Chip Boom Drives Record Kospi, $250 Billion Current-Account Surplus as Households Struggle

Summary

- The Kospi index and current-account surplus are expanding to record levels on the back of a semiconductor supercycle and an export boom.

- Even with high interest rates, stocks and bond yields are rising in tandem, lifting expectations for faster economic growth, stronger nominal growth, and higher tax revenue, while polarization and pressure on household finances worsen.

- Surging long-term card-loan delinquencies, nonperforming loans, insurance cancellations, and personal and corporate bankruptcies are making K-shaped polarization a growing risk to a recovery in domestic demand and to vulnerable borrowers.

Forecast Trend Report by Period

Bull Market in a High-Rate Era: Golden Bell or Warning Bell?

Markets Enter an Age of ‘Mega Forces’ in the AI Shift

Old Rule That Higher Rates Sink Assets Is Breaking Down

Companies Pour Money Into AI and Other Big Bets to Survive

That Spending Is Emerging as a Powerful Engine of Growth

Kospi Hits Record, Growth Outlook Revised Up

But Card Delinquencies Jump and Income Polarization Persists

High interest rates have long been seen as the enemy of stocks. Warren Buffett once described rates as gravity pulling down asset values. This year looks different. Bond yields and stock prices are rising at the same time in South Korea, the US and Japan.

Views are split. Optimists say a new narrative is taking hold. In the AI era, returns from large-scale investment may outweigh the drag from higher borrowing costs. Skeptics counter that prolonged periods of high rates have always ended in downturns. The question now is where stocks, already at records despite elevated rates, head next.

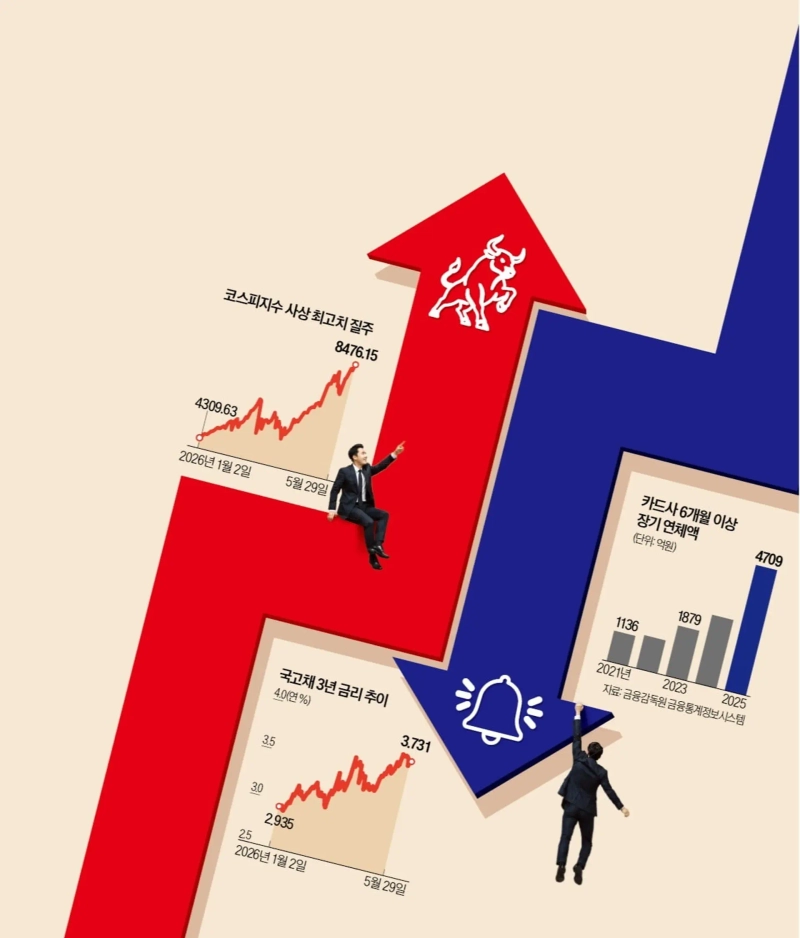

The Kospi hit an all-time high on May 29. It closed at 8,476.15, up 3.55% from a day earlier. The market shrugged off the Bank of Korea after it formally signaled a policy-rate increase on May 28. Stocks have roughly doubled this year, and with the economy showing signs of a rebound, the BOK projects growth of about 3% this year, above its estimate of potential growth at 1.8%. Some also say gross national income per capita could top $40,000 for the first time this year.

