Aftermath of the Middle East war… If ‘oil money’ stops, global financial markets will be shaken [Global Money X-File]

Summary

- Gulf sovereign wealth funds are said to be moving to pause new investments and review asset sales and sponsorship contracts amid the Middle East conflict.

- As a result, liquidity strains and valuation pressure are rising for Gulf-capital-dependent asset classes such as private equity (PE), venture capital (VC), commercial real estate and AI infrastructure.

- A slowdown in Gulf overseas investment could lead to higher borrowing costs in global bond markets and higher-for-longer rates, while for South Korea it could translate into indirect headwinds via energy inflation and tighter global financial conditions.

Forecast Trend Report by Period

Concerns are growing that the Middle East is triggering a tightening of liquidity in global financial markets. Gulf sovereign wealth funds—powerful buyers of global risk assets—are putting new investments on hold as regional conflict escalates.

Gulf sovereign wealth funds revisit plans

Reuters reported on the 26th that three Gulf countries are said to be reviewing how to deploy funds worth trillions of dollars invested by their sovereign wealth funds, in order to offset losses stemming from U.S. and Israeli strikes on Iran.

A source said the review includes withdrawing existing investment commitments, selling assets, and revisiting global sponsorship contracts. The person asked not to be identified given the sensitivity of the matter and did not specify which countries were involved.

A related source said, “Three members of the Gulf Cooperation Council (GCC) will revisit all current and future investment and sponsorship plans if this situation drags on.” Saudi Arabia, the United Arab Emirates (UAE), Qatar and Kuwait are key GCC members.

Global markets are not only watching oil-price volatility tied to a potential closure of the Strait of Hormuz. Attention is also focused on the plans of Middle Eastern sovereign wealth funds. Over the past several years, Gulf capital has played a central role in supplying liquidity to capital markets worldwide—and has also been a key investor driving next-generation technological innovation.

According to Global SWF, a data platform for sovereign wealth funds, total assets under management by state investors worldwide (including central banks and public pension funds) surpassed $60 trillion for the first time as of end-2025. Of that, sovereign wealth funds alone accounted for $15 trillion.

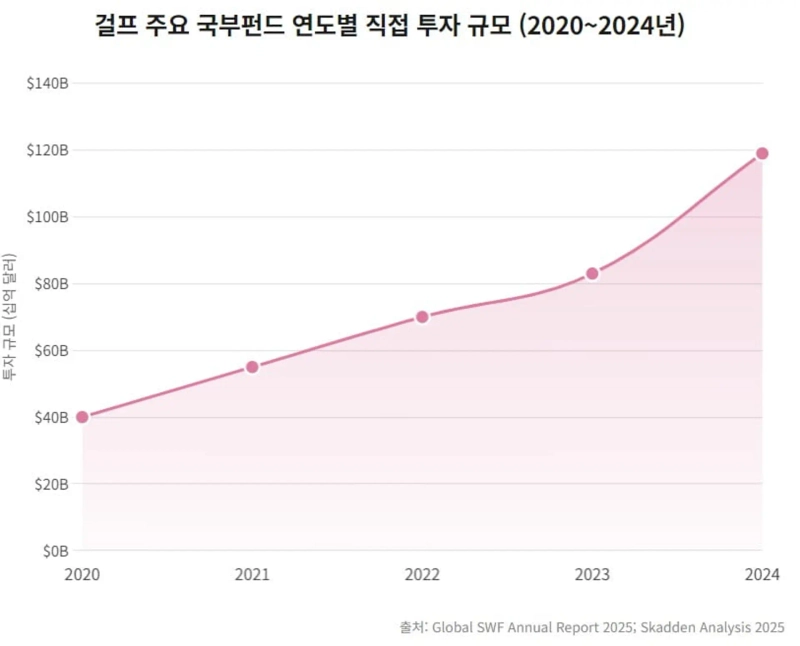

In particular, major funds known as the “Gulf 7”—including Saudi Arabia’s Public Investment Fund (PIF), the UAE’s Abu Dhabi Investment Authority (ADIA) and Mubadala, the Qatar Investment Authority (QIA), and the Kuwait Investment Authority (KIA)—deployed $119 billion of investments last year, up 43% from the previous year. That represented 43% of all state investment globally.

