Not gas prices but the ‘dollar’ is the problem… the hidden bomb in the energy shock [Global Money X-File]

Summary

- After U.S. and Israeli strikes on Iran, international crude and natural gas prices surged, increasing pressure on energy importers’ external balances and global inflation, the report said.

- As emerging-market currencies weaken and preference for the dollar intensifies, government bond yields are rising and money is flowing into money market funds, amplifying volatility in capital markets, it added.

- Central banks face a dilemma between delayed rate cuts and keeping rates high amid energy-driven inflation, while Asian emerging economies—including South Korea—are particularly vulnerable due to energy dependence and the risk of current-account deterioration, it said.

Forecast Trend Report by Period

The Middle East-driven crisis in the global energy supply chain, triggered by U.S. and Israeli strikes on Iran, is shaking foreign-exchange and capital markets worldwide. Markets are preemptively pricing in the deterioration in external balances of energy-importing countries and the limits of central banks’ monetary policy. If crude shortages also feed into inflation, the fallout is likely to grow larger.

Crude prices surge

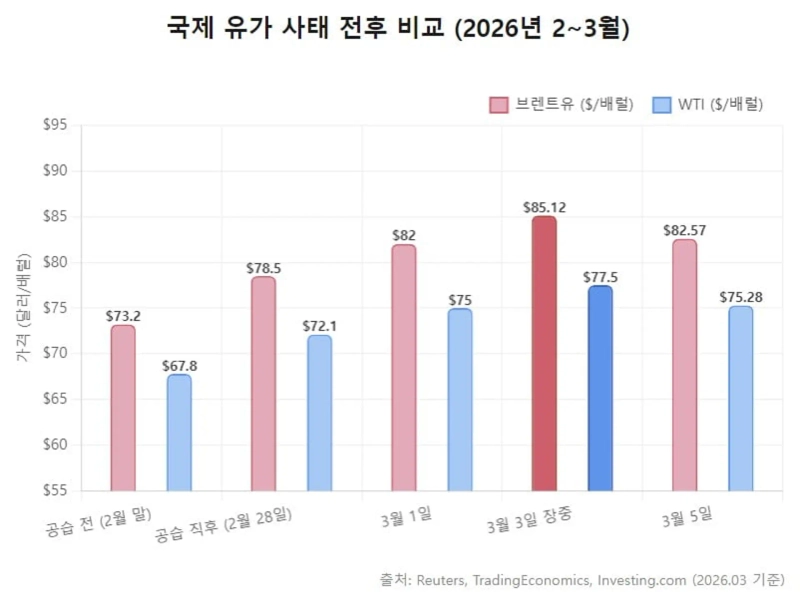

According to Reuters on the 5th, during Asian trading hours global benchmark Brent futures traded at $82.57 a barrel, rising more than 5% over the past two days. U.S. West Texas Intermediate (WTI) also jumped to $75.28 a barrel. In intraday trading on the 3rd, Brent touched $85.12 a barrel, the highest level in 1 year and 8 months since July 2024.

Oil prices spiked after the U.S. and Israel struck Iran on the 28th of last month. Goldman Sachs CEO David Solomon told Reuters that “it could take ‘several weeks’ for the market to fully digest the true macroeconomic significance of this event and reprice fundamentals.”