Markets are increasingly treating tight monetary conditions not as a crisis but as another opportunity. One interpretation is that high rates reflect economic growth as much as they restrain it. That argument is spreading beyond the US to South Korea, where some say the country, like other hardware powerhouses, has entered a new cycle.

Kim Yong-beom, the presidential chief of policy, described the current environment as not a sign of crisis but the friction and cost of a leap forward. Many in the market argue South Korea has joined the ranks of economies being reshaped by “mega forces,” or large structural shifts, in which productivity gains outpace the rise in rates.

Other financial indicators point the other way. Credit-card delinquencies have climbed to their highest since the 2003 card crisis. Bad loans at banks are at their largest since 2019. Risks also remain. War-driven inflation has pushed benchmark yields in both South Korea and the US to fresh highs almost daily. The won may also be headed for its weakest annual level against the dollar.

Domestic demand remains sluggish, and pressure on ordinary households is growing. South Korea’s income quintile ratio, a gauge of inequality, rose to 6.59 in the first quarter, the highest in five years. Former BOK Governor Park Seung said the country needs to prepare for deepening polarization and imbalances in the shadow of semiconductor-led growth. Investors are now focused on how long the simultaneous rise in stocks and interest rates can last.

Semiconductor Boom Sends Exports and Growth Soaring

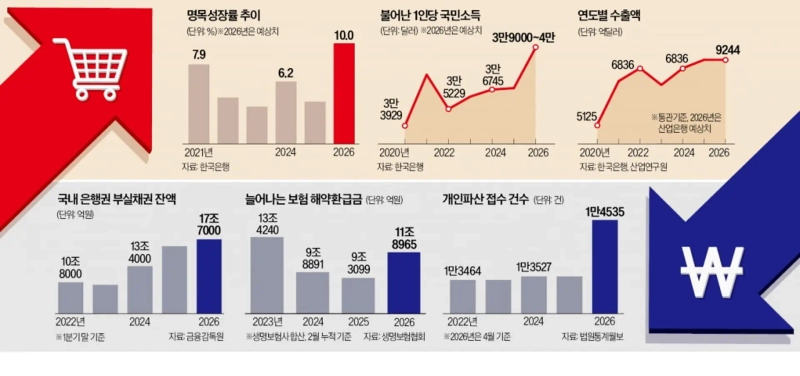

Current-Account Surplus at Record $250 Billion, Nominal Growth Set for First Double-Digit Gain in 24 Years

Foreign investors and international credit-rating firms often view the current account as the key measure of South Korea’s economic fundamentals in its export-led economy. Before past crises, the current account invariably deteriorated. In boom times, the surplus surged. This year, powered by a semiconductor supercycle, the current-account surplus is projected to more than double from last year to $250 billion. Even so, the gains from the chip boom are concentrated among higher-income groups, while sentiment among ordinary households remains weak.

According to the BOK’s economic outlook report released on May 28, South Korea’s current-account surplus is estimated at $250 billion this year. That is about double last year’s record $123 billion. It is also nearly equal to the combined current-account surpluses posted over the past three years, from 2023 through 2025, of $255.6 billion.

The BOK expects the surplus to widen sharply as semiconductor exports surge. The Korea Institute for Industrial Economics & Trade forecasts total exports at $924.4 billion this year, up 30.3% from a year earlier. Semiconductor exports are projected at $350.1 billion, up 101.1%. On that basis, South Korea is poised to overtake the Netherlands and become the world’s fourth-largest exporter after China, the US and Germany.

The export boom is also feeding through to growth and tax revenue. In its optimistic scenario, the BOK projects real economic growth of 3.1% this year, well above potential growth of 1.8%. The government is targeting nominal growth of about 10%. If that materializes, it would be the highest since 2002, when nominal growth was 11%. It would also raise the possibility that gross national income per capita, stuck in the $30,000 range for 11 straight years from 2015 through last year, could surpass $40,000 for the first time.

