From $3,600 to $3.6 Million, Investor in His 40s Shifts Stock and Crypto Gains Into Bonds, ETFs

Summary

- A plans to reallocate the 5 billion won ($3.6 million) built through stocks and crypto assets into a diversified portfolio centered on financial assets excluding real estate.

- He plans to invest across variable annuities, low-coupon bonds, principal-preservation-focused ELBs, domestic and overseas ETFs, time deposits and dollar assets to secure tax efficiency, stable interest income and monthly cash flow.

- The portfolio’s target return is 5.7% to 10% a year, with tax-efficient products, monthly income products and growth-oriented ETFs combined to improve both after-tax returns and long-term asset growth.

Forecast Trend Report by Period

Gangnam Wealth Investment Notes

An Aggressive Investor’s New Dilemma

How to Manage $3.6 Million With Taxes in Mind

Low-Coupon Bonds and ELBs for Stable Returns

ETFs and Dollar Assets for Diversification

A man in his 40s working at an information-technology company amassed wealth over several years through investments in stocks and crypto. He started with 5 million won ($3,600) and grew his financial assets to 5 billion won ($3.6 million) by making aggressive bets on tech shares, growth stocks and cryptocurrencies. As his assets increased, his priorities changed. Instead of pursuing returns while tolerating sharp volatility, he decided he needed a structure that could deliver steadier, more sustainable gains.

His goal was clear: reorganize the 5 billion won ($3.6 million) earned from stocks and crypto into a diversified portfolio centered on financial assets, excluding real estate. Though he had experience with aggressive investing, he now wanted to lower tax burdens, secure steady interest income and monthly cash flow, and still retain exposure to stock-market gains.

Taxes Complicate a Deposit-Only Strategy

Taxes were the main issue. If he put the full 5 billion won ($3.6 million) into time deposits at an annual rate of 3%, he would earn about 150 million won ($109,000) in interest each year. That financial income would be combined with his wage income, potentially increasing his comprehensive income-tax burden. As financial income rises, so does the tax rate, making it difficult to build a portfolio based only on pretax returns.

