South Korean Banks to Cut Overdraft Limits for High Earners as Household Debt Surges

Summary

- Authorities are tightening controls, prompting banks to reduce credit-loan limits for high-income earners on products such as overdraft accounts.

- Unsecured loans rose by 3.4 trillion won last month, emerging as the main factor behind broader household loan growth and prompting calls for preemptive management.

- Measures under review include limits on high-income borrowers with annual income of around 100 million won, caps on professional credit loans, and a waiver of prepayment fees on unsecured loans.

Forecast Trend Report by Period

Mortgage Loan Growth Slows, but Unsecured Lending Jumps

Household Loans Increase by More Than 9 Trillion Won in May

South Korean banks are set to tighten overdraft and other unsecured credit-line limits for high-income borrowers as early as this month after regulators called for stricter household debt controls. The move follows a surge in debt-fueled stock investing that has added to household borrowing. While mortgage loan growth has moderated, unsecured lending is emerging as a new pressure point in debt management.

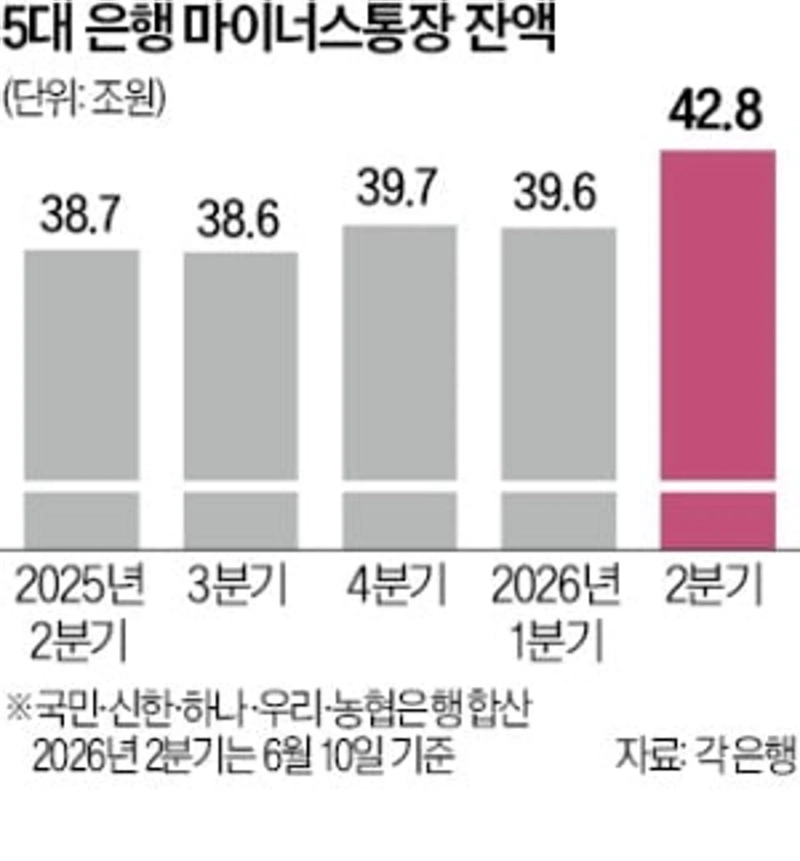

Household loans from financial institutions rose by 9.3 trillion won ($6.7 billion) in May, the Financial Services Commission said on June 11. That was nearly triple the 3.5 trillion won increase in April and the biggest rise since August 2025, when loans increased by 9.8 trillion won. Growth in mortgage loans slowed to 4 trillion won ($2.9 billion) from 5.5 trillion won, while other loans swung to an increase of 5.3 trillion won ($3.8 billion) from a 2 trillion won decline. That was the largest increase in that category since July 2021. Unsecured loans were a major driver, reversing from a 900 billion won decline to a 3.4 trillion won increase.

Banks plan to lower limits on new unsecured lending for high-income borrowers, focusing on revolving credit products such as overdraft accounts that have led the recent increase. They also intend to waive prepayment fees on unsecured loans to encourage repayment of existing debt. Shin Jin-chang, secretary general of the Financial Services Commission, told a household debt review meeting at Government Complex Seoul that this is a point when authorities and the financial industry must fully mobilize to manage household debt. He added that banks need to act preemptively because volatility in unsecured lending could increase.

Overdraft Limits May Be Tightened Starting With Borrowers Earning 100 Million Won a Year

FSC to Check Total Household Lending Weekly; Woori Bank to Halt Platform Loans From June 12

Financial authorities directed banks to tighten oversight of overdraft limits for high earners because unsecured lending has become a new variable in household debt management. Mortgage loan growth has eased, but a buoyant stock market is driving a rapid increase in unsecured borrowing, raising concern that broader controls on household lending could become harder to maintain.

The issue was discussed intensively at a household debt review meeting on June 11 chaired by Shin. Mortgage loan growth slowed, but unsecured lending rebounded by 3.4 trillion won, becoming the main factor pushing up household borrowing. Shin said demand tied to May spending for Family Month and the strong stock market sharply increased other lending, mainly through overdraft credit lines. He said regulators will check each week whether financial companies that failed to meet targets, including total household lending controls, are carrying out their management plans.

Banks are expected to draw up measures as early as this month to manage unsecured lending to high-income borrowers. They currently set credit limits by comprehensively assessing a borrower's income, employer and credit profile. Employees at major companies and licensed professionals typically receive higher limits because their income is viewed as stable and delinquency rates are low.

In the financial industry, annual income of about 100 million won ($72,000) is being discussed as the effective threshold for tighter management. Regulators did not present a specific standard and left details to banks, but lenders are weighing steps such as capping new overdraft accounts for high earners at around 100 million won or lowering the percentage of income used to calculate credit limits. For example, banks that had recognized up to 100% of annual income may cut that ratio to 50% to 70% for high-income borrowers. Professional credit loans for doctors, lawyers and accountants with limits of 300 million won to 500 million won may also be affected. An official at a commercial bank said lenders need to review specific responses on their own and that reducing limits on new overdraft accounts will likely be discussed first.

Banks are also expected to move ahead with waiving prepayment fees on unsecured loans. Raising the bar only for new borrowing would have a limited effect on managing total household lending.

Some banks have already decided to scale back unsecured lending. Woori Bank will suspend new household unsecured loans and refinancing through loan-comparison platforms including Toss, Kakao Pay and Naver Financial starting June 12.

Cho Mi-hyun / Kim Jin-seong, Korea Economic Daily reporters

Cho Mi-hyun (mwise@hankyung.com) Kim Jin-seong (jskim1028@hankyung.com)

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.