t change."

Historically, geopolitical conflicts have not had a lasting impact on equity markets. According to Barclays, after conflicts broke out since 1980, the S&P 500 fell 5–7% in the first 10 days, recovered to flat after a month, and rose 8–10% after 12 months.

"The real risk: $1.8 trillion private-credit jitters"

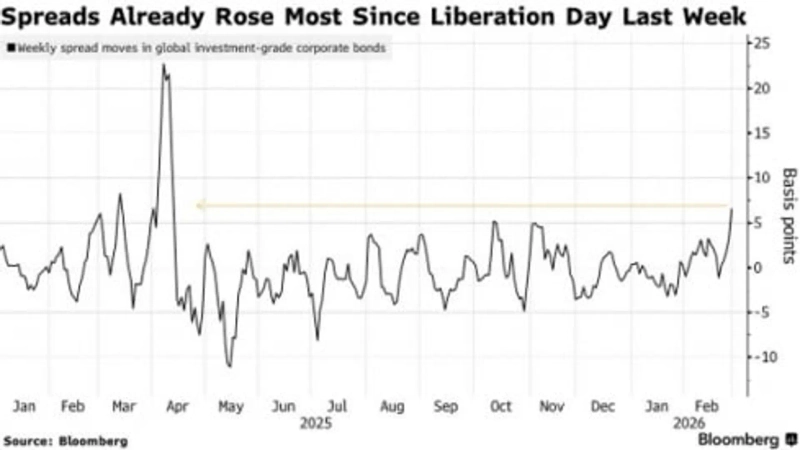

What Wall Street fears more than the Iran situation is the possibility of a private-credit-driven crisis festering beneath the surface. Citi said, "A more important question than Middle East risk is whether the AI valuation overhang that has built up recently and private-credit market anxiety will spread into broader asset markets." Citi added that "since early February, tech shares falling, credit concerns, and bond strength have occurred simultaneously, pushing rate volatility to the highest level in a year," arguing that bonds and rates—not equities—could become the market’s central variable.

In the private-credit market, a series of stress signals has been emerging. U.K. mortgage lender MFS, which had borrowed from Wall Street banks such as Wells Fargo and Jefferies, filed for bankruptcy leaving behind loans totaling £2.4 billion (₩4.2 trillion) amid allegations of double-collateral fraud. It resembles last October’s market-rattling collapses of subprime auto lender Tricolor and auto-parts maker First Brands. Jamie Dimon’s remark—"If you see one cockroach, there are probably more"—appears to be playing out.

Even private-credit funds run by major private-market players such as Blue Owl, KKR and Ares have faced an unbroken stream of dividend cuts tied to loan losses, markdowns in asset values and large redemption demands. On the day, reports said Blackstone’s private-credit fund BCRED moved to meet $3.8 billion of redemption requests—equivalent to 7.9% of total assets—by having employees step in to purchase assets. It is a sign that outflows and structural fault lines may be increasing across the private-credit market.

Private credit—where private funds lend directly to companies like banks and collect high interest—differs from publicly traded stocks or listed corporate bonds in that it lacks real-time market pricing and is not externally marked. In the era of ultra-low rates and abundant liquidity, there was little chance for problems to surface, and returns were strong. As money poured in from institutions as well as insurers and individuals, the market rapidly expanded to $1.8 trillion.

But weaknesses are now starting to show: a liquidity-mismatch structure (making long-term loans while allowing investors periodic redemptions) and limited transparency and market trust. With rates higher and shares of software companies—major borrowers from private funds—slumping amid an "AI doomsday" narrative, a pileup of negatives has followed: falling asset values, rising loan stress, and slower inflows of new capital.

Crisis-level impairment risk vs. exaggerated fears

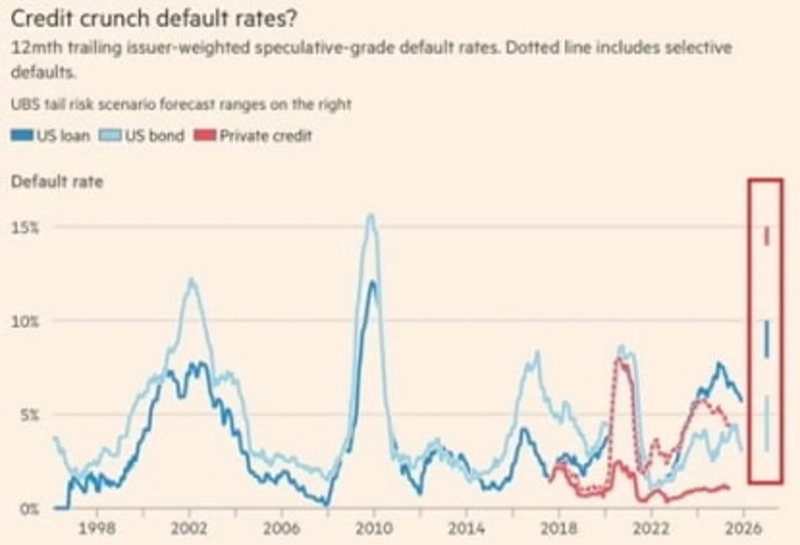

UBS estimates that in a worst-case scenario, private-credit distress rates could jump to 15%, the highest since the global financial crisis. Eisman said, "I don’t know if that number is realistic, but if it happens, it would be catastrophic." That’s because the market is now supported not only by institutional investors but also by policyholder funds, retail investor money and retirement plans (401(k)s), meaning impairments could hit the broader U.S. economy. Last year, President Trump signed an executive order easing rules to allow private credit and private equity (PE) to be included in retirement-plan products.

