Lido V3: A strategy to reclaim 2.7 million ETH [Poplars Research]

Summary

- Lido V3 is presented as a strategy to absorb the 2.7 million ETH that exited and the 70% of ETH that remains unstaked through the stVault, stETH, and Core Pool structure.

- V3 targets native staking, competing LSTs, and the APR Maxi segment by offering customizable risk configurations, optional liquidity, and restaking and leverage strategies—aiming to regain lost share and recover gross profit.

- However, V3’s risk isolation is assessed at about 95%; in extreme scenarios losses can be transmitted to the Core Pool and all stETH holders, making an investment thesis premised on full isolation fragile.

Forecast Trend Report by Period

**

**

Key Takeaways

Lido V2’s standardized design failed to meet the needs of diverse stakers. While the staking market grew 73% from mid-2023, Lido expanded only 34%; the 2.7 million ETH it failed to capture represents an opportunity cost of roughly $20 million per year. Outflows split between native staking (8.5 million ETH) and competing LSTs (4.5 million ETH). Meanwhile, the yield-chasing (APR Maxi) segment used Lido merely as a simple on-ramp into EigenLayer and LRTs, causing Lido to lose the value-added layer. V3 is designed for all three segments.

V3 structurally resolves liquid staking’s core trade-offs. Traditional liquid staking required users to accept a uniform risk pool. Introduced in V3, stVault is a customized staking service in which users choose operators, fee structures, and risk configurations themselves. Users can mint stETH against a vault position to secure liquidity, or run it like native staking without minting.

However, risk isolation has structural limits. Under normal operating conditions, vault risk remains ring-fenced, but in extreme market conditions losses can be transmitted to the Core Pool via a forced rebalancing mechanism. In this sense, V3 is assessed as delivering roughly 95% risk separation.

V3 provides the foundation for Lido to win back the three segments it has missed. Native stakers can retain control without giving up liquidity; institutions can implement asset segregation and compliance frameworks; and yield-seeking users gain composability by using Lido as the base layer. With 70% of Ethereum still unstaked, V3 is a strategic foundation for Lido to regain and expand lost share.

1. Market-share decline during a growth phase

A superficial reading of Lido’s share decline is that rising competition fragmented the market. In reality, the market grew—and the core issue is that Lido failed to capture that growth.