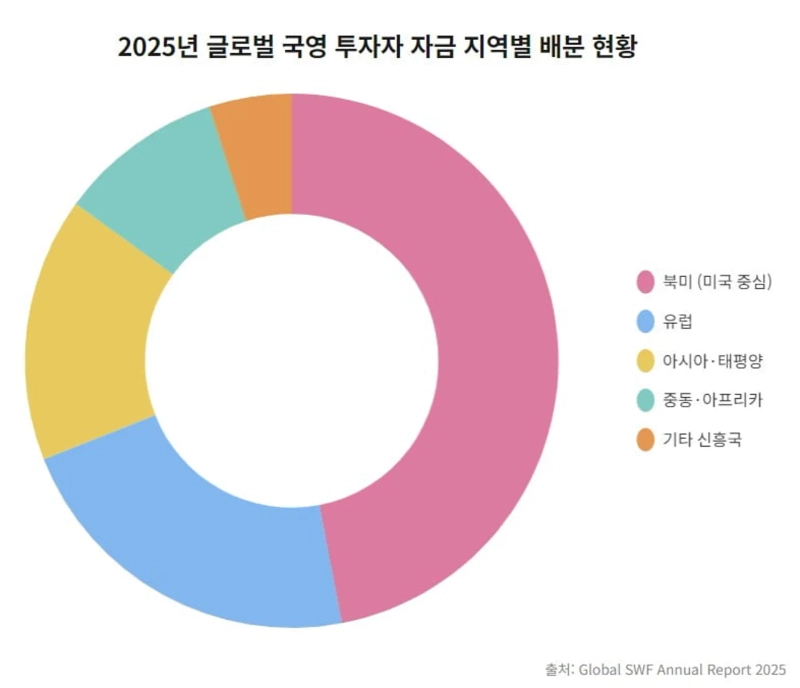

That capital flowed heavily into specific regions and advanced industries. Based on Global SWF data, $132 billion—47% of all state-investor capital in 2025—went into U.S. markets. Infrastructure buildouts at Silicon Valley tech giants, the artificial intelligence (AI) ecosystem, and private credit markets have grown largely on Gulf funding.

But the latest Middle East conflict has put the brakes on Gulf capital pipelines. Partial closures of Gulf air routes, disruptions at logistics hubs, and the normalization of military attacks targeting regional energy infrastructure are placing unpredictable pressure on national finances. As a result, fiscal authorities in Saudi Arabia, the UAE and Qatar are reviewing plans to deploy sovereign wealth funds worth trillions of dollars for domestic defense and to stabilize regional financial systems.

Private equity and VC markets take a direct hit

The first to take a direct hit from reduced Gulf investment are private equity (PE) and venture capital (VC) markets—asset classes with lower liquidity and higher reliance on leverage. The global private equity industry is already facing a frozen exit environment amid strict merger controls in many countries and a weak initial public offering (IPO) market. In that context, the absence of Gulf capital—which had supported downside when asset prices fell—is seen as potentially critical.

Structurally, private equity uses “capital calls,” in which general partners (GPs) request limited partners (LPs) to contribute funds each time an investment is made. If Gulf sovereign wealth funds delay meeting capital calls or sit out new fundraising due to national security and fiscal pressures, major global managers could quickly face a severe liquidity drought.

Managers whose funding lines dry up may halt new investments. They also risk falling into a vicious cycle of having to force-sell even high-quality assets at fire-sale prices to return cash to existing LPs. That could trigger a cascading decline in net asset values across global private assets.

North America and Europe’s depressed commercial real estate markets are also vulnerable. Even amid record vacancy rates, it was Middle Eastern capital that bought landmark assets in London, New York and Paris at low prices, helping defend the downside. If Middle Eastern capital shifts to the sidelines, the repricing and bottoming process for commercial real estate—already facing a massive refinancing wall—will likely be delayed.

Large-scale mergers and acquisitions (M&A) in AI infrastructure and the big-tech ecosystem will also be affected. Global mega-deals such as data-center buildouts require billions of dollars in upfront capital and long investment horizons—an area that has relied heavily on Gulf funding. If Middle Eastern money dries up, valuation models for innovative tech companies seeking new funding will face a sharp headwind.

Some in the market worry that “oil money will dump global assets at fire-sale prices across the board, triggering a large-scale exodus.” But others note that based on current fundamental data and the structural characteristics of these funds, such panic selling is unlikely.