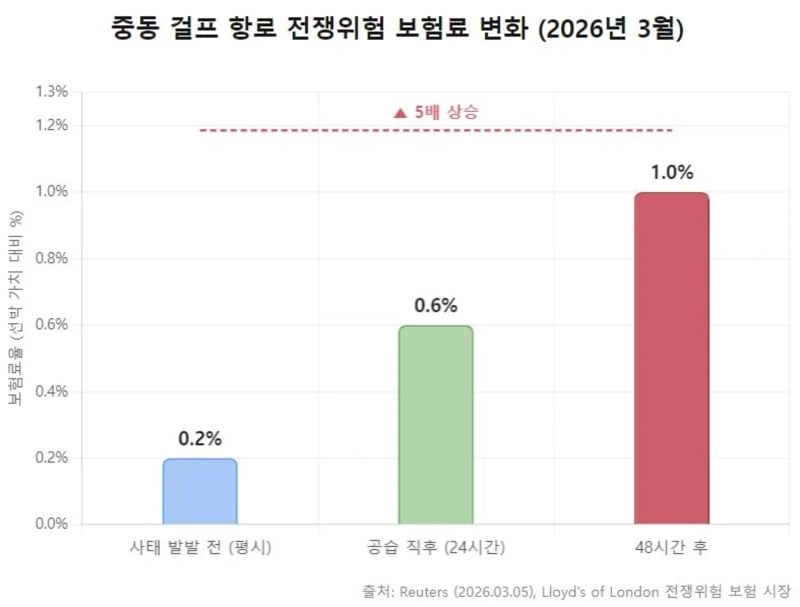

The U.S. strike on Iran is having a major impact across the entire global manufacturing value chain. The first area effectively brought to a halt by the direct hit has been global shipping logistics and the marine insurance industry. As Iran’s threats of retaliation over passage through the Strait of Hormuz came into view, global insurers immediately moved to reduce risk to curb potential losses. According to Reuters, war-risk insurance premiums charged on merchant vessels transiting Gulf routes in the Middle East jumped fivefold—from about 0.2% of a ship’s value just before the outbreak to as high as 1.0% within 48 hours.

Some conservative large London-based reinsurers said they would completely withdraw coverage for those high-risk waters starting on the 5th. Even before bombs or missiles hit ports, insurance—part of the financial system—had already effectively grounded ships, triggering a logistics freeze.

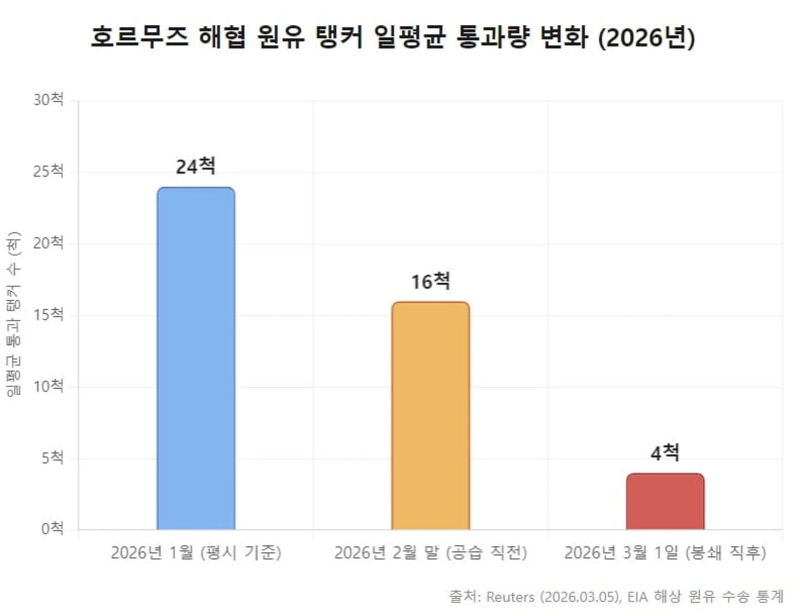

With coverage cut and safety severely threatened, bottlenecks appeared immediately across global logistics networks. Reuters reported that the number of crude tankers passing through the Strait of Hormuz—an average of 24 vessels per day as of January this year—shrunk to just four on March 1.

Tanker operations become difficult

Shipowners abandoned voyages to protect assets, and 150 very large crude carriers (VLCCs) dropped anchor outside the strait after giving up entry. Including anchorages off the coasts of the United Arab Emirates (UAE) and Oman, around 750 merchant ships worldwide are reportedly stranded and waiting.