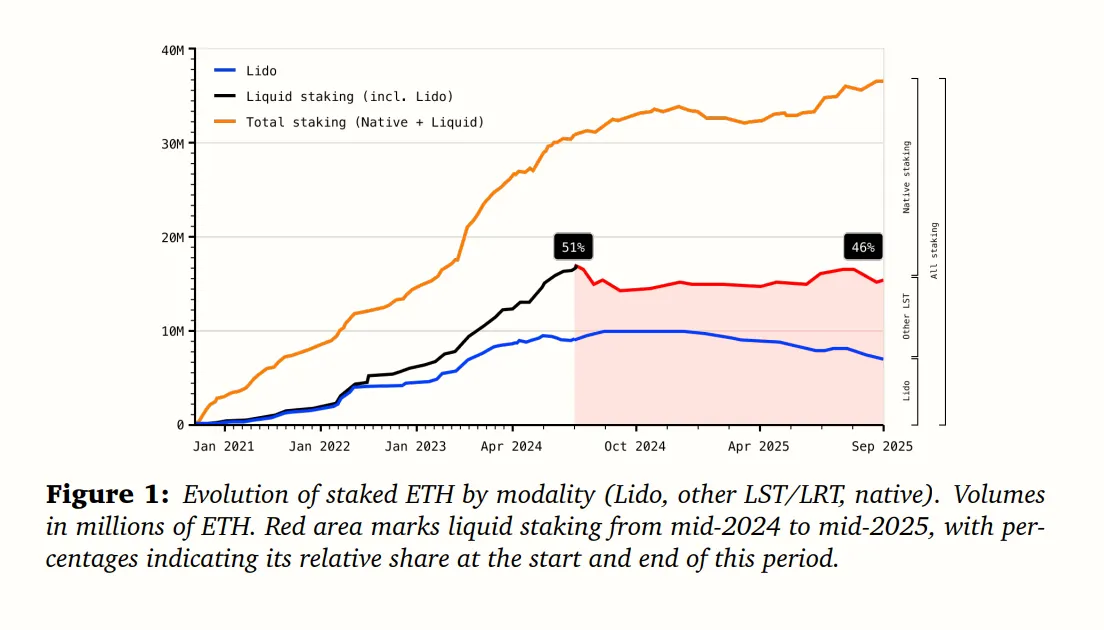

Native staking absorbed 55% of new inflows (8.5 million ETH), driven by solo stakers, institutional custody, and demand for direct validator operations. Liquid staking’s share of total staking fell from 51% in mid-2024 to 46% in mid-2025.

Drivers of outflows differ by segment. Native stakers either did not need liquidity or preferred direct control. Institutional stakers faced different constraints: regulatory requirements often demand operators in specific jurisdictions or operators holding particular certifications. Such requirements are hard to reconcile with V2’s pooled operator model. V3 enables a single-operator configuration while offering the option to mint stETH when needed for DeFi or liquidity management.

