In the end, a toll-ending?…Why stocks jumped on the ‘Hormuz tollgate’ outlook [Bin Nansae’s Wall Street Without Gaps]

Summary

- From the market’s perspective, the most important issue is normalization of the Strait of Hormuz and whether energy flows are restored.

- If a Hormuz toll-collection model is realized, it would give Iran energy-geopolitical leverage and lead to a long-term rise in energy costs.

- If higher energy prices, asset inflation, and a high-rate environment become entrenched, investors should focus on high-quality companies with strong pricing power and robust free cash flow.

Forecast Trend Report by Period

Iran floats ‘joint management’ of Hormuz with Oman

Third-country consortium also envisions ‘bypass tolls’

Stocks rebound despite risk of toll regime being institutionalized

More important than an end to the war: normalizing energy flows

Crossroads: forced reopening, prolonged blockade, or conditional opening

“Just open the strait” — equities’ short-term bet

Postwar risks: high oil, high inflation, high rates

Is this ultimately a ‘toll-ending’? It’s the story of the Strait of Hormuz, held hostage by the war between the U.S.-Israel and Iran.

On the 2nd (local time), Iran’s state news agency IRNA reported that Iran and Oman are drawing up a protocol to jointly oversee the Strait of Hormuz. Iran’s deputy foreign minister Gharibabadi said it was “not to restrict vessel passage but to ensure safe transit and improve services,” but whatever the pretext, it is hard to avoid the interpretation that this is yet another step toward levying tolls. Iran’s parliament on the 30th of last month approved a new management plan that includes a provision to impose tolls on ships transiting the strait.

Iran’s plan to install a ‘tollgate’ on Hormuz—a vital natural strait through which 20% of the world’s crude shipments pass—is, of course, a violation of international law. Many countries, including South Korea, that import Middle Eastern energy through the Strait of Hormuz cannot simply stand by and watch such an attempt. If this continues, Iran could hold the strait hostage even after the war and manipulate the global energy market at will.

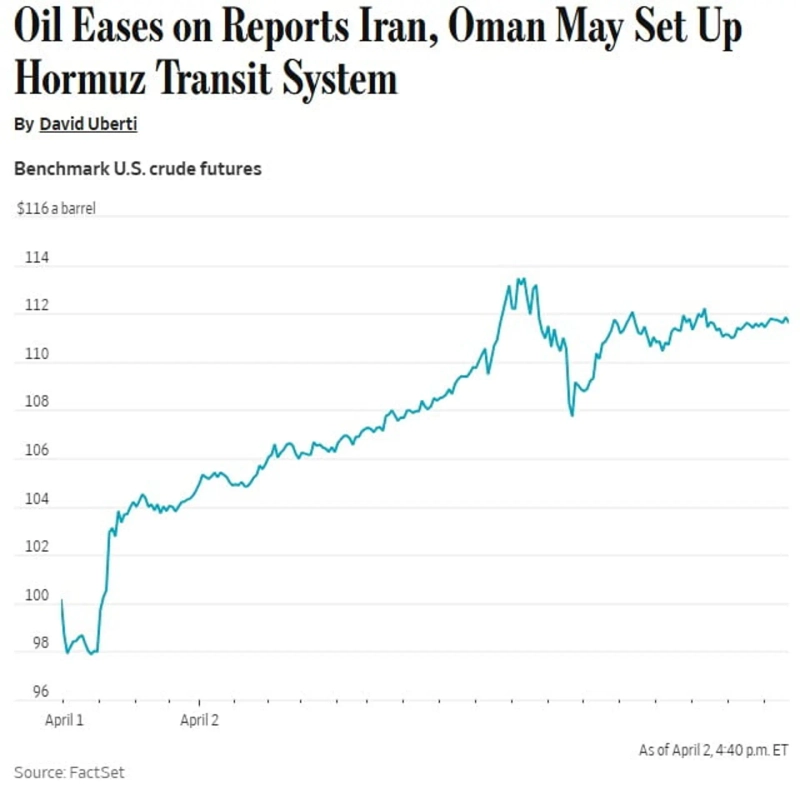

Yet the market staged a sharp rebound as soon as the news hit. The day before, after President Donald Trump’s substance-light address to the nation, hopes for a concrete end-of-war plan faded; global equities plunged and oil spiked. This reversed that in one fell swoop. So why did stocks bounce even under this seemingly absurd scenario of charging tolls on a strait that had enjoyed freedom of navigation? And if a toll model is really put in place, how could it work?

