Trump’s gamble as he can’t ‘TACO’… Markets jolted by warnings of a ‘worst-case scenario’ [Bin Nan-sae’s Wall Street, No Gaps]

Summary

- It said that the U.S. strike on military facilities on Kharg Island and Iran’s retaliatory airstrikes on Fujairah port are heightening risks of a surge in oil and commodity prices and disruptions across global supply chains.

- It reported that Jeff Currie of Carlyle Energy said the situation is pushing commodities into a phase of structural repricing that reflects a security premium, potentially accelerating a commodities supercycle.

- It reported that Wall Street is highlighting a real-asset-centered investment environment known as the HALO trade, and that energy, metals, fertilizers, agricultural products, basic materials, physical infrastructure and manufacturing could command increasingly higher valuations.

Forecast Trend Report by Period

U.S. strikes military facilities on Iran’s Kharg Island

Despite threats to hit key oil infrastructure

Iran retaliates with airstrikes on an alternative Hormuz route

**“Iran has the global economy by the throat

Trump’s ‘Hail Mary’ because he can’t TACO”

Trump even asks China to send warships

Beyond oil—fertilizer, gas, minerals, etc.

Disruptions across the global supply chain

“Even if a ceasefire happens immediately, the world has already changed”

The ‘just-in-time’ era for energy and commodities is over

Prices repriced with a ‘security/real-economy premium’

From peace to fragmentation, the ‘HALO’ trade

Is the worst-case scenario the market feared in an Iran war becoming reality? The U.S. military struck Kharg Island, which accounts for 90% of Iran’s oil exports. What was destroyed this time were only military facilities, but markets fear a prolonged tit-for-tat escalation that could ultimately extend to energy infrastructure. President Donald Trump confirmed the strike himself on Truth Social on the 13th (local time), saying, “For the sake of propriety we did not destroy oil infrastructure, but if Iran or anyone else obstructs passage through the Strait of Hormuz, we will reconsider immediately.”

Kharg Island is home to Iran’s main crude-export terminal. It can ship up to 7 million barrels a day. In normal times, it accounts for about one-third of the crude passing through the Strait of Hormuz (about 20 million barrels a day). Iran has continued exporting large volumes of crude centered on Kharg Island even after the war broke out. Precisely because it is such a strategic chokepoint, if the island’s oil infrastructure is destroyed, Iran’s export capacity would be structurally impaired, and repairs could take years. It is a key variable that could send oil prices surging again, coming on top of a Hormuz blockade now heading into its third week and production cuts by Middle Eastern producers.

Trump warned that “Iran’s military and everyone involved with this terrorist regime would be wise to lay down their weapons and protect what remains,” but Iran immediately retaliated on the 14th with airstrikes on oil storage facilities at Fujairah port in the United Arab Emirates (UAE).

Fujairah, like Oman’s Salalah port previously attacked by Iran, was one of the oil-export routes that can substitute for the Strait of Hormuz. Linked by an onshore pipeline to Abu Dhabi’s Habshan oil field, it allows crude exports to bypass Hormuz and go straight out via the Gulf of Oman; shipments are reported to have been suspended following the attack. Iran carried out the strike after threatening, immediately after the U.S. attack on Kharg Island, that “if Iran’s oil and energy infrastructure is attacked, we will turn to ashes the energy facilities owned by companies cooperating with the United States.”

Trump later named China, France, Japan, South Korea and the U.K., writing on Truth Social that he “Hopefully” wants other countries affected by Iran’s attempt to blockade Hormuz to send warships to the region alongside the United States. Bloomberg energy and commodities columnist Javier Blas wrote on X that he could not understand how, even as the White House said it had anticipated (and even prepared for) Iran’s attempt to blockade Hormuz, its response amounted to the president asking even hostile countries like China on social media to send warships to reopen the sea lanes.

“Kharg Island strike, Trump’s gamble because he can’t TACO”

Jim Bianco, founder of Bianco Research, likens the Trump administration’s decision to strike Kharg Island to a “Hail Mary pass,” an American football term. “Hail Mary” refers to a prayer to the Virgin Mary—an expression of hoping for a miracle. In football, it describes a last-ditch long throw when time is running out and there’s no time for a normal, prepared play—launched in hopes someone comes down with it. The odds are low, but it’s a desperate, gambling play aimed at a comeback in a single attempt.

