Treasury yields won’t move unless the Fed does?… Fears of “fiscal dominance” [Global Money X-File]

Summary

- It reported that concerns about “fiscal dominance” have intensified as the U.S. Treasury’s scale of debt issuance coincides with the Fed’s policy of rolling over Treasuries and reinvesting into T-bills.

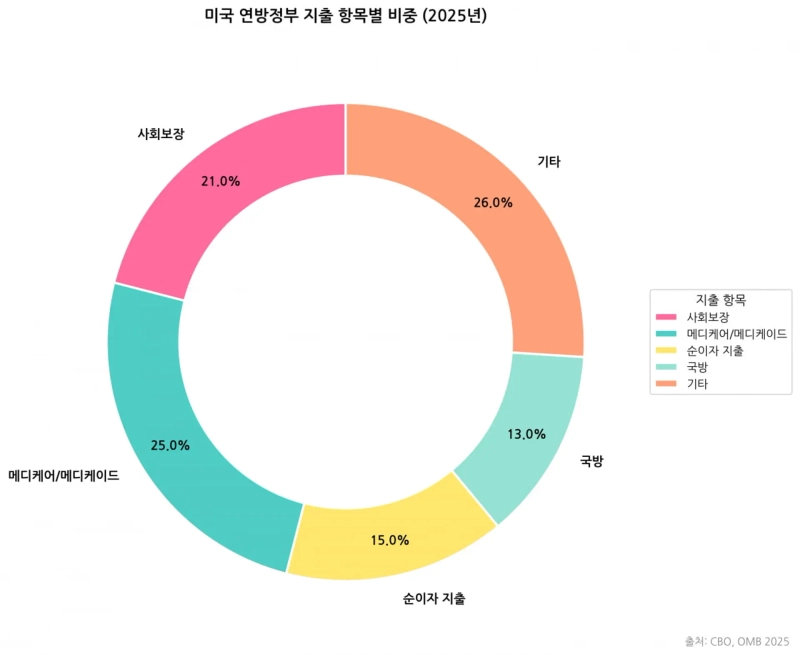

- It said that as U.S. net interest outlays have surpassed defense spending and federal debt is surging, concerns are rising over a spike in bond yields and potential corrections in high-valuation AI and biotech companies.

- It reported that if the QRA on the 4th signals normalizing the T-bill share and expanding long-term issuance, it could trigger a surge in 10-year and 30-year yields, a higher term premium, and dollar strength, putting heavy pressure on emerging-market bonds, including Korea’s.

Forecast Trend Report by Period

A growing view holds that global financial markets have become as focused on the scale of U.S. Treasury debt issuance as on the Federal Reserve’s monetary policy. The industry is watching the U.S. Treasury’s “quarterly refunding announcement” scheduled for the 4th. Analysts say the reason is the intensification of the so-called “fiscal dominance” phenomenon.

A 10–2 crack at the FOMC

According to the Fed on the 1st, last month’s FOMC decision to hold rates was, on the surface, a “status quo” outcome. But critics say it laid bare internal conflict and external political pressure. The vote was not unanimous but 10 to 2. The majority, including Fed Chair Jerome Powell, backed a hold, citing data and a balance of risks.

However, Governors Stephen Miran and Christopher Waller dissented, arguing for a 0.25%-point cut. Some note that the message from the minority was forceful enough that it is hard to view it simply as a hawk-vs-dove split. Some analysts even say Miran turned what had been behind-the-scenes political pressure into an overt act via a public vote.

Chair Powell stressed through this FOMC that the committee “focused only on its mandates of price stability and maximum employment, without political fear or bias.” Yet some say the Fed’s independence has been shaken. Looking at the FOMC “operating guidelines,” there are claims that a compromise with the U.S. Treasury emerged on the “quantity” side of Treasury holdings.

The guidelines included language stating that “principal payments from Treasury holdings will be rolled over in full, and principal payments from agency (MBS) holdings will be reinvested in Treasury bills (T-bills) in full.” They also specified that, if necessary, the Fed may purchase T-bills and other short-dated instruments for “technical purposes.” On the surface, this is a liquidity-management measure.

In substance, however, it can also be read as a form of “backdoor quantitative easing” that supports the Treasury’s short-term funding. The market response has been that “the Fed hasn’t been fully captured, but at least one wrist is being held by the Treasury.”

Interest costs exceed defense spending

Underlying concerns about fiscal dominance is U.S. debt that has become difficult to control. According to the Congressional Budget Office (CBO)’s “2025–2034 Budget Outlook,” U.S. net interest outlays already surpassed defense spending as of last year. In other words, the cost of paying interest on debt has grown larger than the cost of maintaining the world’s most powerful military.

As of January this year, U.S. net interest outlays exceed 3.2% of GDP. That is set to surpass the prior all-time high recorded in 1991. Assuming current laws remain in place, the CBO estimates net interest outlays will reach 4.1% of GDP by 2034. It also projected that, excluding Social Security and Medicare, it would become the largest single line item in the federal budget.