The real endgame isn’t a U.S. pullout—it’s normalization of Hormuz

Since the Iran war broke out, the only thing moving markets has been oil. That’s why, from the market’s perspective, what matters most is not ceasefire/end-of-war headlines, but whether the Strait of Hormuz is actually normalized and energy flows are restored.

The end of the war and the normalization of the Strait of Hormuz are entirely different issues. Reporting on the 31st and 1st of last month that Trump was considering withdrawing without forcibly reopening Hormuz militarily—and Trump’s remarks that seemed to confirm it (“the responsibility for keeping the strait open lies with the user countries”)—reflected this: even as equities rebounded on reduced fears of a prolonged ground war, oil remained elevated.

Goldman Sachs recently said the rebound is driven by positioning and flows rather than fundamentals and is therefore hard to sustain. Hedge funds’ short positions and institutional hedges put on for further downside were unwound all at once, while month-end pension rebalancing and options-market structure amplified a technical bounce. In other words, the market has become more sensitive to good news than bad—not so much “it rose because everything truly improved” as “it snapped back because positioning had become too pessimistic.”

So when could a ‘real rally’ emerge? Ultimately, it hinges on whether the Strait of Hormuz is reopened and oil prices stabilize downward. JPMorgan said “the key variable for markets right now is whether the strait fully reopens,” adding that “given that oil has not fallen meaningfully (despite the recent rally), this bout of optimism is also likely to be temporary.”

Hormuz reopening scenarios

The question is how to reopen the strait in practice. Iran sees the current moment as a ‘once-in-a-lifetime opportunity’ to institutionalize and monetize control of the Strait of Hormuz.

In an interview with Iranian economist Hossein Raghfar (pictured), ILNA reported: “Iran can use this opportunity to neutralize Western sanctions via the Strait of Hormuz and counterattack the U.S. and allies that joined those sanctions as a regional power. It is a special opportunity that must not be missed,” adding that “controlling the strait requires military power, and the costs should be funded by charging tolls.” It also stressed that “if energy prices rise (due to restricting trade through the Strait of Hormuz), it will directly affect the U.S. recession and inflation, which will in turn decisively influence the U.S. stance toward Iran.”

This shows Iran’s thinking that by holding the strait’s choke point and dragging out time, it can win without even negotiating with the U.S. In fact, Iran has drawn up a plan to collect tolls of around $1 per barrel on tankers transiting Hormuz—in Iranian and Chinese currencies or in stablecoins—while allowing passage only for vessels that suit the Iranian government’s preferences.

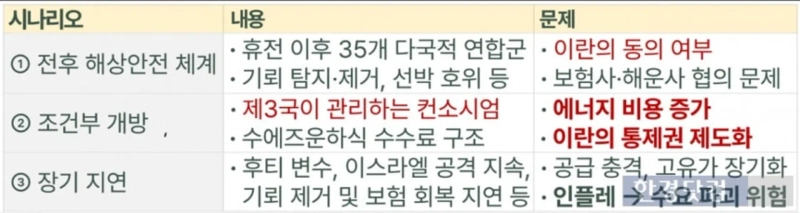

In this situation, there are three broad scenarios for reopening the Strait of Hormuz.

① First, as Trump said, the U.S. strikes Iran hard enough to “send it back to the Stone Age,” forcing Iran to the negotiating table for a ceasefire or an end to the war. After that, a 35-country joint multinational maritime security mechanism led by France is activated. A multinational coalition would normalize shipping traffic by detecting and clearing mines and escorting tankers.

This is the most optimistic scenario and the one most consistent with the current international order. The biggest obstacle is whether Iran, cornered at the cliff’s edge, would actually give up control of the strait.

② The worst-case scenario is that normalization of the strait is delayed for a long time. Many variables could lead to this outcome: the U.S. being tied down longer than Trump intends; Israel continuing attacks even if the U.S. withdraws; or Iran using the Houthi rebels to disrupt the Red Sea and even block the Suez Canal.

