"Easy money is over" Markets plunged on Wash fears—then a 'bold call' emerged [Bin Nansa’s Wall Street Without Gaps]

Summary

- Wall Street said the key variables driving the bull market in stocks, gold and commodities have not changed, emphasizing that it remains in a buying stance on these assets.

- Goldman Sachs and JPMorgan reaffirmed a preference for real assets, citing AI investment, fiscal expansion and currency depreciation, and said the asset bull market would continue alongside upward revisions to gold price forecasts.

- Wall Street presented as solutions a barbell strategy of holding real commodities such as gold and copper along with growth equities, a duration-shortening approach centered on short-term bonds, and using February volatility as a dip-buying opportunity.

Forecast Trend Report by Period

Wall Street shakes off 'Wash fears': "Keep buying gold and stocks"

Druckenmiller: "The 'hawkish Wash' is a misunderstanding"

Wall Street, too: "QT can’t happen right away"

Market overheating ends, 'taper tantrum' quickly calms

AI investment, fiscal expansion, currency depreciation

Core drivers of the 'asset bull market' remain intact

"A massive wave of AI capex is bigger than Fed policy"

Hold gold/commodities and equities together: a 'barbell strategy'

"There’s a risk of a February pullback, but it could be a dip-buying opportunity"

Markets that had been jolted by the nomination of former Fed governor Kevin Warsh as the next chair of the Federal Reserve (the U.S. central bank) are recovering quickly. Warsh’s history of criticizing the Fed’s quantitative easing (QE) revived fears of the end of the “easy money” era investors had grown accustomed to, triggering a “taper tantrum” in which stocks, bonds, gold and bitcoin sold off in tandem. That bleak mood persisted right up until before the U.S. market open on Feb. 2 (local time).

But the panic did not last long. In U.S. trading on Feb. 2, the S&P 500 rebounded 0.5% to move back close to record highs, while the small-cap Russell 2000 finished up nearly 1%. Gold and silver, which had suffered their biggest drop since 1980, are rebounding, as are industrial metals such as copper, platinum and palladium.

In the near term, fear has been tempered by a wave of analysis suggesting Warsh is not as hardline a hawk as markets had worried. More fundamentally, however, the view has quickly spread that the key variables that have powered the bull run in equities and in precious metals/commodities have not changed.

Mark Wilson, head of trading at Goldman Sachs, frames the recent plunge as a “technical correction” driven by excessive crowding into equities and gold/silver, rather than a shift in the macro environment such as Fed policy. In his view, none of the key forces that have determined the market’s trajectory—solid U.S. growth, Trump administration stimulus, unwavering enthusiasm for artificial intelligence (AI) investment, and a move to raise allocations to real assets—have changed at all.

In other words, one person named Warsh is unlikely to alter these sweeping trends. For example, Ashish Sehgal, co-head of Goldman Sachs’ global rates, FX and commodities business, stressed: “We remain buyers of equities and gold/commodities.”

Druckenmiller: “Warsh isn’t an unconditional hawk”

Another factor that helped markets quickly shrug off “tightening fears” sparked by Warsh’s nomination was an interview with Stanley Druckenmiller—Wall Street’s legendary investor and Warsh’s mentor. In interviews with the Financial Times and Barron’s after the nomination, Druckenmiller said Warsh is “not an unconditional hawk,” portraying him as a “pragmatist” to the market.

In particular, Druckenmiller said Warsh is “very open-minded” about former Fed Chair Alan Greenspan’s approach to monetary policy, emphasizing that Warsh does not subscribe to the fixed idea that inflation must necessarily follow whenever the economy grows.

Greenspan led the Fed in the 1990s, a U.S. golden age that preceded the bursting of the information-technology (IT) bubble. Though he once warned that surging IT stock prices reflected “irrational exuberance,” he later said: “The Fed’s goal is to improve the economic and financial environment to encourage the technological innovation and investment that spur structural productivity gains,” and kept rates unchanged for nearly five years. That reflected the belief that a productivity revolution was delivering “growth with price stability,” with the Fed providing support.

This “Greenspan-style” dovish rate policy is also what Trump’s economic team—including Treasury Secretary Bessent and National Economic Council (NEC) Director Hassett—has called for. Warsh, who has publicly stressed that “AI is a powerful disinflationary force,” shares that view. In effect, Druckenmiller resurfaced Warsh’s thinking to the market in Warsh’s stead, as Warsh must refrain from official comments until his confirmation hearing.

Druckenmiller also underscored that “Bessent and Warsh will have to work together,” calling coordination between the Treasury secretary and the Fed chair “an ideal combination.” By highlighting the possibility of coordination between monetary and fiscal policy, he helped erase concerns about the one-sided quantitative tightening (QT) scenario the market had feared. (Druckenmiller, when he worked at Soros Fund Management, gave Bessent his first job, and also backed Bessent when he founded Key Square Capital.)

