Why the Won Stays Near 1,500 Per Dollar Despite Korea’s Dollar Windfall

Summary

- Despite a current-account surplus and an export boom in the first quarter, the won-dollar exchange rate has remained in the 1,500s as overseas investment expanded sharply and foreign investors were net sellers of Korean stocks.

- Purchases of US stocks and bonds by pension funds and Korean retail investors, along with companies’ spending on overseas factories and US investment, have kept earned dollars from flowing into Korea’s foreign-exchange market, reinforcing expectations that the weak won will become entrenched.

- Experts are split between the view that the exchange rate could correct on a short-term concentration of flows and the view that, given low potential growth, population aging and continued investment toward the US, entrenched won weakness is unavoidable.

Forecast Trend Report by Period

The Mystery Behind the High Won-Dollar Rate

Old Exchange-Rate Rules Have Broken Down

Export Boom and Stock Rally Fail to Lift the Won

“The Variables Driving the Exchange Rate Have Changed”

Pension Funds and Retail Investors Keep Buying Dollars

Exporters Reinvest Overseas Instead of Bringing Proceeds Home

Even at 1,500, Koreans Remain Strikingly Calm

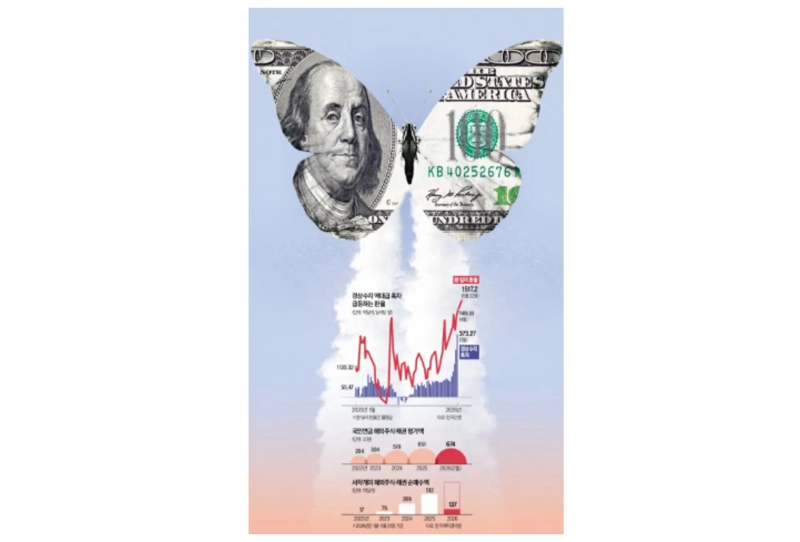

It is a puzzle. South Korea’s won is hovering just above 1,500 per dollar even as domestic companies bring in record export earnings in US currency. Those are levels usually associated with the 1997 Asian financial crisis and the 2008 global financial crisis. Korea’s current-account surplus in the first quarter was four times the level a year earlier. Yet the currency has failed to strengthen during an AI-led export boom, leaving even experts puzzled.

The won finished daytime trading in Seoul at 1,517.2 per dollar on May 22. It has closed above 1,500 for six straight sessions since May 15. That makes 18 trading days this year with a close above the 1,500 level. During the 2008-2009 financial crisis, the won finished above that threshold on only 14 trading days combined. Korea’s sovereign credit-default swap premium, a measure of default risk, stood at 0.2265 percentage point on May 22. That is about one-fifteenth of the crisis peak of 6.99 percentage points on Oct. 27, 2008. The message is that the weak won has little to do with sovereign-risk concerns.

The currency is also moving against the direction implied by Korea’s dollar-generating power. The country posted a cumulative current-account surplus of $73.78 billion in the first quarter, nearly four times the $19.49 billion recorded a year earlier. In the past, numbers like that would have driven the won sharply higher. The old formula of a trade surplus leading to a stronger won is no longer working.

Why is that happening? Market participants say capital flows now matter more than the goods balance, or exports minus imports. Korea’s net financial-account assets — defined here as overseas investment by Koreans minus investment in Korea by foreigners — totaled $65.42 billion in the first quarter. In effect, nearly as many dollars left the country as were generated by the current-account surplus. Rising overseas investment by pension funds and individuals reflects a structural shift tied to an aging population. Companies that are increasingly compelled, or willing, to invest in the US are also keeping their dollars offshore. That helps explain why expectations for a prolonged period of won weakness have been slow to fade.

Foreign investors taking profits have added to the pressure. They have been net sellers of more than 100 trillion won ($72.5 billion) worth of Korean stocks this year, helping drive the exchange rate higher. External headwinds have also lined up against the won, including the prolonged war in the Middle East, surging oil prices, a spike in US Treasury yields and yen weakness.