Bianco said that “it could take weeks to months to seize control of Hormuz, and if oil prices keep rising during that time, the global economy could be damaged,” adding that “if oil is going to $200 anyway, they may have thought it’s better to (hit Kharg Island quickly) and spike prices next week, then focus on bringing prices back down over the six months left until the midterms.” In that view, the administration pulled out an ultra-aggressive card immediately.

If the midterms and a spike in oil prices are the concern, one might think Trump could simply declare the mission accomplished and withdraw now—i.e., do the so-called “TACO (TACO·Trump Always Chickens Out).” Bianco argues “that would be an even worse outcome” for Trump, because “Iran could hold the global economy by the throat (via control over passage through the Strait of Hormuz) and keep oil at $200, making everyone suffer.”

Iran is already reported to be allowing passage through Hormuz only for vessels from allies or the non-Western camp, and even considering permitting only tankers carrying crude traded in Chinese yuan. If true, it would be an attempt to weaken the “petrodollar” system under which crude is traded in U.S. dollars.

In the end, to stick to its goal of finishing with a short military operation and forcing Iran into complete capitulation, the Trump administration has found itself in a contradiction: it may have no choice but to broaden the conflict, even at the cost of higher oil prices in the near term. Wall Street is maintaining a hope-tinged view that the administration will seek a quick exit strategy, citing gasoline prices in the U.S. jumping to around a two-year high and deteriorating public sentiment among Americans exhausted by inflation.

The problem is that it is becoming increasingly unclear whether Iran’s dictatorship will truly collapse and surrender in the short term. U.S. and Israeli intelligence agencies have recently assessed that, even after the military operation began, the likelihood of regime collapse in Iran is not high. Instead, Iran is doubling down on a “long war, high oil prices” strategy—focusing on attacks on neighboring Gulf states and energy infrastructure rather than responding directly to U.S.-Israeli bombing.

At this rate, the risk cannot be ruled out that the U.S. ultimately deploys ground forces, or that Saudi Arabia and the UAE join the fighting, widening it into a regional Middle East war. As the ancient Roman historian Sallust put it, “war is easy to start but very hard to stop”—and the risk of sliding into such chaos keeps rising.

The single most important variable right now: oil

From the market’s perspective, the sole key variable remains oil—more broadly, commodity prices. Supply chains for not only crude and refined products but also petrochemicals, industrial gases, fertilizers, agricultural products and minerals are being disrupted one after another.

Urea, a feedstock for nitrogen fertilizer, has jumped 40% since the Iran war began, while helium gas—an essential material for semiconductor manufacturing—and tungsten have also suffered supply disruptions, with prices in severe cases doubling. Indium phosphide, a material used in optical devices and optical-communications substrates that has recently drawn attention, is also seeing worsening shortages. If this situation drags on, it will not only raise costs across industry; fertilizer price increases and agricultural shortages will inevitably re-ignite food inflation.

If the scenario of a prolonged war and high oil prices gains traction, recession fears could also come to the fore. In bond markets, a tug-of-war over this is already under way: (1) high-oil inflation fears → global central banks delaying rate cuts or hiking rates → higher sovereign yields, versus (2) prolonged inflation → demand destruction → recession → higher government bond prices (lower yields).

Now, the path of oil hinges on whether the oil facilities on Kharg Island are actually hit. If that happens, the situation could spiral into the worst-case scenario: irreversible, “mutual-destruction”-style attacks on energy infrastructure by both sides and a surge in oil prices. Brent has already climbed back above $100 a barrel, and Asian economies with high dependence on energy imports—such as South Korea, Japan and Taiwan—are already suffering fuel shortages. Not only Europe, which also has a low energy self-sufficiency rate, but even the U.S. cannot avoid, the longer this drags on, a chain of rising energy and commodity prices → higher costs → declining corporate profits. That is why markets, directionless, are staring only at oil and headlines—waiting for when a real end to the war will come and when Hormuz will reopen.

“The end of the just-in-time era”… the security premium in commodities

Energy experts advise that investors should look beyond war as a short-term event and focus on a sweeping structural shift that changes the paradigm of the global economy—geopolitical fractures and a reshaping of global supply chains.

