Coin Taxation: Deferred, Not Ended

Summary

- Taxation on virtual asset income has been deferred until 2027, but with system improvements and enhanced international cooperation, its implementation is becoming more likely.

- The Korean government is building an infrastructure for the OECD CARF MCAA system to automatically exchange virtual asset transaction information.

- Once virtual asset taxation becomes a reality in 2027, it could negatively impact virtual asset prices through weakened investor sentiment and increased profit-taking, so investors should exercise caution.

Taxation on virtual asset income has been postponed until 2027 due to insufficient legal grounds and lack of investor protection measures, but as systems are improved and international cooperation increases, the possibility of implementation is growing. In particular, with the push for tax fairness and participation in the OECD information exchange system (CARF MCAA), the government is ramping up infrastructure development.

[Asset Management Consulting]

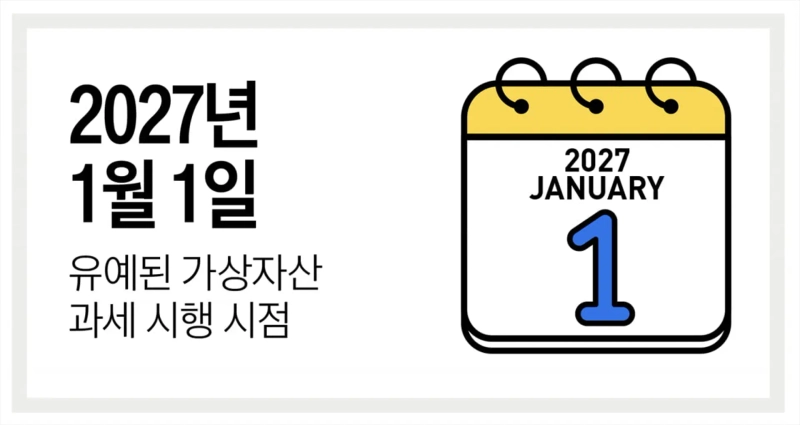

In December last year, the National Assembly passed an amendment to the Income Tax Act that postponed the implementation of taxation on virtual asset income to January 1, 2027, a two-year deferral. While the highly contentious financial investment income tax was abolished, taxation on virtual assets was delayed by two years by agreement between the ruling and opposition parties.

It has become common for younger generations, who have difficulty owning real estate assets, to make “all-in” investments in stocks and coins. Politicians had no choice but to worry about their negative public opinion and contraction in the capital markets. Though they found a brief respite, this was only a temporary deferral of tax, not the end. At this point, let’s examine why taxation on virtual asset income is necessary, its potential issues and countermeasures, and points for investors to note, one by one.

No taxation where there is income?

Mr. A, who worked at a major corporation, invested ₩15,000,000 in Bitcoin and Ethereum in January 2020 at the recommendation of a colleague, made over ₩3,000,000,000 in a year and a half, and quit his job (The Korea Economic Daily, October 7, 2022). Yet, Mr. A likely paid no tax on more than ₩3,000,000,000 of income. Isn’t that odd? Taxation must be based on the law—this is the “principle of statutory taxation.” There is also a “tax equity principle” which requires people earning the same income to be taxed equally, but the Korean Income Tax Act takes a “source of income principle,” meaning there is no choice but to tax only if the law specifically identifies the income source.

Of course, before there was an explicit basis in law, the tax authorities attempted to tax coins. For example, Bithumb Exchange was taxed hundreds of billions of won on the grounds that the income paid by Bithumb Exchange to foreigners (non-residents) was income from transferring “domestic assets” as defined by the Income Tax Act, and Bithumb Exchange should have withheld and paid the income tax. However, the court ruled that since virtual assets are not managed on a central server containing transaction information but rather on computers worldwide connected to the blockchain network, they cannot be considered “domestic assets” and canceled the tax imposition.

Eventually, after such controversy, at the end of 2020 the government defined virtual asset income as miscellaneous income and created a system to separately tax the capital gains by deducting acquisition costs and incidental expenses from the sales proceeds, then applying a basic deduction of ₩2,500,000 and a 20% tax rate to the taxable base. In short, after trading coins for a year, profits exceeding ₩2,500,000 are subject to a 20% tax. It was natural for investors to strongly resist this. While the stock market is subject to strict management for investor protection and disclosure under the Capital Markets Act, which can justify corresponding taxation, it was argued that taxing virtual assets—without investor protection—was unjustified.

Proper taxation of virtual assets presumes transaction information is provided to tax authorities. Since the authorities cannot obtain transaction information from overseas exchanges, only domestic exchange users would be taxed, raising concerns about a mass exodus to foreign exchanges and resulting capital outflows. Thus, the implementation was initially postponed to January 1, 2025, but at the end of last year, with the rollback of the financial investment income tax, the taxation of virtual asset income was deferred again, now until January 1, 2027.

High Likelihood of Taxation from 2027

The government, conscious that investor protection is not yet established for virtual asset users, will implement the “Act on the Protection of Virtual Asset Users” (commonly known as the Virtual Asset User Protection Act) from July 19, 2024, imposing obligations on virtual asset service providers for user deposit custody/trust and actual holding of the same type and amount of virtual assets as users. The former requires that the cash users deposit for trading at exchanges be kept in financial institutions such as banks or placed in trust to protect users in case of exchange bankruptcy or embezzlement. The latter is to prevent exchanges from creating “virtual balances” or “Ponzi schemes” by recording only numbers in ledgers without holding actual virtual assets.

Meanwhile, South Korea, Germany, Japan, France, Australia, and 43 other countries officially signed the “CARF MCAA” (a multilateral agreement on the automatic exchange of information on virtual assets) at the OECD Global Forum on November 27, 2024. Under this agreement, virtual asset service providers submit user personal details and transaction information to their respective tax authorities, which then report via the OECD Common Transmission System to share information with each other. The Ministry of Economy and Finance plans to update relevant legislation and negotiate with signatories to ensure smooth information exchange from 2027.

If these prerequisites for virtual asset taxation are met by 2027, the likelihood of taxation on virtual asset income being implemented is high. It should also be remembered that when the Democratic Party pushed for taxation back in 2024, they proposed raising the deduction limit to ₩50,000,000, and a similar compromise may reappear in the future. If taxation materializes, investor sentiment may weaken and profit-taking sell-offs may increase, negatively affecting virtual asset prices, so investors should take caution well before 2027.

Jung Jae-hee, Attorney at Barun Law LLC

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.