"The real bottom isn’t in yet" Sell-off warning… Where is the turning point for U.S. stocks? [Wall Street Without Gaps by Bin Nansa]

Summary

- Wall Street said the “real bottom” in U.S. equities has not yet formed, citing oil prices, a strong dollar, uncertainty over the Iran war, and negative gamma, among other factors.

- Citadel Securities said March 20—when $5 trillion of options expire—could be an inflection point, as mechanical selling pressure may ease afterward and allow stocks to regain direction.

- Wall Street advised that, for now, risk management, selecting high-quality companies, and preparing a “shopping list” for a potential bull-market resumption are needed rather than premature bargain buying.

Forecast Trend Report by Period

After President Donald Trump’s comment on the 9th (local time) that “the war is almost over,” fears of a prolonged Iran war have eased somewhat, but it still looks like there is a long way to go until a “real end to the war.” That is what the market is signaling through stubbornly high oil prices and volatile equities.

On the 11th (local time), in overnight trading on NYMEX and ICE futures, West Texas Intermediate (WTI) and Brent crude each jumped more than 7%. WTI surged back above $90 a barrel, while Brent is nearing $99 a barrel. This is because there is still no sign of tensions easing around the Strait of Hormuz—the root cause behind the oil rally—even though, under a proposal from the International Energy Agency (IEA), countries agreed to release a record 400 million barrels from strategic stockpiles.

Oil rises despite record stockpile release

According to JPMorgan, what matters more to the oil market than “how much” is released is “how fast” it is released—and the realistic pace at this point is about 1.2 million barrels per day. Given estimates that supply disruptions from a Strait of Hormuz closure could amount to roughly 15 million barrels per day, that is nowhere near enough to stabilize prices.

Trump added to market confusion by delivering mixed messages again that day—claiming “we’ve already won,” “the war will end soon,” and “there’s no problem with oil flows,” while also saying “it’s not time to leave Iran yet” and “we will” release U.S. strategic petroleum reserves “(to bring down oil prices).” According to Bloomberg, the Trump administration is also considering invoking the Cold War-era Defense Production Act alongside SPR releases to restart offshore oil production off the Southern California coast. Lisa Shalett, CIO at Morgan Stanley Investment Management, said that policymakers looking “as if they’re panicking” can leave investors with the impression that the war and oil-price surge may last longer—“which is in itself an unsettling signal.”

Still, Trump’s stance has clearly shifted compared with last week, when he said that “even if oil rises a bit, it’s cheap as the price of peace.” Since the 9th, when Brent topped $120, the tone has turned toward seeking an exit strategy as quickly as possible. As disruptions through the Strait of Hormuz send gasoline and diesel prices sharply higher—costs U.S. voters feel every day—the burden on the Trump administration ahead of the midterms is growing. With heating oil, jet fuel, fertilizers and industrial raw materials also climbing in tandem, some warn of a second-round inflation shock hitting agricultural products, food and airfares.

With affordability already a core issue heading into the U.S. midterms, the risk of inflation reigniting is critical. That is why, since the U.S. and Israel began military operations against Iran on the 28th of last month, Wall Street has expected the Trump administration would be unlikely to drag the Iran war into a prolonged campaign of more than 4–6 weeks while tolerating an oil-price spike. Trump’s visible shift in tone lends weight to that scenario. The sharp stock rebound on the 9th and the subsequent recovery in tech shares reflect that optimism.

Even so, some on Wall Street warn that “the storm hasn’t fully passed,” and that rushing to buy is risky. Some analyses suggest the likelihood of large-scale selling in U.S. equities over the next week is high. The argument is that uncertainty and volatility remain elevated without confirmation of a “real” end to the war and oil-price stabilization, and that technical supply-demand constraints capping the rally have yet to be cleared.

Between expectations and reality on an early end to the war

From a macro perspective, the key variable is ultimately oil. Even after Trump’s comments that an end to the war is near, oil is holding more than $20 a barrel above pre-war levels. The key questions are when an actual end—not just rhetoric—will be reached, when logistics through the Strait of Hormuz normalize, and when oil returns to pre-war levels.