Lloyd Blankfein, former Goldman Sachs CEO who led the firm during the global financial crisis, also said "the likelihood of a private-credit market collapse is increasing." He noted that each time a crisis hits, people repeat that "system-wide leverage is low," only for hidden risks to surface all at once—recalling the 2008 global financial crisis. Howard Marks, chairman of Oaktree Capital who predicted the dot-com bubble, shares the view. Citing the BCRED redemptions, he said, "Markets tend to reject new information that conflicts with existing beliefs, then suddenly break down."

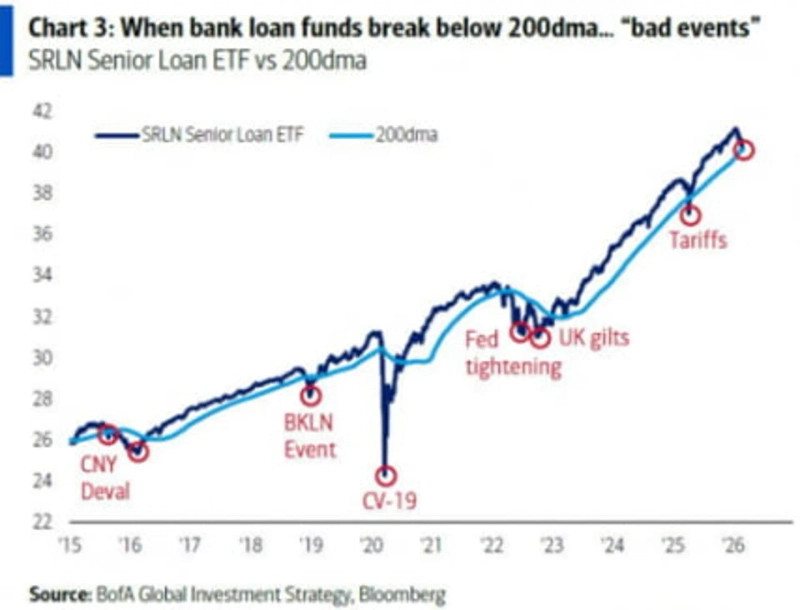

Bank of America’s Hartnett strategist argues that leading indicators of a shock are appearing not only in private lending but across the broader credit market. The basis is that senior-loan ETFs and financial-sector ETFs have recently broken below long-term trend lines. Hartnett warned that, as in the past, when credit falls first, stocks that looked healthy are at elevated risk of falling alongside.

Still, with financial stocks up significantly since last year, the current decline could be a simple correction. Blackstone President Jon Gray said valuations are being conducted rigorously and dismissed today’s worries as mere noise. Ares Management CEO Michael Arougheti pushed back, saying UBS’s 15% default scenario is exaggerated.

Goldman Sachs CEO David Solomon emphasized that while there are issues in a small number of cases, it is not a problem for the overall credit market, saying, "We have not seen broad-based deterioration across private-credit fund portfolios." The fact that institutions such as the Soros fund are buying on weakness shares of listed private-lending companies (BDCs), whose stocks have plunged amid the "AI doomsday" narrative and private-lending stress concerns, also suggests the crisis talk may be overstated.

Possible market scenarios ahead

Putting the views together, the market could unfold along four broad scenarios.

(1) A "soft landing" in which Iran risk subsides and oil and inflation worries stabilize, while credit risk and the AI valuation overhang are contained. Wall Street currently sees this as the most likely base case. It is also supported by the belief that today’s Fed will step in to backstop the system if trouble emerges across private credit (Citi).

(2) A "reflation" scenario in which the economy overheats. This aligns with plans attributed to Trump’s economic team to stimulate growth through looser fiscal and monetary policy and address high debt burdens via inflation. Morgan Stanley CIO Wilson, who has argued for a bullish view since last year, and legendary investor Stanley Druckenmiller have expressed this perspective. Druckenmiller proposed a portfolio of buying stocks, holding gold and copper, and selling bonds to prepare for rising inflation.

There are negative scenarios for financial markets as well. (3) While less likely, the private-credit impairment crisis Wall Street worries about could ultimately materialize. In that case, many companies that have tapped private markets to fund AI investment could see their financing dry up, risking an AI-bubble burst. (4) Finally, a dystopian scenario in which AI triggers faster-than-expected mass white-collar unemployment, leading to weaker consumption, recession and a market breakdown.

Ultimately, the key variables that will determine the direction of global markets are not the one-off shock of a war, but the trajectory of inflation and the spread of stress in private credit.

New York=Correspondent Bin Nansae binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.