This includes about 100 large container ships, roughly 10% of the global container fleet. Not only crude, but global logistics for consumer goods and key components is being affected in a cascading fashion. The shortage of ships has fed directly into a spike in ocean freight rates; a single-voyage charter rate for a tanker loading crude at Yanbu, Saudi Arabia, and heading to South Korea was reportedly fixed at $28 million—well over double the usual level.

Production infrastructure in Middle Eastern oil exporters that directly extract and export crude and natural gas has also faced partial physical shutdowns. Iraq, which can export crude only through the Strait of Hormuz, could not withstand the depletion of spare capacity in inland storage tanks due to tanker scheduling delays and implemented large, forced production cuts. Iraq has already preemptively reduced crude output by 1.5 million barrels per day. JPMorgan’s commodities research team outlined a scenario in which a strait closure lasting eight days would cause a global supply disruption of 3.3 million barrels, rising to as much as 4.7 million barrels after 18 days.

The impact on the natural gas market is even larger. Qatar, one of the world’s largest LNG exporters, abruptly suspended LNG production and loadings citing the safety of its vessels and facilities. Europe, with fragile energy self-sufficiency, took a direct hit. On the 4th, Europe’s natural gas benchmark price surged about 65% in just two days as fears of Qatari supply disruptions piled on.

The unusual simultaneous rise in logistics costs and raw-material prices also affects global manufacturing. In petrochemicals, where naphtha is cracked into base feedstocks, soaring costs are likely to compress ethylene margins. Heavy industries that consume large amounts of energy—such as steel, cement and autos—will also be affected.

The paralysis in maritime transport is also expected to spill over into the air cargo market. If semiconductors, biopharmaceuticals and high-tech components abandon sea freight and rush into air cargo, it could add upward pressure to global airfreight rates already saturated by ultra-low-priced Chinese e-commerce volumes. This could be passed through into higher final prices for consumer goods—eroding corporate profitability while pushing up consumer inflation.

Financial markets showed mixed indicator moves. According to Lipper, a financial data analytics subsidiary of London Stock Exchange Group (LSEG), $47.9 billion in cash flowed into money market funds (MMFs) worldwide immediately after the outbreak, with $30.75 billion absorbed by U.S. MMFs alone. Jan Nevruzi, a macro strategist at U.K. investment bank NatWest Markets, told Reuters that “global financial markets are currently fleeing risk and sprinting aggressively into cash.”

In FX markets, differentiated decoupling emerged depending on countries’ economic structures. Over the weekend immediately after the outbreak, the safe-haven Japanese yen and Swiss franc mechanically strengthened on war-risk headlines. But as it became clear that damage to the energy supply chain would be fatal for the eurozone and Asian emerging economies, capital flowed into the U.S. dollar (USD), backed by energy self-sufficiency and dominant hegemony.

This U.S.-Iran military confrontation is also stoking ‘stagflation’ fears. The argument is that this economic shock is not about lagging indicators like inflation, but about the deterioration in the external balances (balance of payments) of emerging markets that import commodities—and the resulting paralysis of central banks’ monetary policy.

Rising burden of commodity costs

The surge in international oil and natural gas prices worsens the terms of trade for importing countries that source most of their energy externally. To buy the same amount of oil, they must pay more dollars abroad than before. This means additional value generated by the country leaks out. As a result, the current-account surplus—a key gauge of a country’s economic fundamentals—can shrink sharply or swing into a large deficit. In FX markets, dollar demand for import settlement rises, structurally driving a steep decline in the value of the local currency.

Research analysts at Dutch financial group ING estimated in a report that “even a 10% rise in international oil prices could worsen emerging markets’ current accounts by 0.40–0.60% points of GDP.” ING cited Thailand, South Korea, Vietnam, Taiwan and the Philippines as the countries structurally most vulnerable to such external-balance shocks.

Goldman Sachs warned in a March report that “if a supply shock pushes Brent from $70 to around $85 a barrel, overall inflation in Asian emerging economies could rise by about 0.7% points, while growth could be hit by a roughly 0.5%-point decline.”