Source: Lido V3 whitepaper

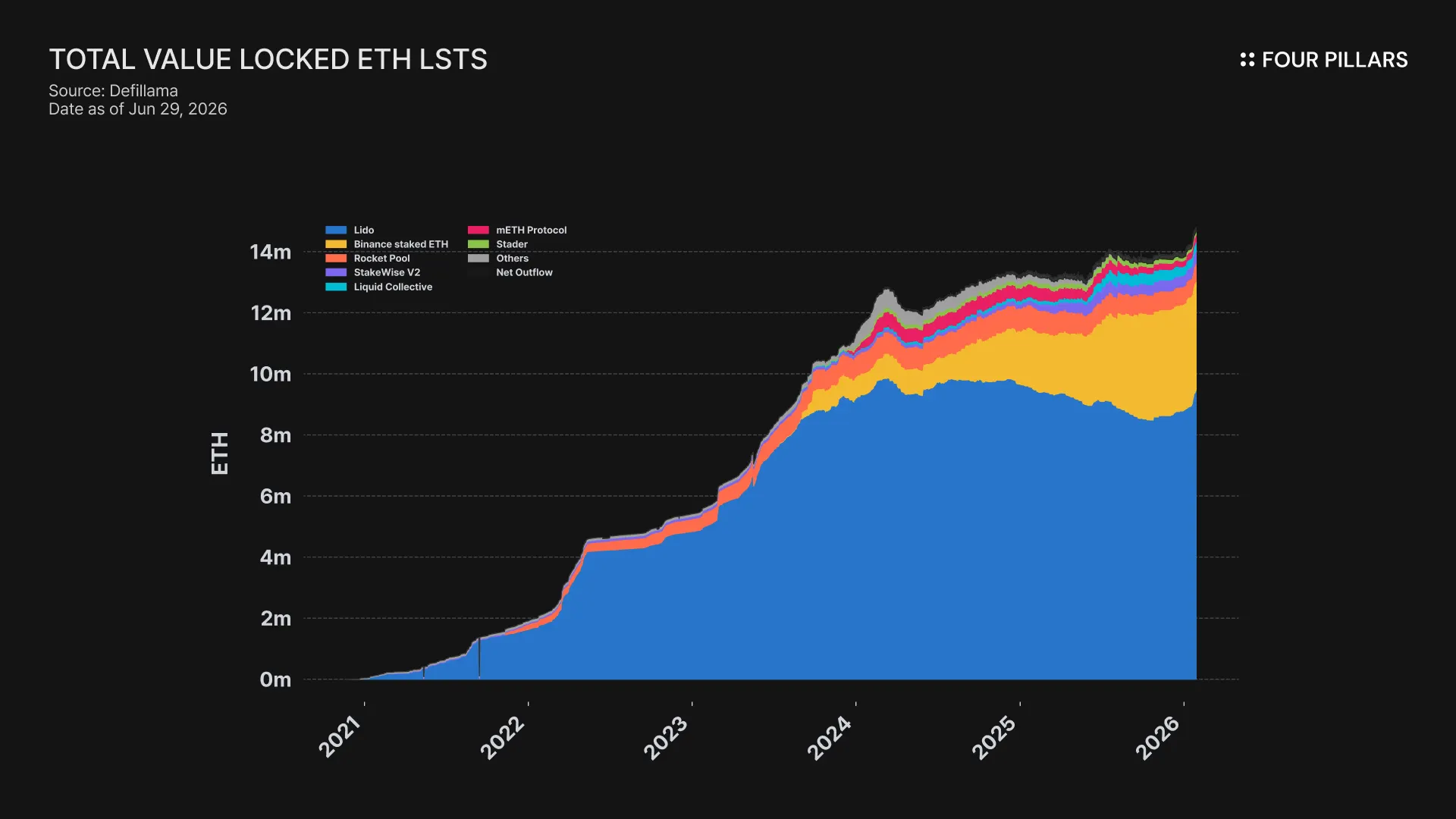

Competing LSTs captured 29% of new staking (4.5 million ETH). Binance staked ETH rose +335%, Liquid Collective +229%, and StakeWise +328%. As a result, Lido’s share within the liquid staking market fell from 90% to 65%.

The yield-chasing (APR Maxi) segment is a separate issue. According to Lido’s Q3 2025 tokenholder update, the APR Maxi segment surged from 2% to 20% of total staking. They did use stETH, but only as an intermediate step rather than the destination—depositing into EigenLayer, wrapping via Ether.fi, and farming points on Renzo. Lido retained the staking layer but lost the upper layers where value accrues.

