China’s CXMT Targets Memory Top Tier With $8.1 Billion IPO Valuing It at $80.8 Billion

Forecast Trend Report by Period

CXMT to raise 57.9 billion yuan in Shanghai STAR Market listing

Funds to go toward G5 and HBM3 development, capacity expansion

Targets 20% bit-share by 2035

China’s largest DRAM maker, ChangXin Memory Technologies Inc., is using a blockbuster initial public offering to push into the top ranks of the global memory market. The company is concentrating investment on next-generation process technology and high-bandwidth memory, or HBM, while planning to triple production capacity in a bid to move beyond the 15% market-share threshold the industry views as critical for long-term survival.

CXMT will take subscription orders from retail and institutional investors on July 16 and is scheduled to list on Shanghai’s STAR Market on July 27. The offering price was set at 8.66 yuan a share, implying proceeds of about 57.9 billion yuan, or roughly $8.1 billion, before any greenshoe exercise. The company’s post-listing market capitalization is projected at about 579.2 billion yuan, or roughly $80.8 billion. The listing comes a decade after construction began on its fabs.

The proceeds will fund development of the next-generation G5 process, 12-layer HBM3 and new production facilities. CXMT plans to expand monthly wafer capacity to 420,000 by 2027 from about 320,000 now. It is building new fabs in Shanghai and Beijing and setting up a large production cluster in Hefei.

The company also plans to double capacity by 2030 and triple it by 2035. Its product mix is shifting from commodity DRAM to higher-value chips, with LPDDR5 and DDR5 projected to account for about 75% of output. Global manufacturers have already begun sourcing the company’s DRAM for PCs and servers.

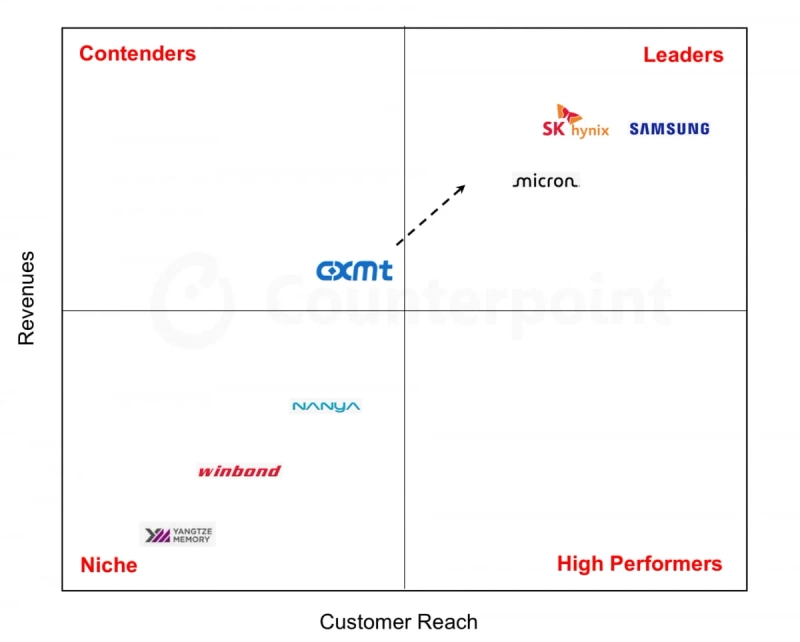

Aiming to join the memory big three

CXMT currently holds a 9% share of global DRAM bit shipments, according to Counterpoint Research. Counterpoint projects that figure will rise to 11% by bit shipments and 9% by revenue in 2028. To break into the leading group dominated by Samsung Electronics Co., SK Hynix Inc. and Micron Technology Inc., the company needs to lift market share to at least 15% to 17%, the research firm said.

“Taiwanese DRAM makers in 2008 saw their market share fall below 15%, failed to secure the funding needed for next-generation fab investment, and eventually dropped to around 3%, becoming niche players,” Hwang Min-seong, research director at Counterpoint Research, said. “Fifteen percent is the line CXMT must cross, and every investment now under way is part of the race to reach that goal first.”

Counterpoint said a key long-term marker will be whether CXMT can reach a 20% share of bit shipments and a 15% share of revenue by 2035. If capacity expands as planned, the company could narrow the gap with established leaders.

Investors are also watching whether the company’s valuation will be rerated. Hwang said the key question is whether a rise in CXMT’s stock price will prompt a broader reassessment, or whether the DRAM industry is already at a cyclical peak and that has already been reflected in the elevated market values of global leaders. The gap remains wide, but the pace at which CXMT closes it after this fundraise will be critical.

HBM output and overseas customers are key variables

The first major test for growth after the listing is HBM. CXMT is developing 12-layer HBM3, but its ability to mass-produce the chips at stable yields has yet to be proven.

Counterpoint estimates CXMT could generate about $2 billion in HBM revenue by 2028, helped by rising production of Huawei Technologies Co.’s Ascend AI chips. Chinese companies including Cambricon Technologies Corp. and Biren Technology are also evaluating CXMT products, the report said.

Winning customers outside China is another challenge. CXMT entered the PC supply chain in mid-2025, and whether that leads to large supply contracts will help determine how quickly it expands market share. Supplying Apple Inc. was cited as another variable that would require political approval.

“Recent market-share gains by CXMT, combined with Apple lobbying, broader global export growth and an impending entry into the HBM market, mean the conditions for growth are falling into place,” Neil Shah, a vice president at Counterpoint Research, said. Tighter US restrictions and an HBM business that has not yet been proven in mass production remain factors weighing on valuation comparisons with rivals, he added.

US restrictions on semiconductor equipment exports will also shape CXMT’s growth path. Tougher rules could make it harder to secure advanced tools and overseas customers. With access to cutting-edge lithography equipment constrained, CXMT is accelerating development of new memory architectures such as vertical channel transistors, or VCT, and wafer-on-wafer bonding.

“Paradoxically, restrictions on CXMT could become an opportunity for it to overtake incumbent leaders,” Shah said. Existing players may be slower to adopt such innovations because they need to protect returns on their installed equipment, he said. “CXMT could turn the constraint of export controls into a catalyst for narrowing the gap and surprise its competitors.”

Hong Min-seong, Hankyung.com reporter, mshong@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.