Some experts expect a “quiet throttling,” with selective investments based on rigorous risk management and a slower pace of new deployments. In an interview with Reuters, Sam Bourgi, senior analyst at InvestorsObserver, said, “Our base case is that Gulf sovereign wealth funds are not forced sellers,” adding, “What we’re seeing in public markets is not indiscriminate selling, but a slowdown in overseas investment and quiet portfolio rebalancing.”

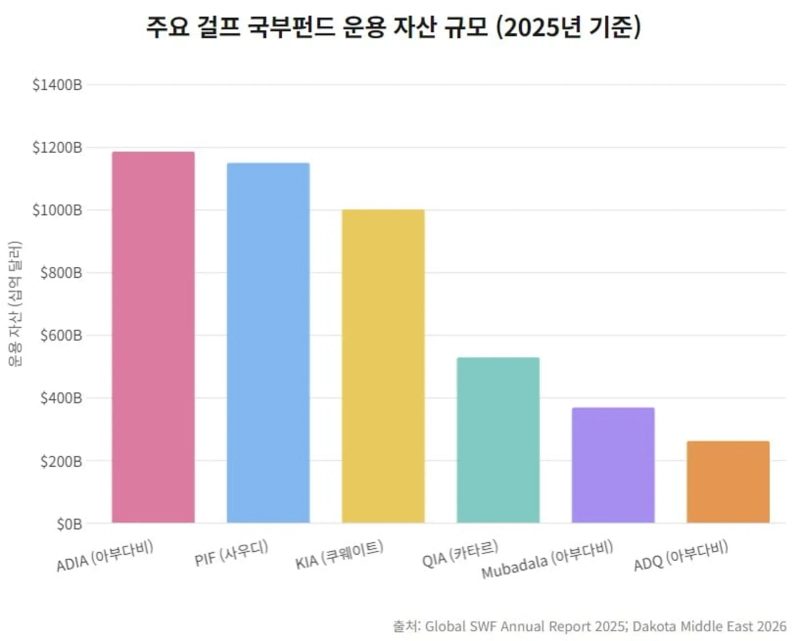

Gulf sovereign wealth funds operate with different objectives. According to Global SWF, Saudi Arabia’s PIF manages about $1.151 trillion in assets, while ADIA is estimated at about $1.187 trillion. PIF, which plays a core role in Crown Prince Mohammed bin Salman’s national transformation project ‘Vision 2030,’ has deployed about 80% of its assets domestically in Saudi Arabia.

By contrast, ADIA adheres to a principle of 100% global diversification. KIA also invests 94% of its assets overseas. These structures provide little incentive to rush into selling high-quality global assets at distressed prices due to temporary fiscal pressure in the Middle East. While they may delay new commitments and adopt a wait-and-see stance amid uncertainty, some expect them to focus only on familiar, safe, top-tier assets in developed markets rather than dumping existing holdings.

Even if a Gulf capital slowdown does not translate into immediate forced selling, it can still weigh on the global macroeconomy. The broadest spillover would be higher borrowing costs in global bond markets—raising concerns that “higher-for-longer” interest rates become entrenched.

Allianz’s chief economic adviser Mohamed El-Erian wrote recently in a Financial Times op-ed that “the world has depended on Gulf capital more deeply than many people think.”

He warned that “GCC countries have run massive current-account surpluses of more than $800 billion over the past four years, and even a short-term reduction in their cross-border capital flows could tighten conditions in markets where financing is already constrained—potentially extending high interest rates and affecting almost every country, business and household.”

The United States must endlessly refinance waves of maturing Treasuries to cover a massive fiscal deficit and national debt approaching $39 trillion. On top of that, global companies leading a new industrial revolution are expected to require trillions of dollars in new funding to expand AI infrastructure.

The time is also coming for many global companies that borrowed at low rates during the COVID-19 pandemic to refinance their debt. With demand for capital surging across the board, if Gulf capital—the most dependable “supplier” of that demand—slows its pace of deployment, market interest rates will face structural upward pressure.

South Korea, which has high dependence on external conditions, is also within the zone of impact. According to the Korea Institute for International Economic Policy (KIEP), eight major Gulf sovereign wealth funds invested a total of $85.1 billion in Asia from 2014 through June 2024.

Of that, South Korea’s share was only 0.9% by investment amount and 0.7% by number of deals. The portion of Middle Eastern capital flowing directly into Korea’s capital markets is negligible. But Korea will face indirect headwinds in the form of “energy inflation” and tighter global financial conditions.

Reporter Kim Joo-wan kjwan@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.