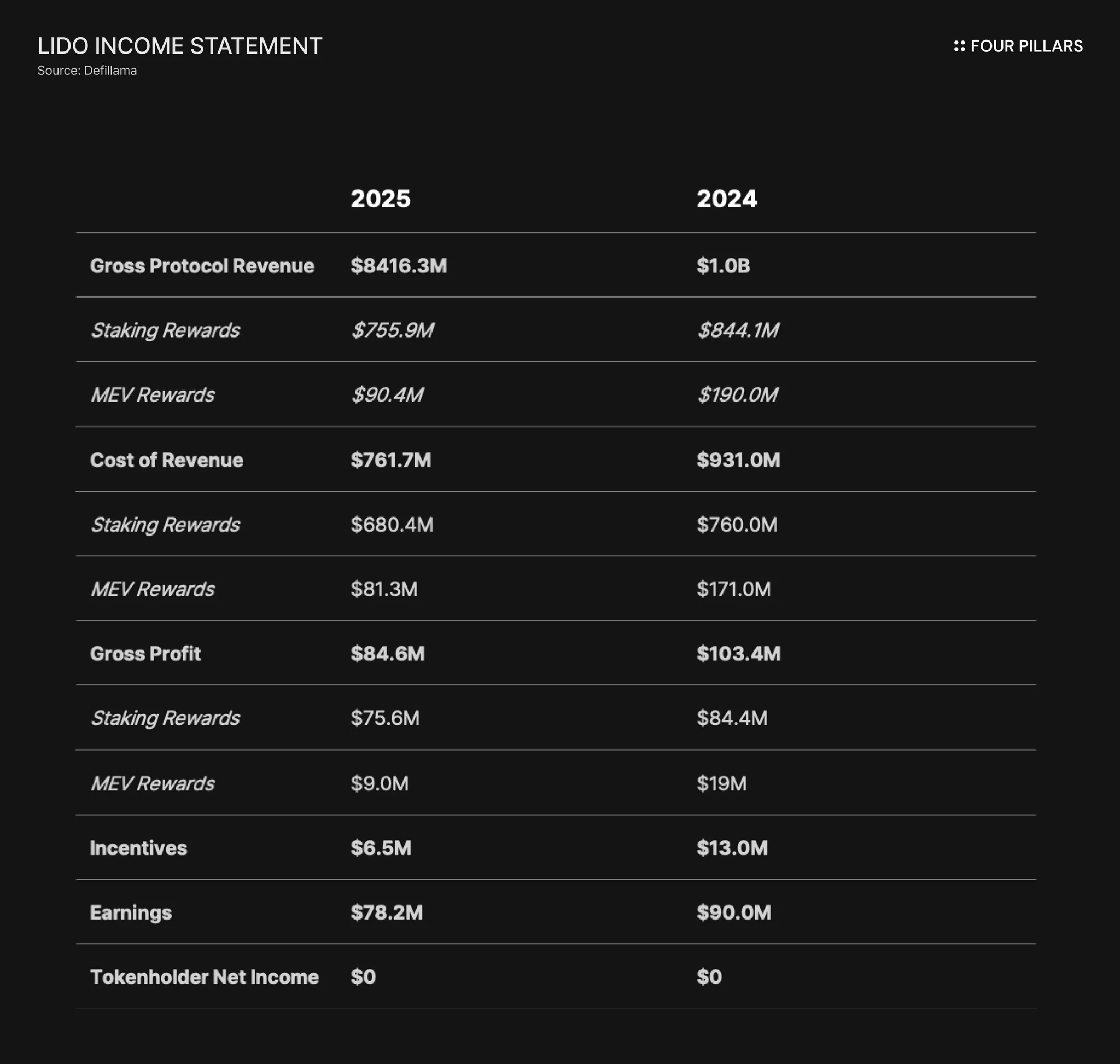

Further worsening the picture is that only 30% of total Ethereum is staked (36.4 million / 120.7 million ETH). With 70% still unstaked, the fact that Lido’s share within the staked 30% has already fallen from 33.5% to 26% implies its foundation is weakening even before a full market expansion begins. The opportunity cost is quantifiable. Had Lido maintained its mid-2023 share, it would hold an additional 2.7 million ETH today—equivalent to roughly $20 million in annual gross profit. In fact, gross profit fell 18% from $103 million in 2024 to $85 million in 2025.

V3 is Lido’s response to these structural issues.