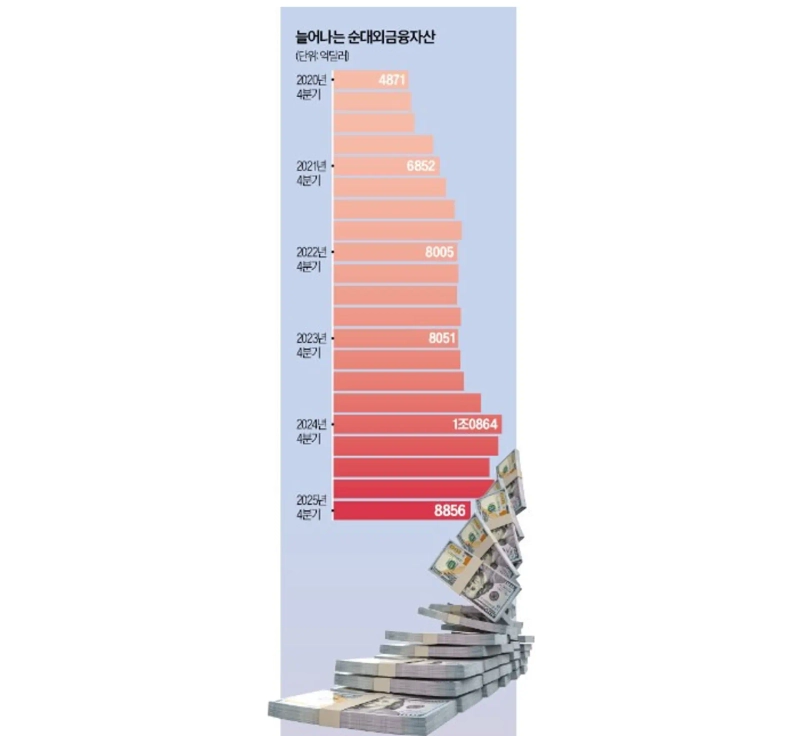

What is even more puzzling is how calm Koreans have remained. There is little broad sense of crisis. One reason is that more people now hold foreign-currency assets. Korea’s net international investment position reached $885.6 billion in the fourth quarter of last year. Investors in US stocks benefit when the exchange rate rises, and domestic equities have climbed enough to limit complaints. The real problem is inflation. If interest rates begin to rise in earnest, vulnerable households will be hit first. The exchange rate captures the condition of the broader economy. It is not a simple issue.

1,500 Once Signaled Crisis. Now It Is Becoming the New Normal as the Trade-Surplus Rule Breaks Down

Six Questions About Why the Won Remains in the 1,500s Despite Record Exports

Exchange rates are difficult by nature. They reflect domestic and global variables in real time, including interest rates, stock markets, growth, inflation and geopolitical risk.

The won-dollar rate has become even harder to explain. Korea’s growth is improving on a semiconductor boom, and the current account is posting record surpluses, yet the currency is trading at levels last seen during the financial crisis. Has a won-dollar rate near 1,500 become the new normal? Here are six questions at the center of that debate.

Q. If Korea is raking in dollars, why is the exchange rate still rising?

Korea’s current-account surplus reached $73.78 billion from January through March. The problem is that the dollars being earned are also leaving the country. Companies are building factories overseas, while pension funds and retail investors continue to increase purchases of foreign stocks and bonds. Net financial-account assets, which include foreign direct investment and overseas securities investment, rose by $65.42 billion in the first quarter from a year earlier.

The expansion in overseas investment is structural. Korean retail investors’ net purchases of US stocks and bonds surged from $1.76 billion in 2022 to $51.21 billion last year. They bought more than $13.7 billion on a net basis through May 20 this year. The National Pension Service has also sharply increased its overseas equity holdings. Their valuation jumped from 2.5662 trillion won ($1.86 billion) in 2021 to 5.7314 trillion won ($4.15 billion) as of the end of February.

Another issue is that dollars earned by exporters are no longer flowing into Seoul’s foreign-exchange market. After the won moved into the 1,400 range in 2022, exporters began increasing the share of foreign-currency assets they hold. The reason was concern that the exchange rate could rise further.

More companies are also building factories overseas or pursuing mergers and acquisitions as global supply chains are reshaped. A pledge made in tariff talks with the US in October last year to invest $350 billion in the US is also weighing on the won. Participants in the foreign-exchange market estimate that commitment alone lifted the won-dollar rate by about 50 won.

Q. Stock prices are rising. Shouldn’t that push the exchange rate lower?

That used to be the case. When stocks rose, the won-dollar rate typically fell because foreign investors buying Korean shares increased demand for the won. Recently, the opposite has happened. As major semiconductor shares surged, foreign investors moved to lock in gains and sold more than 100 trillion won ($72.5 billion) of domestic equities this year. That is roughly equal to the first-quarter current-account surplus. The selling was partly mechanical, reflecting efforts to reduce Korea’s weight in portfolios after the rally. The volume of sales over a short period has had a powerful effect on the won-dollar rate.