Militarily, the overwhelming advantage of the U.S. and Israel appears clear. But experts warn that Iran cannot be ruled out from adopting a “scorched earth strategy,” with nothing left to lose. Bank of America said “the Iranian regime is maintaining a more hardline leadership structure, and its relations with neighboring countries have deteriorated,” adding that a “scorched earth strategy” to maximize economic disruption “could be Iran’s most powerful tool” to plunge financial markets into a bigger shock. Unlike the U.S., which must pay attention to market reactions and public opinion, Iran’s authoritarian regime could resort to brinkmanship even at the cost of mutual destruction.

UBS also urged caution after Trump’s comments, saying “there is a gap between market optimism and reality.” With the S&P 500 down only about 3% since the war began, if the oil-price stabilization the market is counting on fails to materialize quickly, there is a risk that disappointment selling could spill out at any time. UBS said the key variables are when the U.S. declares its objectives achieved—i.e., a “real end to the war”—and whether normal passage through the Strait of Hormuz is restored.

“Systematic selling pressure is intensifying”

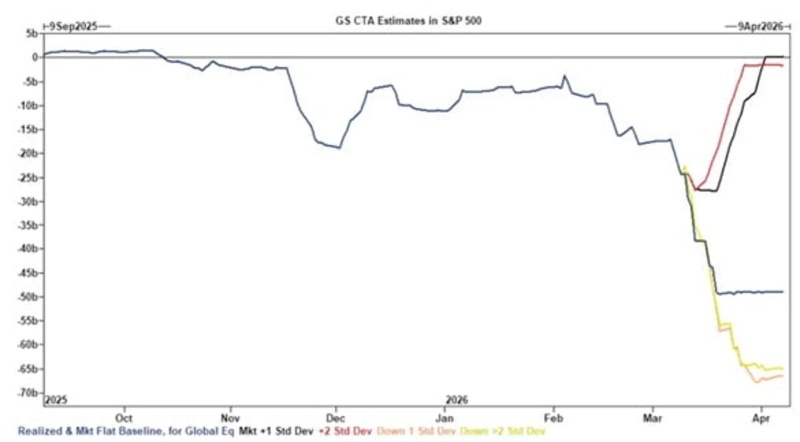

Technical flows are also unfavorable for a rally. On the 10th, Goldman Sachs’ trading desk said extreme volatility recently triggered forced risk-management mechanisms among trend-following CTA funds. That means that over the next week to a month, regardless of whether the S&P 500 rises or falls, these algorithmic strategies are likely to be net sellers of equities to reduce risk exposure. The scale of that net selling is even expected to be as large as historical extremes.

Market makers, as liquidity providers, are also contributing to volatility. When market makers sell options to clients, they mechanically hedge to manage the risk from moves in the underlying asset. But in today’s options-market regime (negative gamma), that hedging can amplify volatility. Put simply, a structure can form in which market makers have to sell more when prices fall and buy more when prices rise—creating conditions for larger swings. In a market with heavy selling pressure, such “negative gamma” is structurally unfavorable for upside.

Liquidity has also dried up. According to Goldman Sachs, order-book depth in the Nasdaq futures market has thinned to around the level seen in April last year, when it hit a historic low. That suggests a fragile market in which even small shocks can cause outsized price swings. Goldman said it “shows that market participants have broadly lost conviction about direction.”

Despite the recent decline, Wall Street believes a meaningful bottom has not yet been set. JPMorgan’s Positioning Intelligence team said that as of the 10th, U.S. equity investors’ positioning had only retreated to roughly neutral, and that full deleveraging has not yet occurred. That implies the market lacks sufficient “dry powder” to absorb another shock—put simply, there are still more sellers left.

Morgan Stanley’s Mike Wilson, CIO, also said that “a correction typically ends only after the very highest-quality stocks and the indexes are hit, and we’re not at that point yet,” predicting that “the market could struggle for about another month.”

He said more specifically that the S&P 500 could slide to around 6,300 by early April. Only then, he argued, would the favorable underlying fundamentals that underpin the bull market be able to reassert themselves.