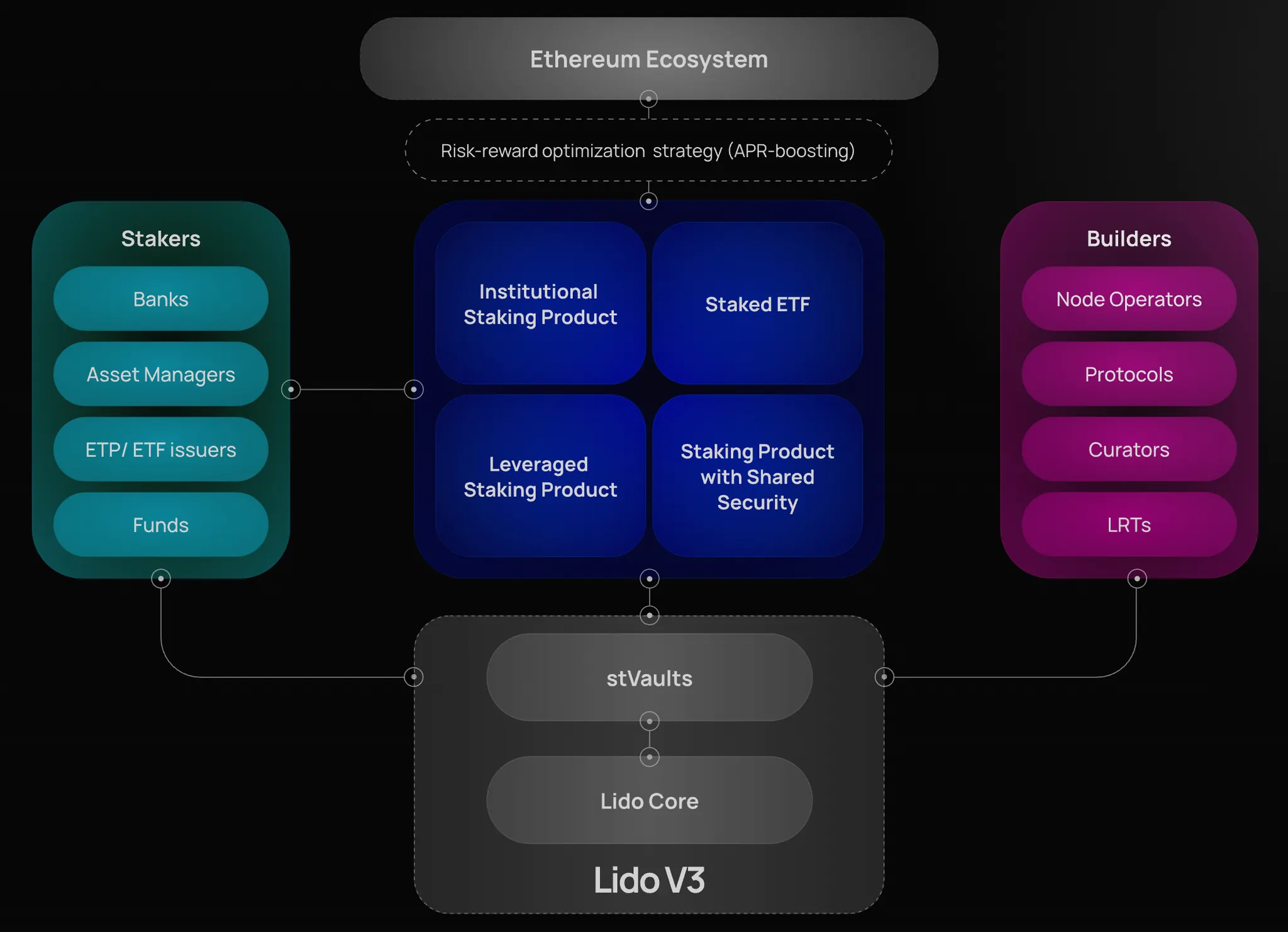

2. V3 technology stack architecture

V2’s architecture worked as follows: deposit ETH, receive stETH, and assets enter a shared pool managed by Lido’s Staking Router. Because all participants shared the same operator set, the same risk exposure, and the same returns, demand for customization inevitably translated into churn—and in practice, millions of ETH exited.

V3 unbundles what was bundled in V2 so that risk and liquidity operate as separate layers. The risk layer, stVault, is a non-custodial smart contract that lets users design their own staking environment. Where Lido set all parameters in V2, users control them in stVault: which operator to delegate to, fee structure, MEV policy and client software, and whether to attach DVT or restaking modules. Crucially, users also retain withdrawal rights. Operators handle only infrastructure operations and cannot access principal; via EIP-7002, users can execute validator exits directly without operator approval, enforcing this structure at the protocol level.

The liquidity layer, stETH, is now optional. Users can mint stETH against a vault position, and issuance follows an overcollateralized design. The reserve ratio ranges from 2% to 50% based on a multi-factor risk assessment framework. DVT-based operators with client diversity can qualify for the minimum 2% reserve ratio, while concentration, operating track record, and operating environment are all incorporated. Higher-risk configurations require higher collateral, reducing the amount of stETH that can be minted.

The Core Pool—V2’s existing mechanism—remains for passive stakers who want simplicity, while additionally serving as the system-wide liquidity buffer and the APR reference rate. All stETH redemptions are designed to route through the Core Pool first, preventing arbitrary liquidation of stVault positions, and stVault fees are computed with reference to Core Pool APR, limiting operators’ ability to game performance metrics.

At launch, the cap on stVault scale is set at 30% of the Core Pool, and is expected to expand as the mechanism is validated.

3. Strategy to capture the three segments

The native staking segment—55% of new staking inflows—chose not to use liquid staking tokens. V3’s value proposition for them is an optional liquidity layer usable only when needed, on top of everything direct staking offers. Because stVault supports full operator configuration, EIP-7002-based execution-layer exits, and MaxEB auto-compounding for up to 2,048 ETH validators, not minting stETH makes it effectively equivalent to running native staking with improved tooling.

Source: https://v3.lido.fi/

The institutional segment is where competing LSTs have grown fastest, with Binance staked ETH up +335% and Liquid Collective up +229%. Their core value propositions were asset segregation, compliance, auditability, and explicit operator agreements. V3 is addressing this demand via Northstake and P2P.org. Northstake is building a Staking Vault Manager for regulators, with multi-vault consolidated management API/SDK, clear asset attribution, audit trails, and a full compliance framework; P2P.org is launching a Dedicated Vault with similar institutional control features. However, whether Lido can attract capital away from Binance is likely to depend more on sales execution than on architecture.