Jeff Currie, chief strategy officer (CSO) at Carlyle Energy, said in an interview with Bloomberg TV on the 11th, “Even if a ceasefire happens five minutes from now, the world has already changed. This shock isn’t a simple war event—it shook the global supply chain itself,” adding that “commodities are entering a phase of structural repricing that reflects a security premium.”

He explained that this episode is accelerating a regime change in the energy market. In the globalized market of the past, “just in time” procurement made it possible to source as much energy as needed cheaply, anytime and anywhere, as long as you paid. But now, with supply chains fragmenting around the U.S. and China, procurement can be cut off depending on sanctions, geopolitical disputes and alliance structures. Countries, companies and individuals are also shifting to a “just in case” system—building up stockpiles in preparation for emergencies.

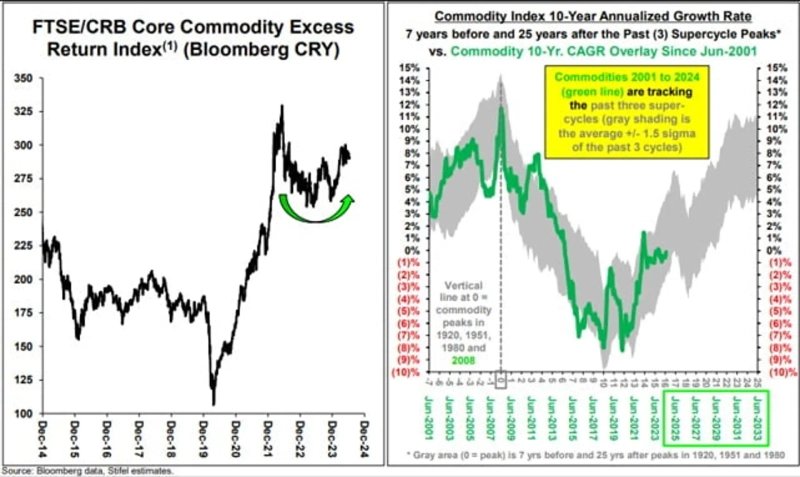

Under this system, energy shifts from a “commodity” that can be sourced cheaply and efficiently to a “strategic material” where security must take priority. Currie argued that “not just oil, but all cross-border commodities will carry a security premium—‘security first.’” He suggested that the commodity upcycle that began gradually in 2020—the “commodities supercycle”—could accelerate.

An investment framework for an era of fragmentation: ‘HALO’

These geopolitical shocks and a rise in real interest rates driven by inflation are also changing the investment logic in global asset markets. Over the past decade-plus, it was an asset-light economy led by software-centric tech firms and intangible financial assets, with low burdens for capex and capital investment. With zero rates and massive liquidity, hardware costs fell and the real value of tangible assets such as factories and production facilities declined.

But now, companies holding capital in real assets that cannot be easily replicated (Heavy Asset) and that does not easily become obsolete even as technology advances (Low Obsolescence) are being re-rated. Here, “real assets” includes not only physical infrastructure such as commodities and production facilities, but also capital such as manufacturing technology, networks and intellectual property that take a long time to build and are hard to imitate because of regulation, costs and know-how. On Wall Street, this trend is also dubbed the “revival of the old economy,” or the “HALO (halo) trade,” reflecting a resurgence of manufacturing and the real economy.

This trend also intersects with the reshaping of commodities and manufacturing supply chains, as well as the AI boom. While concerns are growing that software and IT services can be rapidly replicated and replaced by AI, the physical infrastructure essential to run AI—semiconductors, data centers, power grids and transformers—cannot be mass-produced overnight. That makes them even scarcer.

And geopolitical risks like the Iran war, along with supply-chain fragmentation, make it more expensive to procure these scarce resources. Just as China can’t buy Nvidia’s advanced AI chips, and U.S. companies can’t buy China’s cheap memory chips.

Ultimately, the Iran war—alongside U.S.-China tensions and Trump’s tariffs—could become one scene in a structural transition in which the paradigm of the global political economy shifts. The era of peace and ultra-low rates is ending, and the world is moving into an era of security priorities, high inflation and high interest rates. If so, investors must also prepare for a world in which asset prices carry security and real-economy premiums even after the war. An era could be taking shape in which commodities—including energy and metals, fertilizers and agricultural products—basic materials, physical infrastructure and manufacturing command increasingly higher valuations.

New York=Correspondent Bin Nan-sae binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.