The longer the strait stays closed, the longer it takes to normalize supply chains for crude, refined products, chemicals, fertilizers, and a wide range of energy and raw materials. In that case, prolonged high oil from a supply shock would require investors to contemplate risks beyond stagflation—global growth deceleration and, in severe cases, recession.

The Hormuz toll model

③ A recently rising scenario is ‘conditional opening’—restoring freedom of navigation while imposing fees in some form.

Pakistan, which is acting as a mediator between the U.S. and Iran, hosted a meeting of the foreign ministers of Saudi Arabia, Türkiye, and Egypt on the 29th of last month to discuss ideas for reopening Hormuz to propose to Washington. According to Reuters, the meeting produced ideas including a Suez Canal-style fee structure and a neutral strait-management consortium involving the three countries. The proposal is said to have been conveyed to both the U.S. and Iran.

The core of this consortium is to create a framework in which third countries such as Saudi Arabia, Türkiye, and Egypt manage maritime traffic through Hormuz from the front, while Iran agrees to provide security guarantees or ease control—without serving as the direct toll-collection party. In effect, it would be a diplomatic compromise: securing freedom of navigation in exchange for routing massive toll revenues to Iran via the consortium.

China, which had been watching from the sidelines, also moved to mediate. Two days after the trilateral discussions with Pakistan, China jointly announced for the first time a five-point peace proposal with Pakistan. As the largest importer of Iranian crude, China, too, is facing growing economic damage—so severe that a prolonged blockage of the strait has forced domestic refineries to halt operations.

Some also speculate that if the U.S. accepts this plan, it could be structured so that the U.S. also takes a portion of the toll revenues collected by the consortium. That’s because on the 23rd of last month, Trump said, “(the Strait of Hormuz) will probably be controlled jointly by me and Iran’s Ayatollah (supreme leader).”

Of course, all of this remains pure conjecture, and the idea is still at the proposal stage by third countries—not even negotiations. Any arrangement that appears to recognize Iran’s right to collect tolls—by whatever mechanism—would not only violate international law but also, over the long term, hand Iran lasting energy-geopolitical leverage. If tolls are imposed, energy prices would, naturally, be higher than in the era of free navigation.

Even so, militarily reopening the Strait of Hormuz entails enormous risks, so countries are trying to find a diplomatic breakthrough one way or another. That is also why the U.S. is threatening even the possibility of strikes on energy facilities to bring Iran to the negotiating table. Given this context, it is not surprising that a toll model is being discussed in back-channel talks.

Markets: “Just get it flowing again”

Ultimately, a toll-collection model is deeply problematic in that it gives Iran tremendous leverage and drives a long-term increase in energy costs. Nevertheless, if, in the near term, navigation through the Strait of Hormuz is restored in a predictable manner, markets will likely cheer first—regardless of the mechanism. If energy supply flows recover and oil prices fall, worries about inflation, central bank rate hikes, and economic slowdown could fade, and a ‘risk-on’ regime could re-emerge.

That is also the backdrop to why U.S. equities on the 2nd reversed higher even as oil rose. It suggests that the political-level view that “tolls are bad” does not, at least in the short term, carry in markets. It also shows how desperately equities want “energy flows to be unblocked.”

Investors have now entered a phase where they must focus not only on whether the Strait of Hormuz opens, but also on how it opens and what postwar order will be written. Beyond that, even if the strait is normalized, the odds are rising that everything will not return to the prewar state.

In the worst case, if a toll model truly becomes reality, energy costs will be structurally higher over the long run. Even if not, Wall Street has already marked up its average oil-price forecasts for the next year versus prewar levels. Even if the strait were normalized today, supply chains would take time to recover.

Going forward, investors may also face an era in which security takes priority over price and efficiency when procuring energy and raw materials. That implies a larger security premium and higher commodity prices than before. If higher energy prices, asset inflation, and a high-rate environment become entrenched, investors over the long term may need to focus more on high-quality companies with strong pricing power, robust free cash flow, irreplaceable real assets, and monopolistic technologies.

New York=Correspondent Bin Nansae binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.