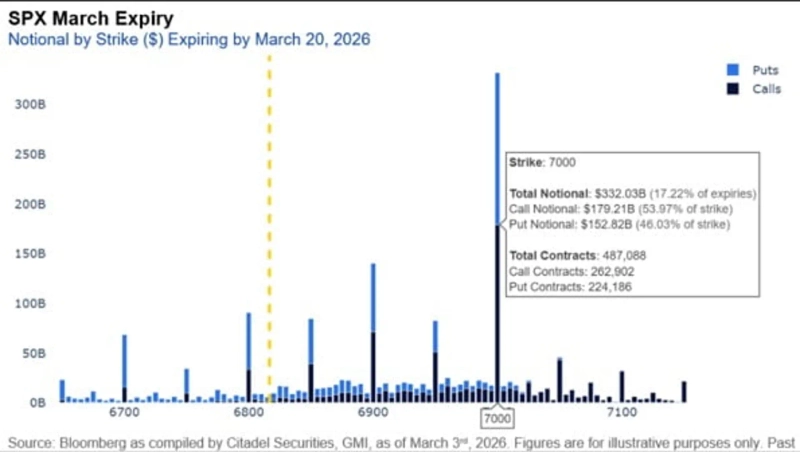

“$5 trillion options expiry—March 20 is the inflection point”

Scott Rubner, head of equity derivatives strategy at Citadel Securities, points to March 20—when monthly and quarterly options expire—as the most important technical event. Rubner, who correctly called the bear market in February this year, wrote in a report on the 4th that he is “withdrawing” the “tactical bearish” view he presented in February, and said that if the various mechanical flow constraints weighing on the market are cleared by mid-March, a full-fledged risk-on environment could unfold from April.

That, he says, is why March 20 could become the key inflection point. It is the day a record index-options expiry of $5 trillion comes due. Rubner expects that once this massive expiry passes, mechanical selling pressure that has been holding back the market will be absorbed, allowing the index to break out of its tight range and regain direction.

In fact, through March 1 this year, the S&P 500’s peak-to-trough range was 4.3%, the smallest in 20 years. Volatility has increased since the Iran war, but compared with swings in individual stocks, the index’s own moves are not extreme given the magnitude of the geopolitical shock. Rubner attributes the index being so suppressed to the enormous scale of options trading and market makers’ overwriting (Overwriting) flows used to hedge it. When options expire on the 20th, that market structure will also reset.

Of course, there is no guarantee the market will move higher afterward. Still, Rubner argues that several factors support upside expectations: △if there are signs of easing geopolitical risk, large-scale profit-taking on now-expensive put options could provide short-term fuel for a rebound △if the VIX calms, algorithmic funds could resume mechanical buying △large U.S. tax refunds in March–April could strengthen retail investors’ liquidity buffer △and historically, April has delivered the second-highest U.S. equity gains of the year.

A U.S.-China leaders’ summit between President Trump and President Xi Jinping, slated for late March to early April, could also further reduce geopolitical risk.

“Confirm the real bottom rather than rushing into a ‘full buy’”

In conclusion, the prevailing view on Wall Street is that this is a phase where it is preferable to proceed cautiously—waiting for oil prices and dollar strength to cool decisively and for technical conditions to improve—rather than jumping into bargain-hunting on premature optimism. Unease in private credit markets, which Wall Street is watching as a bigger long-term risk factor than the Iran war, is also persistently weighing on U.S. equities. Wilson said “the index could still fall 5–7%, and heavily crowded names could see additional double-digit declines,” adding that “(the bull-market thesis hasn’t been damaged) but prices still aren’t cheap enough.”

At the same time, he advised: “A final bottom forms faster than a top,” and said investors should prepare a “shopping list” with a bull-market resumption in the second half of this year in mind. After the storm passes and the real bottom is confirmed, the investment narratives that led the previous bull market can regain leadership—themes such as the race to secure AI infrastructure, U.S. reindustrialization, bets on the Trump administration’s willingness to stimulate the economy ahead of the midterms and on fiscal and monetary easing (the “reflation trade”), and a preference for real assets.

If the bull-market thesis is intact, this is not the time to panic-sell in fear. But Wall Street’s consistent message is that it is not yet the time to aggressively chase the rebound either. This is the moment to put risk management front and center while selecting high-quality companies that could lead the next real upswing.

New York=Correspondent Bin Nansa binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.