Wall Street Warns US Stocks Are Overheated as Expected Returns Sink to Lowest Since 2002

Forecast Trend Report by Period

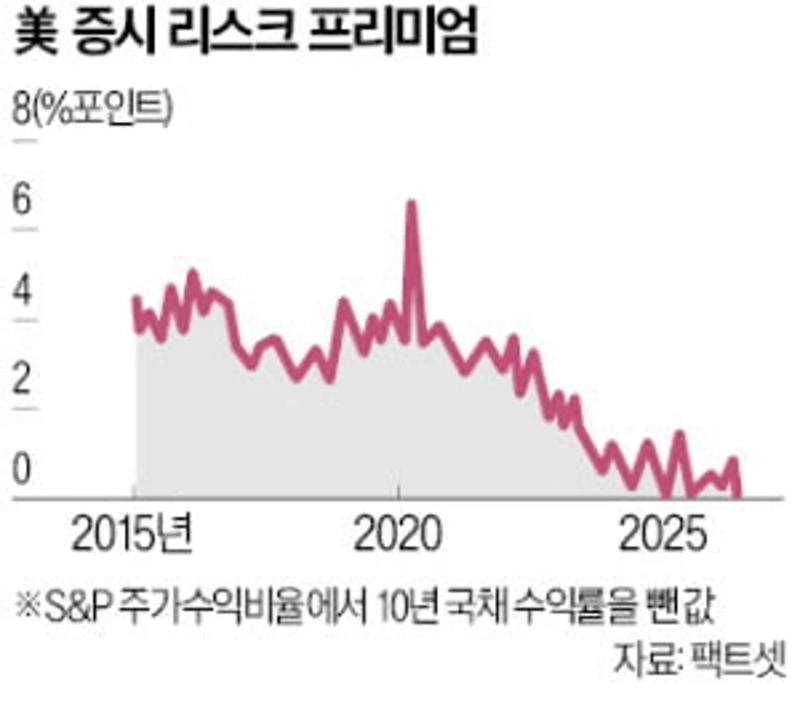

Expected returns on US stocks have fallen sharply, narrowing to a level little different from that of benchmark 10-year Treasuries. The gap has become so small that investors are getting little compensation for taking equity risk.

The S&P 500 equity risk premium, a measure of the index's expected excess return, has traded between 0 and 1 percentage point this year, the Wall Street Journal reported on May 26. After turning negative in early 2025, it has fluctuated below 1 percentage point for more than a year. That is the first time since 2002, when the dot-com bubble began to burst.

The premium is calculated by subtracting the 10-year US Treasury yield from the S&P 500's earnings yield, the inverse of its price-to-earnings ratio. A narrow premium means investing in stocks, a risk asset, is not much more attractive from a return perspective than putting money into Treasuries. Don Calcagni, chief investment officer at Mercer Advisors, said that suggests stocks are overvalued.

A key reason is the rapid rise in the S&P 500's price-to-earnings ratio, led by semiconductor companies. The index is now trading at 21 times projected earnings for the next 12 months, above its 10-year average of 18.9 times. That implies lower expected returns.

Treasury yields, meanwhile, have been rising on inflation linked to the US-Iran war and fading expectations for Federal Reserve rate cuts. The 10-year Treasury yield stood at 4.57% on May 22, up 0.61 percentage point from 3.96% just before the outbreak of the Middle East war in February.

Other indicators also suggest the stock market has entered an overheated phase. The WSJ compared a measure of long-term expected stock returns developed by Nobel laureate and Yale University professor emeritus Robert Shiller with the S&P 500's average excess return over bonds over the past 10 years to assess how stretched the market looks over the medium to long term.

Historically, the two measures moved at similar levels. This year, however, the long-term expected return measure has fallen to 0% to 2%, while the 10-year average excess return measure has climbed into the 10% range. That underpins the view that recent gains will be hard to sustain.

The market is increasingly warning that stock returns ahead may be weaker than they have been so far. Jeff Buchbinder, chief equity strategist at LPL Financial, said the market's current overvaluation would be difficult to sustain unless both rate cuts and corporate earnings growth are confirmed.

Hwang Jung-soo, Korea Economic Daily reporter hjs@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.