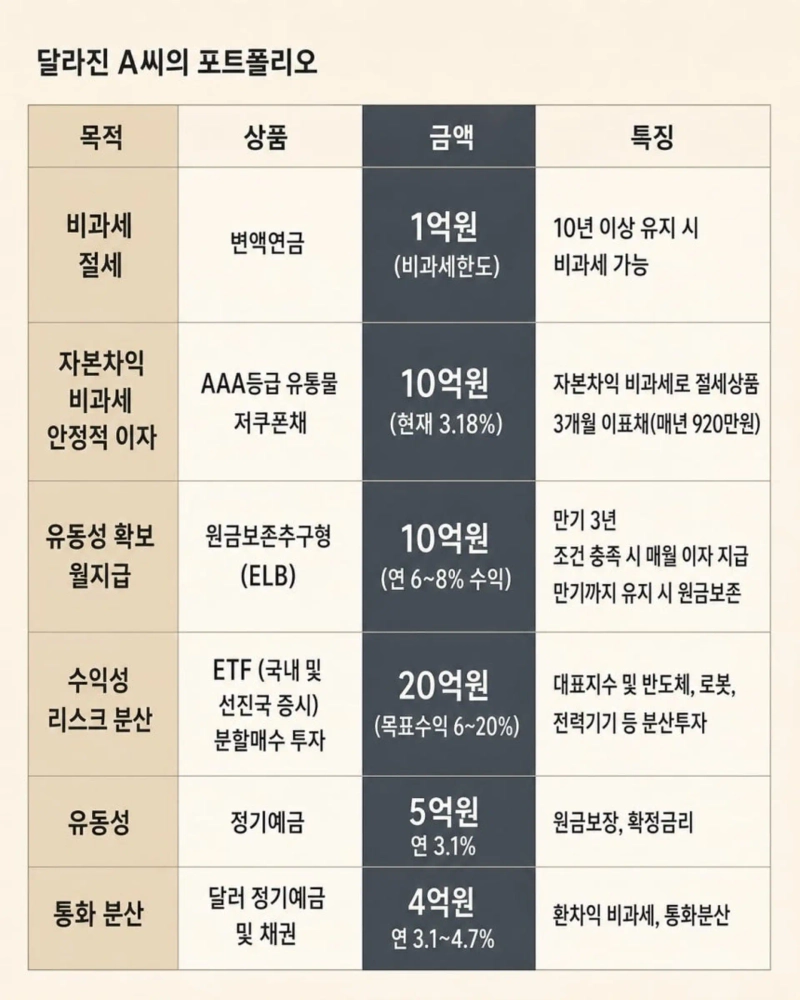

He first allocated 100 million won ($72,000) to a variable annuity for tax planning. The product can qualify for tax exemption if it is held for more than 10 years. He chose a floating-rate structure to prepare for the possibility of higher benchmark interest rates, aiming to combine long-term stability with tax benefits.

For stable interest income, he put 1 billion won ($725,000) into AAA-rated low-coupon bonds bought in the secondary market. Low-coupon bonds generate only a small portion of income through interest payments, while offering the potential for capital gains if bond prices rise. Unlike conventional bonds, they carry a lighter tax burden on capital gains, making them a useful tax-saving tool for wealthy investors. The expected yield is about 3.18%, and the bonds pay interest every three months, providing roughly 9.2 million won ($6,700) a year in coupon income.

He also allocated 1 billion won ($725,000) to principal-preservation-focused equity-linked bonds, or ELBs, to create monthly cash flow. The three-year product is tied to the Kospi 200 and Samsung Electronics. If certain conditions are met, it pays interest monthly, and the structure is designed to preserve principal if held to maturity. Expected returns are 6% to 8% a year.

Domestic and Overseas ETFs to Spread Risk

Domestic and overseas exchange-traded funds are the portfolio’s core assets for returns and diversification. He allocated 2 billion won ($1.45 million) to broad-market and growth-sector ETFs through staggered purchases. The holdings include ETFs tied to semiconductors, power equipment, AI infrastructure, robotics, aerospace, the Kospi 200, the S&P 500 and the Nasdaq 100. The strategy is to reduce volatility by spreading money across several assets with similar growth drivers rather than concentrating on a single stock or asset class.

The ETF allocation reflects expectations for continued growth in global technology shares and the artificial-intelligence industry. Investment by U.S. software companies is continuing, and interest in aerospace and technology stocks more broadly has also increased after a SpaceX listing. He judged that the rally in market leaders and the concentration in semiconductors could continue for some time and chose to diversify across related industries.

For liquidity, he placed 500 million won ($362,000) in time deposits. The allocation secures a fixed annual rate of about 3.1% while preserving principal and maintaining short-term liquidity. It also leaves funds available for additional investment if market volatility rises.

He also added dollar-denominated assets for currency diversification, allocating 400 million won ($290,000) to U.S. dollar time deposits and dollar bonds. Expected returns are 3.1% to 4.7% a year. Dollar assets can offer tax-free foreign-exchange gains and help defend the portfolio when the won weakens.

Balancing Returns and Growth

The portfolio targets annual returns of 5.7% to 10%. If he held only bond products, expected returns would be limited to about 4% to 5%. By combining tax-efficient products, monthly income products and growth-oriented ETFs, he aims to improve both after-tax returns and long-term asset growth.

The market backdrop also supported that allocation. The war between the U.S. and Iran has ended, but major economies have begun raising benchmark interest rates as inflation remains elevated. Higher rates can increase short-term market volatility, but equity assets can also perform when corporate earnings improve. For that reason, the portfolio combines short-term bond products with growth ETFs.

The investor’s portfolio has shifted away from the aggressive positioning of the past toward a structure that weighs tax efficiency, cash flow, growth potential and currency diversification. After building substantial wealth through stock and crypto investments, he now sees stable asset management as more important than short-term price swings.

Lee So-young, a Gold PB executive director at Hana Bank’s Gold Club Bundang PB Center, said that in a period of heightened uncertainty, what matters is not the speed of chasing returns but the balance needed to respond to change. Investors should manage assets by tracking the direction of liquidity shaped by interest rates, inflation, the sustainability of corporate earnings and shifts in global policy, rather than focusing only on short-term stock moves.

Cho Mi-hyun, Hankyung reporter (mwise@hankyung.com)

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.