The APR Maxi segment is the group Lido retained technically but failed to monetize. Because they used stETH only as an input to EigenLayer, Ether.fi, and Renzo, returns accrued to the restaking and LRT layers.

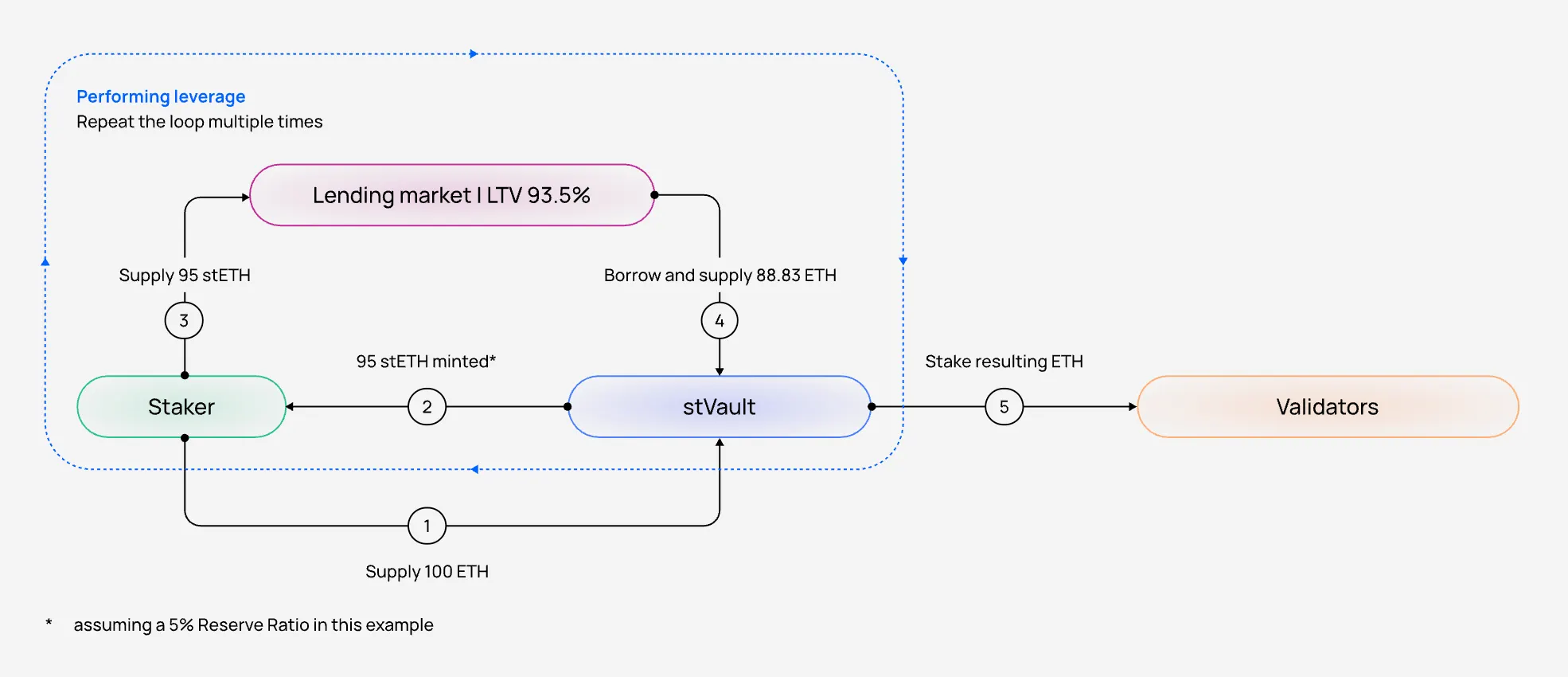

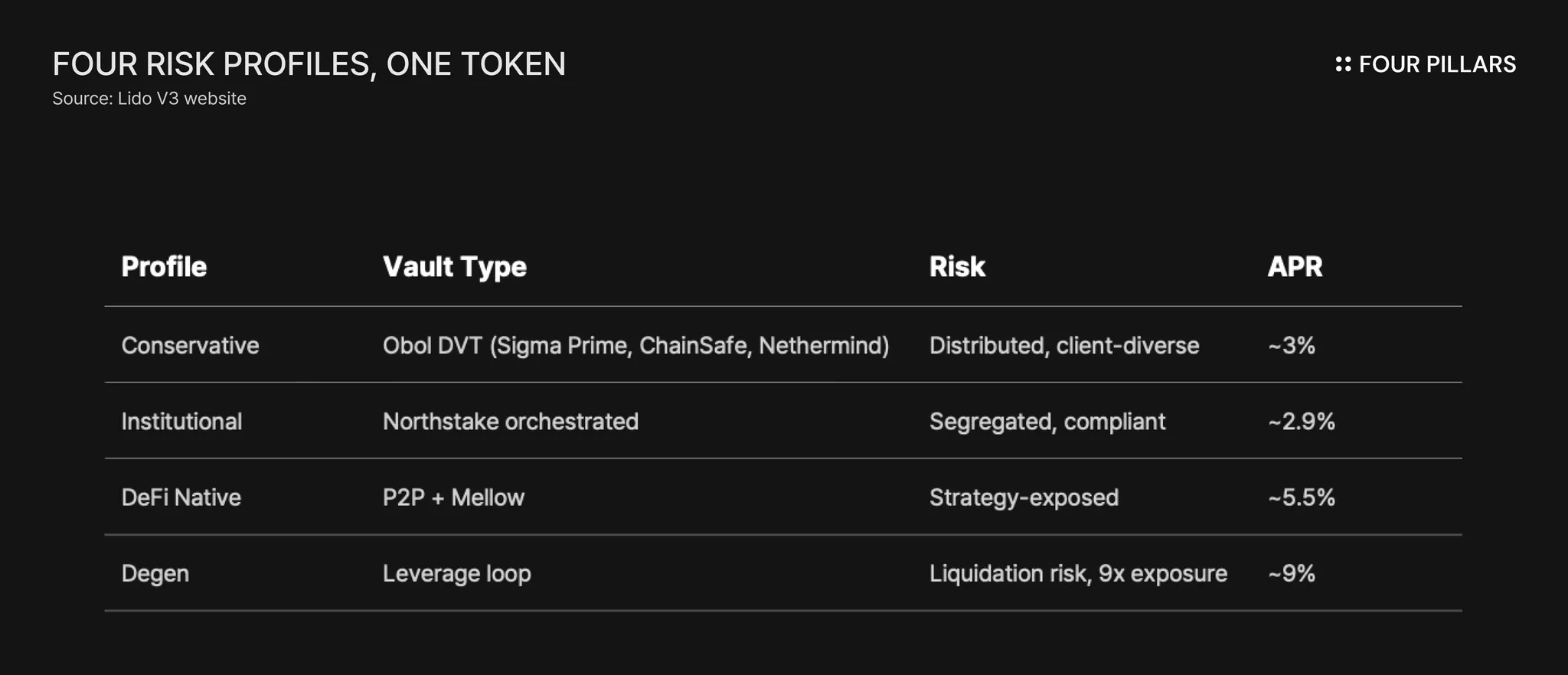

V3’s strategy is to bring operators capable of competing with Lido into Lido’s infrastructure. Through Symbiotic integration, stVault operators can offer restaking directly, and through Mellow wrapping they can build custom LRT products. Rather than remaining a simple pipe beneath these layers, V3 aligns incentives between Lido and operators serving yield-seeking users via a fee-based partnership model (infrastructure fees, liquidity fees, collateral fees). In terms of the return stack, vanilla staking delivers about 3%, DeFi vaults using Mellow about 5.5%, and ~9x leverage loops about 9% effective APR.

Source: Example of leveraged staking, Lido V3 website

The ecosystem is already taking shape. Symbiotic and Mellow are named as partners in the whitepaper, and live deployments will be made at launch. These integrations keep stETH as the liquidity layer while expanding what is possible for stVault users. The architecture is designed to deliver incremental value to the broader DeFi ecosystem.