Government tax revenue is also forecast to reach a record 415.4 trillion won, up 11.1%, or 41.5 trillion won, from a year earlier. The figure reflects 25.2 trillion won in extra tax revenue factored into the supplementary budget compiled in April. With earnings at Samsung Electronics and SK Hynix improving, some expect the tax windfall to swell to about 40 trillion won, roughly 15 trillion won more than estimated when the extra budget was drawn up.

Still, the warmth of the boom has yet to spread across the broader economy. The Ministry of Employment and Labor said average monthly pay for regular workers rose 3.9% in the first quarter from a year earlier to 4.862 million won. Wages for temporary and daily workers rose just 0.7% to 1.767 million won.

The gains from the stock-market rally are also concentrated at the top. The BOK said households in the top 20% by net worth posted average annual capital gains of 2.06 million won between 2020 and 2024. The rest saw gains of just 100,000 won to 410,000 won. That suggests many South Koreans are not benefiting from any trickle-down effect from the semiconductor supercycle and stock-market boom.

Households Cash In Insurance Policies and Face Bankruptcy

Long-Term Card-Loan Delinquencies Jump 84%, Bank Bad Loans Hit Seven-Year High

High interest rates are shaking household finances. Long-term card-loan delinquencies have jumped to their highest since the 2003 card crisis, and more policyholders are cashing out insurance contracts once seen as a last safety net in retirement. As debt-servicing burdens rise for small businesses, bad loans at banks have climbed to their highest in seven years. Economists say this K-shaped polarization is becoming an obstacle to any recovery in domestic demand.

According to the Financial Supervisory Service, long-term overdue balances of six months or more at the country’s eight major card issuers stood at 470.9 billion won at the end of last year. That was up 83.9% from 256.1 billion won a year earlier. It was the largest amount since the 2003 card crisis, when such balances reached 610.8 billion won. Long-term delinquencies are effectively classified as bad debt with little chance of repayment. The data suggest a growing number of borrowers have been pushed to the limit by cumulative inflation and interest burdens.

Delinquencies are also rising among small businesses and the self-employed. In a report on domestic bank bad loans released on May 29, the Financial Supervisory Service said nonperforming loans at banks totaled 17.7 trillion won at the end of the first quarter. That was the highest since 18.5 trillion won in the first quarter of 2019. Corporate nonperforming loans stood at 14.2 trillion won, up 1 trillion won from the end of last year.

Regional banks are showing the most strain. Lawmaker Kang Min-kuk of the ruling People Power Party said the average delinquency ratio at five regional banks — Busan, Gyeongnam, Gwangju, Jeonbuk and Jeju — stood at 1.31% at the end of the first quarter. That was more than triple the 0.40% average for the five major commercial banks. The gap suggests local economies remain trapped in prolonged weakness as regional property markets fail to recover.

More policyholders are also terminating insurance contracts. Refunds paid out by South Korea’s life-insurance industry reached 11.8965 trillion won on a cumulative basis through February, up 27.8% from a year earlier. Those refunds are paid when customers voluntarily cancel their policies. The increase points to a sharp rise in so-called livelihood-driven cancellations as households seek cash to cope with financial stress.

Bankruptcy filings are also mounting. According to the monthly court statistics report, personal bankruptcy cases filed through April totaled 14,535, up 11.4% from a year earlier. That was the highest since 2021, when filings reached 16,956 during the pandemic.

Corporate bankruptcies are rising as well. Filings by companies totaled 859 through April, up 19.6% from a year earlier. That was the highest since the data series began in 2016. The parallel increase in personal and corporate bankruptcy filings points to worsening stress among the self-employed and small and medium-size businesses.

Many economists expect pressure on household finances to intensify. If the current mix of high rates, high inflation and a weak won persists, large-scale delinquencies among vulnerable borrowers could become reality. That would deepen the K-shaped divide in an economy where households, small businesses and the self-employed still form the base of domestic demand.

Kim Ik-hwan, Jang Hyun-joo and Kang Jin-gyu, Hankyung reporters lovepen@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.