Global FX markets reacted immediately. India’s rupee hit a record low on the 4th, with the exchange rate reaching 92.17 rupees per dollar. Citigroup macroeconomists warned that “a prolonged oil shock could completely unanchor inflation-control expectations across emerging markets,” adding that “fragile countries with thin dollar FX buffers—such as Argentina, Sri Lanka, Pakistan and Türkiye—could be exposed to a chain-reaction default risk driven by capital outflows and currency collapse.”

Major central banks are likely to be caught in a bind. The monetary policy of the U.S. Federal Reserve (Fed) and the European Central Bank (ECB)—which had been wrapping up tightening in 2024–2025 and weighing entry into a rate-cut cycle on the back of cooling inflation—will be affected. If surging energy prices stoke imported inflation and push inflation higher, cutting policy rates too quickly to support domestic demand could easily lift inflation expectations.

On the other hand, keeping rates high to contain inflation risks accelerating a slump in the real economy already crushed by cost pressures, raising the likelihood of a wave of bankruptcies among marginal firms. Will Compernolle, a macro strategist at U.S. FHN Financial, warned that “given current U.S. economic indicators and sticky inflation, there is absolutely no comfortable window for the Fed to dismiss a temporary inflation spike from this energy supply shock as mere noise and look past it.”

On expectations of inflation risks and delayed rate cuts, government bond yields rose immediately. As of the 3rd, the U.K. two-year gilt yield jumped to as high as 3.84% intraday. Germany’s two-year yield rose to 2.236%, and the U.S. two-year Treasury yield also climbed to 3.599%.

Europe—which suffered an energy crisis during the Russia-Ukraine war when natural gas pipelines were cut—could be hit harder. Martins Kazaks, governor of the Bank of Latvia and an ECB Governing Council member, told Reuters that, concerned about rising geopolitical uncertainty, “until the situation becomes clearer, we must stay on hold on policy rates for now and fully re-examine the March meeting scenarios.”

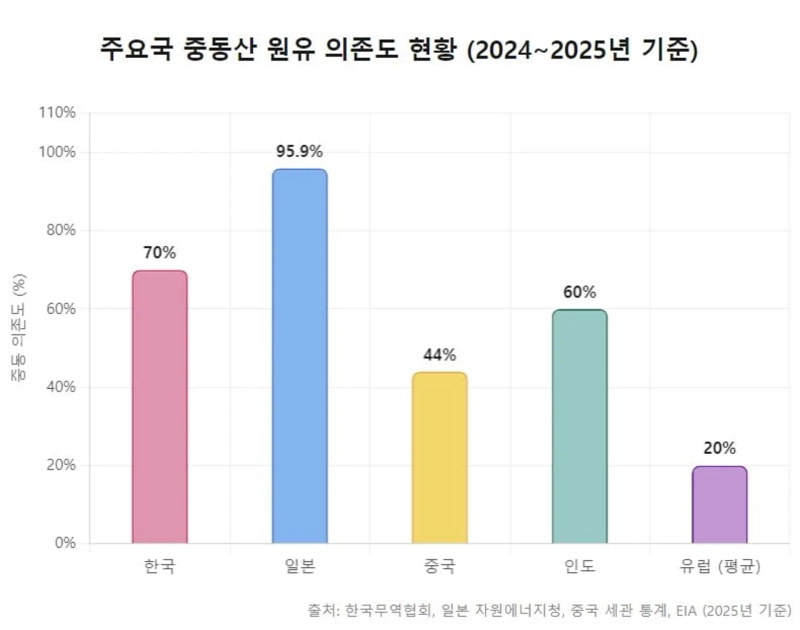

South Korea was also hit head-on. The country relies on the Middle East for about 70% of its crude imports and about 20% of its natural gas (LNG) imports. Key domestic industries such as semiconductors, steel and autos rank among the most energy-intensive.

Reporter Kim Joo-wan kjwan@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.