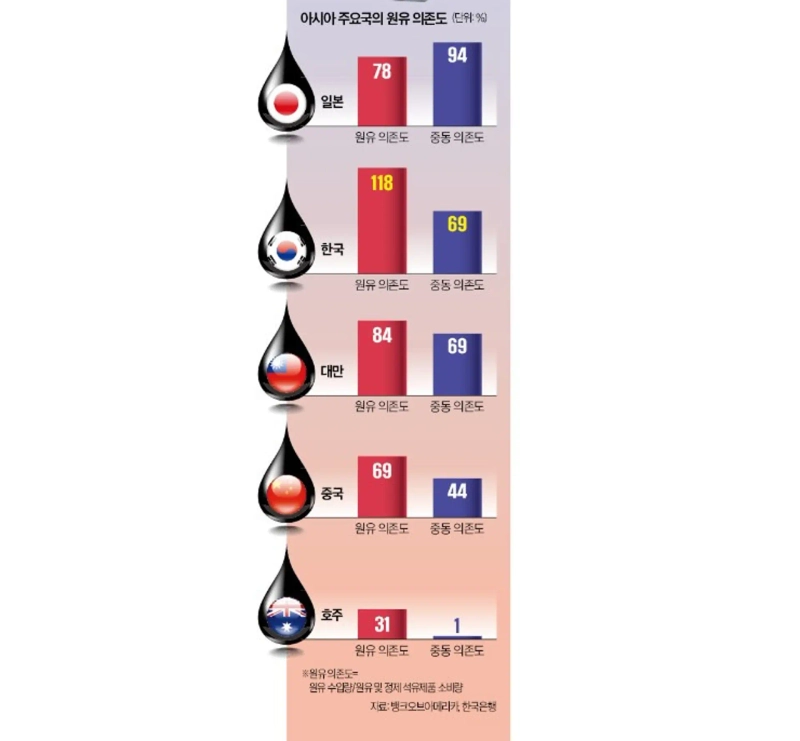

Q. Why does the won weaken when oil prices rise?

Recently, the won-dollar rate has moved in line with global oil prices. That is because crude is essential to Korea’s manufacturing-heavy economy. The country also depends heavily on Middle Eastern oil. When crude import costs rise, they can damage the trade balance of an economy that relies on exports for growth. Bank of Korea data show the country’s oil dependency ratio — crude imports divided by consumption of crude and refined petroleum products — stands at 118%. Dependence on Middle Eastern crude accounts for 69% of that. Since the war began, the dollar index has risen 1.72%, while the won-dollar rate has climbed 5.38%. By contrast, currencies in energy-exporting countries such as Canada and Brazil have been relatively stable over the same period.

Q. The US is sucking in dollars from around the world. How does that affect Korea?

Korea’s benchmark interest rate is currently 2.50%, compared with 3.50% to 3.75% in the US. That leaves a gap of as much as 1.25 percentage points. Global capital chases higher returns, prompting investors to sell won-denominated assets and shift into dollar assets, pushing the exchange rate higher.

Concern over inflation driven by higher oil prices is also sending US Treasury yields sharply higher and putting more pressure on the won. The 30-year Treasury yield briefly climbed to 5.2%. That means investors can earn more than 5% a year in dollars simply by holding US government bonds. With war already fueling haven demand for the dollar, higher yields have made the US a magnet for global dollar liquidity.

Q. Why are Koreans so calm despite the weak won?

One explanation is that household asset structures have changed. Millions of Korean retail investors who stayed up late to buy US stocks have seen their accounts swell as the exchange rate rises. Even if Apple shares are unchanged, returns jump once they are translated back into won.

Another reason is that Korea’s foreign-exchange reserves remain ample, unlike during the 1997 crisis when a shortage of dollars triggered broader turmoil. Reserves stood at $427.88 billion last month. Dollars are also plentiful in domestic funding markets. The additional spread borrowers must pay when borrowing dollars in the foreign-currency funding market — beyond the interest-rate gap between two countries, based on the three-month tenor — was just 0.02 percentage point last month. That means dollars remain readily available for those willing to borrow.

Q. Does this reflect Korea’s fundamentals, or is it a short-term distortion?

Experts are divided. Some view the recent rise in the exchange rate as a short-term concentration of flows. If the Strait of Hormuz remains open in the second half, oil prices fall, and the Bank of Korea raises interest rates, the won-dollar rate could stabilize in the high-1,300 to low-1,400 range.

Others argue that the current level reflects Korea’s underlying economic strength — or lack of it. Since last year, the reasons have changed, from retail buying of foreign stocks to the Middle East war and foreign selling of Korean equities, but the won has remained under pressure. They say the currency reflects weak fundamentals such as potential growth in the 1% range and rapid aging. Ha Geon-hyeong, a researcher at Shinhan Securities, said investment by Korean economic actors into the US would continue. “Entrenched won weakness is unavoidable,” he said.

Shim Seong-mi, Hankyung.com reporter smshim@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.