“A near-term pivot to QT is difficult”…Wall Street’s math

Wall Street also expects Warsh would struggle to push through a rapid balance-sheet runoff. Morgan Stanley said that even if Warsh takes office as chair, “discussion of QT will not be possible until at least after 2027.” With the Fed having only recently begun “de facto” QE since late last year in the form of short-term bill purchases, it would be difficult to abruptly reverse balance-sheet policy. Deutsche Bank likewise said that “even as Fed chair, it won’t be easy to persuade fellow FOMC members,” adding that it is “hard to see monetary policy changing visibly in the near term.”

In reality, Wall Street banks that benefit from asset-market support and interest income on reserves thanks to Fed liquidity do not want today’s “ample liquidity” to shrink. Moreover, the Treasury market—already highly dependent on the Fed’s role—could see greater rate volatility if the Fed begins to slim down. That is why Wall Street views Warsh’s “small Fed” thesis with skepticism.

Politically, too, President Trump—heading into midterm elections—has limited room to tolerate aggressive tightening. Just one day after nominating Warsh, on Jan. 31 (local time), Trump even joked that he would “sue Warsh if he doesn’t cut rates.”

That has helped spread relief that at least through this year, both rate policy and balance-sheet policy are likely to remain accommodative.

Stocks, gold, commodities: “Real assets over paper”

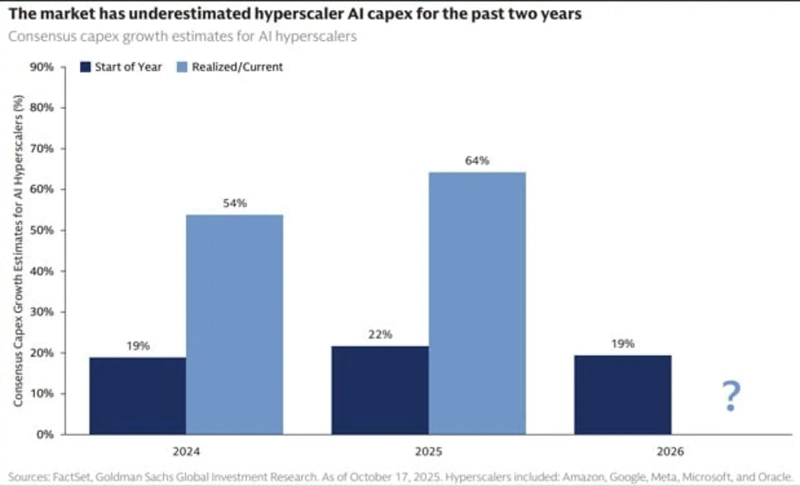

Against this backdrop, market conviction in an “asset bull market” is hardening again. Sehgal said AI investment and U.S. reindustrialization are the key engines lifting real assets such as equities, precious metals and commodities, projecting that global AI-related capital expenditure (CAPEX) will reach $1 trillion this year alone. “This infrastructure investment will be the engine of economic growth over the next 5–10 years,” he said. “Fed or fiscal policy is only a small factor compared with this massive investment wave.”

Of course, President Trump’s various fiscal expansion measures and accommodative fiscal policy also underpin the story. Sehgal expects productivity and nominal growth to be surprisingly strong as a result, while arguing that overheating risks are limited—citing AI-driven cooling in the labor market and deepening K-shaped polarization, as well as the structural disinflation potential from AI and aging demographics. As in Greenspan’s thinking, the sequence “overheating → inflation → rate hikes” may not be inevitable.

At the same time, Sehgal ranks real assets such as gold and copper as top-priority holdings. Deepening geopolitical fragmentation, Trump’s tariff policy, and currency depreciation driven by accommodative policy are stimulating demand for real assets.

Despite the recent plunge, gold is up 10% over the past month and 70% over the past year. Even so, Sehgal argues this is “a multi-decade trajectory, not a speculative frenzy.” Commodities markets can see volatility because available supply is limited, but he expects sustained demand from central banks and individual investors increasing gold allocations away from the dollar.

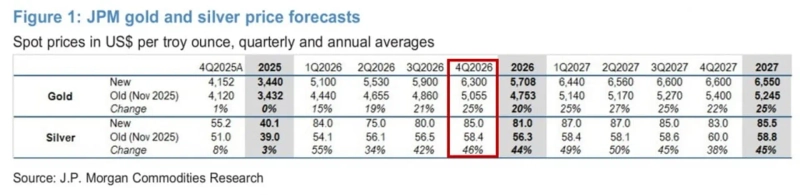

JPMorgan also raised its year-end gold price forecast to $6,300 from $5,055, and its end-2027 forecast to $6,600 from $5,400. The bank cited the view that “the superiority of real assets over paper assets remains firm, and despite short-term volatility, long-term upside momentum will remain fully intact.”

Opinions are more divided on silver, which—unlike gold—does not have central banks as a structural buyer. JPMorgan said it is “concerned that silver may undergo a deeper price correction than gold,” but added that “the average downside support level appears to have risen to $75–$80 compared with before.” It put its silver forecast at $85 for year-end and $83 for end-2027.