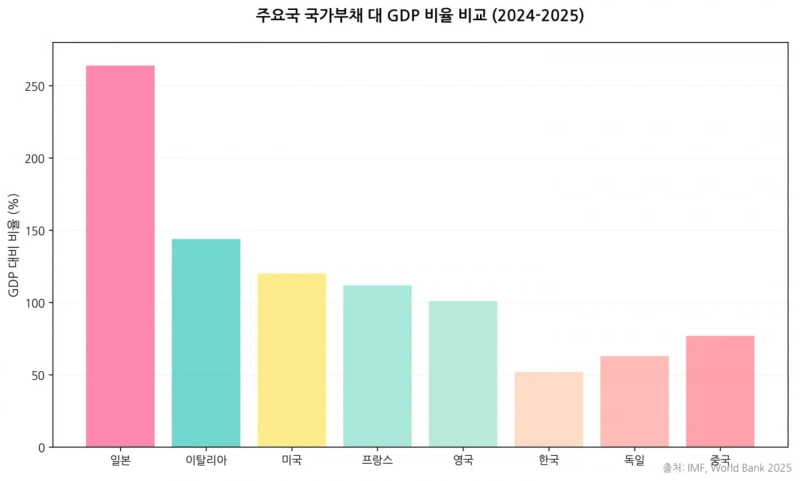

This fiscal deterioration is largely attributed to the Trump administration’s tax-cut and spending-expansion legislation known as the “One Big Beautiful Bill Act (OBBBA).” According to analysis by the Committee for a Responsible Federal Budget (CRFB), under an adjusted baseline reflecting the OBBBA and new tariff policies, U.S. federal debt is projected to approach 120% of GDP by 2035.

Former U.S. Treasury Secretary Larry Summers recently warned in a Mortgage Bankers Association (MBA) speech that “the current fiscal path is unsustainable,” adding that “absent dramatic productivity innovation, the bond market will soon hit a wall, which could trigger a sharp surge in interest rates.”

If the government issues Treasuries in bulk to pay interest, liquidity in the market can be easily sucked into the government. That can lead to a “crowding-out effect,” with private companies facing a shortage of funds needed for investment or sharply higher rates.

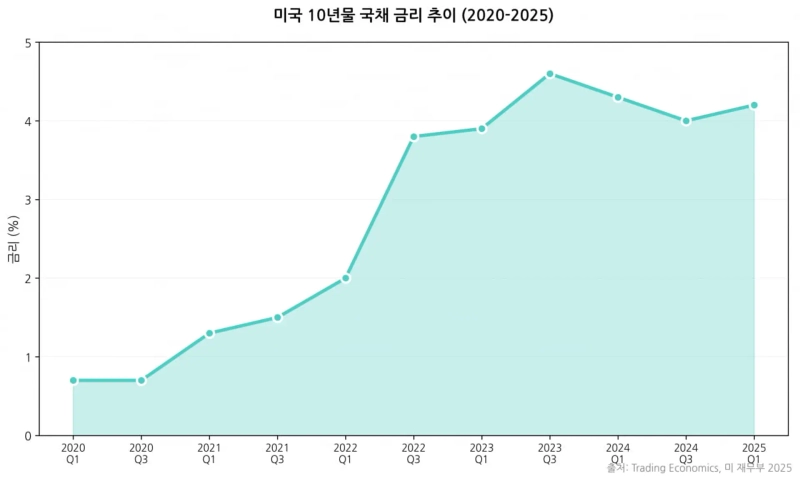

As the discount rate (Treasury yields) used to convert future cash flows into present value rises, downside pressure also increases for high-valuation AI and biotech stocks. In the venture-capital (VC) industry, skepticism could spread along the lines of: “If the risk-free yield is approaching 5%, why take risk?”

Attention turns to the scale of U.S. Treasury issuance

That is why global financial markets are treating the Treasury’s QRA due on the 4th as a risk event. If the FOMC determines short-term rates (the policy rate), the QRA influences “supply and demand,” a key driver of long-term yields.

Under fiscal dominance, bond yields are more likely to be determined by the sum of “expected short-term rates (the Fed’s policy path)” and the so-called “term premium.” Markets are now concerned about a sharp rise in the term premium amid questions over who will absorb the rapidly increasing supply of Treasuries.

Over the past two years, the U.S. Treasury has increased the share of issuance in short-term securities (T-bills) with maturities under one year to prevent a surge in long-term yields. As of last year, 84% of new issuance was financed with T-bills. This exceeds the Treasury Borrowing Advisory Committee (TBAC)’s recommended appropriate share of around 20%. It resembles a household continuously relying on cash advances (short-term debt) to cover credit-card bills.

Brian Smith, a deputy assistant secretary at the Treasury, recently said the department would “respond flexibly in line with long-term fiscal needs,” signaling the possibility of a strategy shift. If, in the QRA on the 4th, the Treasury announces that it will “normalize the T-bill share and significantly increase long-term issuance,” analysts say it could deliver a supply shock, driving a sharp rise in 10-year and 30-year yields.

U.S.-driven fiscal-dominance risk affects the Korean economy. According to research by the Bank for International Settlements (BIS), the impact on emerging markets is far larger when U.S. Treasury yields rise due to “a higher term premium” than when they rise due to “a stronger real economy.” A rise in the U.S. term premium is a signal that “investors demand more compensation even to hold U.S. Treasuries, the world’s safest asset.”

In that case, investors demand even higher premia for relatively riskier assets than the U.S., such as Korean government bonds or other emerging-market debt. Hyun Song Shin, head of research at the BIS, pointed out that “a rise in the term premium on U.S. Treasuries, combined with a stronger dollar, acts as a powerful mechanism that sharply tightens financial conditions in emerging markets.”

[Global Money X-File helps you track important but less well-known flows of money around the world. To conveniently keep up with essential global economic news, please subscribe to the reporter’s page.]

Reporter Juwan Kim kjwan@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.