The architecture is structured to satisfy all three segments. Adoption is not guaranteed, but the infrastructure is already live and early adopters are building.

4. Same token, different risk structures

Differences in risk and return arise not from stETH itself but from each strategy. stETH functions as the common liquidity infrastructure enabling these strategies, while differing exposures reside in vault configurations and the DeFi positions built on top. If this structure works, stETH moves closer to a liquidity primitive that sits atop user-selected risk configurations. The token’s utility becomes decoupled from the exposure of any specific vault; rather than accepting Lido’s operator set, users join a liquidity network while building their own risk beneath it.

That said, the validity of this structure depends on adoption. If, one year on, 90% of stETH still originates from the Core Pool and stVault remains a niche, then little has changed in practice. The market will judge the importance of this structure, and given that institutional sales cycles often take longer than market expectations, forecasting adoption speed is uncertain.

5. Structural limits to risk isolation

V3 improves risk isolation relative to V2, but “improvement” does not mean “complete.” If position sizing assumes full isolation, losses can still arise under extreme market conditions.

Areas where isolation applies are as follows. Operator performance is attributed to the relevant vault; operator downtime is limited to a reduction in that user’s APR; slashing hits the collateral buffer first; and leverage liquidations are the user’s problem. Under normal operating conditions, vault risk is effectively separated.

However, there are areas where isolation does not apply. If a vault’s health factor falls below a threshold, forced rebalancing is triggered and ETH is moved to the Core Pool to repay stETH debt. In this case there is no principal loss, but the position is lost and leverage is unwound regardless of intent. In addition, if simultaneous slashing occurs—such as a large-scale validator outage caused by client bugs—the 5–50% collateral buffer cannot absorb losses, and the Core Pool bears residual risk. Protocol-level failures such as oracle manipulation, governance attacks, and smart contract bugs affect all stETH holders regardless of vault configuration.

Risk mitigations do exist. A tiered collateral structure forces more concentrated operators to post higher collateral, creating first-mover advantages within each tier. LIP-23 proposes zkOracle verification with automatic halts under data discrepancies, and Dual Governance is already live.

In conclusion, V3 is assessed as delivering roughly 95% risk separation. Under normal conditions, user risk stays within the user’s vault, but in extreme scenarios it can still propagate to the overall system. Building an investment thesis on the assumption of full isolation is fragile; V3 is a meaningful improvement over V2, but not a change in the risk framework itself.

6. Implications

Lido’s TAM expands. While V2 targeted only users willing to accept pooled risk, V3 can also encompass users who want their own risk configuration while still needing liquidity. The latter is a much larger market, and it is strategically significant that segments that previously exited can now be accommodated within Lido’s architecture.

From the staker’s perspective, choices broaden. Passive users can keep using the Core Pool; active stakers can select vaults directly to secure reserve-ratio advantages; and yield-seeking users can now execute strategies natively within Lido rather than building them separately on top. Choosing among dozens of vaults is indeed more complex than “deposit and forget,” but for users who do not want complexity, the Core Pool remains an available option.

For the DeFi ecosystem overall, V3 leans toward cooperation over competition. Restaking and LRT protocols get a clearer integration path using stETH as the liquidity layer, and the architecture is designed to create partnership opportunities rather than competitive pressure.

7. Closing: the 70% opportunity still unstaked

70% of total ETH is still unstaked. The market is still in an early phase, and ample opportunity remains for Lido.

There are three key metrics to monitor going forward. First, the stVault TVL share relative to total Lido TVL, with 1 million ETH as the internal benchmark proposed in GOOSE-3. Second, yield-seeking capital inflows via Mellow and Symbiotic integrations—if APR Maxi begins building strategies through Lido rather than above Lido, the investment thesis is being realized. Third, institutional adoption via Northstake and P2P.org; progress is slow, but once capital enters, churn tends to be low.

Over five years, Lido has built stETH into the most liquid LST in crypto. V3 is a strategic push to bring back the 2.7 million ETH that left and, further, to absorb the 70% that remains unstaked—positioning Lido as a core infrastructure layer for Ethereum staking.

Bloomingbit Newsroom

news@bloomingbit.ioFor news reports, news@bloomingbit.io