The answer is a gold + stocks ‘barbell’

The conclusion is clear. Sehgal emphasizes a “barbell strategy” that anchors portfolios on equities as growth assets and on real commodities such as gold and copper as hedges against currency depreciation. If you believe we are in the early stage of a global reindustrialization and credit-expansion cycle driven by AI, holding AI-related equities is an obvious choice. At the same time, he argues, investors should also own real assets that can protect against inflation and currency debasement.

Ashish Sehgal, co-head of Goldman Sachs’ global rates, FX and commodities business, stressed: “We remain buyers of equities and gold/commodities.” Source=Goldman Sachs

Meanwhile, big bond investors including Sehgal emphasize a “shorter duration” strategy for fixed income. If you want to hold bonds, they say you should include short-term bonds—less sensitive to rate moves—as a minimum defensive buffer against the risk scenario in which inflation re-accelerates and the Fed hikes aggressively.

“Volatility is a dip-buying opportunity”…leading sectors

How should investors pick stocks? On Wall Street, warnings are unrelenting that U.S. equities—entering the fourth year of a bull market—will suffer heightened volatility this year. Uncertainty is high, including valuations that have risen relative to other countries, inflation risk, slowing employment and polarization, policy risk, and midterm elections.

Scott Rubner, head of equities and derivatives strategy at Citadel Securities, is also warning about the possibility of a February pullback. February has often seen patterns in which bear phases unfold as the early-year inflow effect fades. Still, he stresses that February volatility could present a dip-buying opportunity. His baseline view that the bull market will continue this year is based on policy momentum, stable corporate earnings, improving breadth from sector rotation, and retail investors—driving flows through “high-conviction buying.”

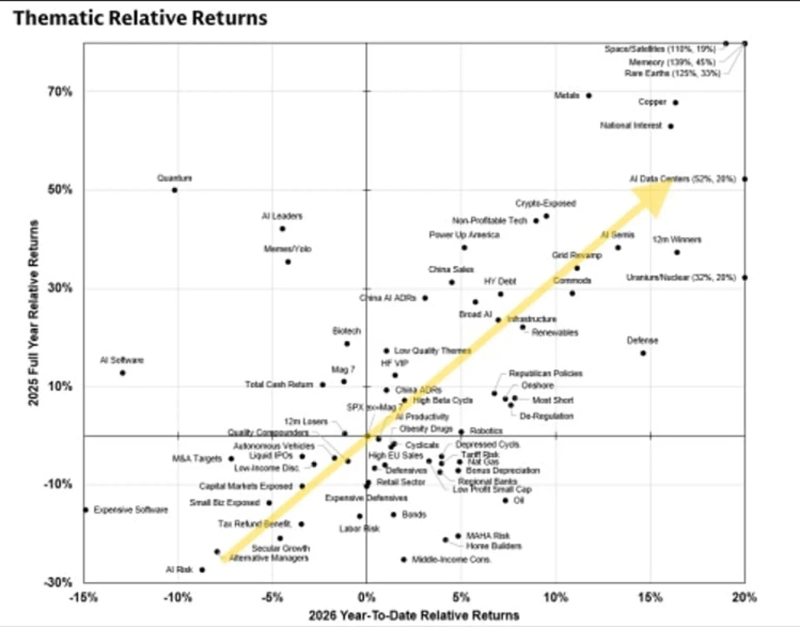

In a market with rising volatility, it becomes more important to identify the sectors and companies most likely to emerge as winners. In periods like now—when the AI revolution, a reshaping geopolitical order, and policy momentum are leading markets—the themes and sectors that can ride those currents are likely to be key.

According to Goldman Sachs’ analysis, themes that posted high relative returns both last year and early this year include: (1) AI hardware and infrastructure such as memory semiconductors, AI data centers/servers, the power grid, and space/satellites; (2) themes expected to benefit from policy momentum, such as defense/security aligned with U.S. interests and rare earths, uranium and nuclear power; and (3) real commodities such as metals, copper and mining stocks. These are themes tied to AI/power/defense, with a tangible “real” component and clear policy or geopolitical catalysts.

Energy, homebuilding and consumer sectors focused on the middle class have shifted from last year’s weakness to a recovery early this year—themes expected to benefit from accommodative policy and nominal economic growth. By contrast, the quantum theme, AI leaders, and the Magnificent Seven mega-caps that led the bull market through last year have become targets for profit-taking this year. Meanwhile, high-valuation software that has not shaken off the narrative of being “eaten by AI,” as well as low-growth/low-quality names sensitive to leverage, remain in a structurally weak patch this year as they were last year.

Ultimately, even with the leadership change at the Fed, the market’s big picture—preferring real assets over paper currency—has not changed. The illusion of “easy money” may have partly faded, but the strategy of holding both real commodities and growth stocks still looks closest to Wall Street’s answer key.

New York=Correspondent Bin Nansa binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.