BOK Raises Rate to 2.75%, Cites Semiconductor Prices as Key Gauge for Further Tightening

Forecast Trend Report by Period

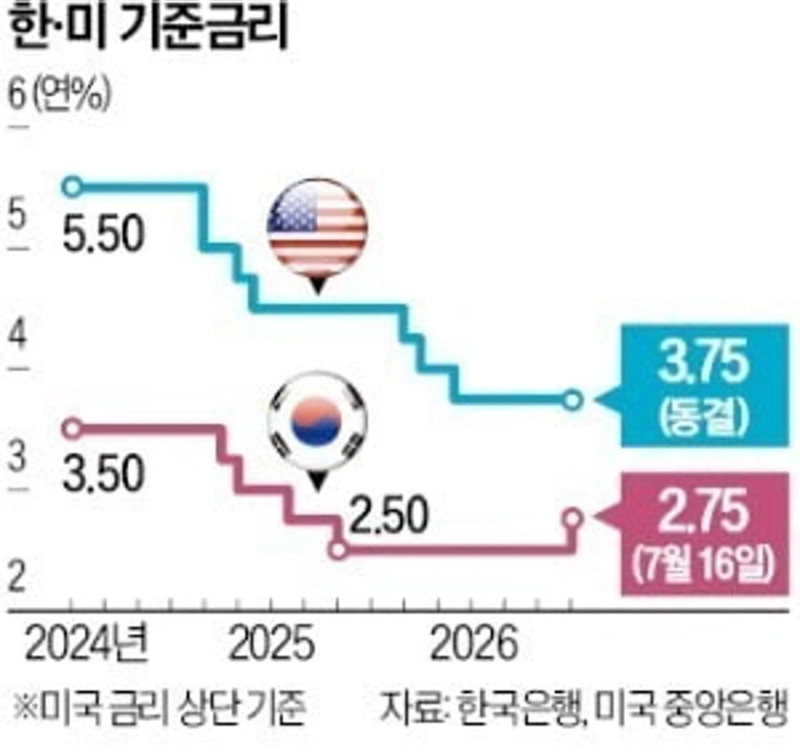

Benchmark rate raised to 2.75% from 2.50%

"Tightening bias to continue"

BOK turns back to tightening after 3 1/2 years

Shin Hyun-song signals more hikes until inflation cools

Korea-U.S. rate gap narrows to 1 percentage point; won strengthens to 1,480 per dollar

The Bank of Korea raised its benchmark interest rate by a quarter point to 2.75% from 2.50%, shifting monetary policy back to tightening for the first time in 3 1/2 years. The move came as the central bank judged that growth remains solid on the back of a semiconductor boom while inflation is still well above target.

The BOK's Monetary Policy Board decided at its July 16 meeting to lift the benchmark rate by 0.25 percentage point. All seven board members supported the increase. "Growth, inflation and financial stability are all pointing toward a rate hike," the board said. In its policy statement, the BOK said it needs to maintain a tightening bias, formally signaling the start of a full tightening cycle.

Inflation concerns were the main driver of the shift. Consumer-price growth accelerated to 3.2% in June from 2.0% in February. The BOK expects elevated inflation to persist for some time, citing higher global oil prices stemming from the U.S.-Iran war, which it said would feed through to domestic prices with a lag. The central bank also said the semiconductor boom will stimulate domestic demand and add to price pressures. Governor Shin Hyun-song said board members agreed that demand-side inflation pressures should not be overlooked.

At the same time, the economy has maintained solid growth. The Ministry of Economy and Finance raised its 2026 growth forecast for South Korea by 1 percentage point to 3.0% in its second-half economic strategy released on July 14. The BOK also said on July 16 that this year's growth will far exceed the 2.6% forecast it presented in May. That has strengthened the case for the central bank to focus on price stability.

Asked how long the tightening bias would remain in place, Shin said the BOK would keep responding until it is confident inflation will converge stably to the 2% target.

On the timing of any additional increase, he said all options remain open. The won-dollar exchange rate ended daytime trading at 1,480.4 won per dollar on July 16, down 4.3 won from the previous session. As the Korea-U.S. interest-rate gap narrowed to 1 percentage point for the first time in 3 1/2 years, the won briefly strengthened to 1,479.2 per dollar during the session.

Semiconductor boom keeps growth firm as stronger domestic demand adds to inflation pressure

Shin says July living-cost data will be closely watched; market sees another hike in October

Shin said after the Monetary Policy Board's July 16 decision to raise the benchmark rate by 0.25 percentage point to 2.75% that "if there is one indicator we need to watch, it is semiconductor prices." Chip prices, driven higher by a global supply shortage, are likely to have a decisive effect on both South Korea's growth and inflation for some time, meaning monetary policy will also hinge on them.

"This year's growth will be well above 2.6%"

The BOK began its tightening cycle on July 16 by raising a benchmark rate that had been held at 2.50% for one year and two months since May 2025. It was the first increase since January 2023, marking a policy pivot after 3 1/2 years. The main factor, Shin said, is the faster pace of growth driven by the semiconductor boom. "From today's perspective, this year's 2.6% growth forecast presented in May is too low," he said. "It will be revised up significantly at the August monetary policy meeting."

Second-quarter GDP data due next week are also forecast to come in well above the BOK's estimate of 0.2% growth from the previous quarter. Some projections put the figure as high as 0.5%. The BOK said the output gap may turn positive sooner than previously expected as strong growth continues. Shin said the central bank had projected in May that the GDP gap would turn positive in early next year, but recent developments suggest that could happen somewhat earlier.

The central bank also expects the semiconductor upcycle to revive domestic demand and intensify inflation pressure from the demand side. The BOK sees a chain in which the chip boom boosts corporate tax revenue and performance bonuses, leading to greater fiscal spending, stronger consumption and higher prices over an extended period. Shin said underlying inflation pressure could be stronger and last longer than previously expected, adding that the tightening bias needs to be maintained.

He also said monetary tightening remains necessary from a financial-stability standpoint, including for the exchange rate and household debt. "Expectations for home-price gains in the Seoul metropolitan area remain alive, and the exchange rate is still high enough to affect import prices," he said.

Bond yields fall

"Semiconductor prices were ultimately the reason gross domestic income could grow as much as 13.2% in the first quarter," Shin said. "If semiconductors become a key part of infrastructure building in the AI era, chip prices could become a highly meaningful indicator for the Korean economy's long-term growth trend." He added that semiconductor prices should also be closely watched in setting monetary policy. If gains in chip prices persist for a prolonged period, the tightening cycle could last longer than expected.

On whether the BOK will raise rates again in August, a key focus for markets, Shin said all options are open and decisions will be based on data. He specifically cited second-quarter GDP figures due next week and July inflation data due in August. "We will look at whether GDI growth moderates from the first quarter or remains supported by exports," he said. "We will also pay close attention to core inflation and living-cost inflation in the July consumer-price data." He added that several upcoming meetings would be "live meetings," meaning policymakers will decide rates based on incoming data rather than a predetermined conclusion.

After the board meeting, markets increasingly bet on one more rate increase in October. Yoon Yeo-sam, a team head at Meritz Securities, said the BOK is likely to hold rates steady in August because July inflation will probably stabilize on lower oil prices even if second-quarter growth remains strong. Reflecting that view, the yield on South Korea's three-year government bond fell 0.018 percentage point to 3.848% on July 16.

Shim Sung-mi, Korea Economic Daily reporter smshim@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.