PiCK

[Hands-on] Paying at cafes and convenience stores with coins… what it’s like to use a ‘coin card’

Summary

- It said payments are possible at many merchants in Korea by converting major digital assets such as Bitcoin, Ethereum and Solana into fiat currency in real time.

- It noted that the market is expanding rapidly, with global total payment volume for coin cards that use the global Visa and Mastercard card networks surging about fivefold from a year earlier.

- It said Korea’s finance sector is moving to strengthen competitiveness by building USDC, stablecoin and digital-asset-based payment infrastructure, and by conducting a card-network payment technology proof of concept (PoC).

Forecast Trend Report by Period

Coin card hands-on

Real-time coin→cash conversion mechanism

Tap the terminal and the payment goes through immediately

Runs on the Visa and Mastercard card networks

Korean finance sector ramps up response

I recently heard that coin cards that allow payments with digital assets can also be used in South Korea. Not only stablecoins pegged to fiat currencies, but also major digital assets such as Bitcoin (BTC), Ethereum (ETH) and Solana (SOL) can be used for payments.

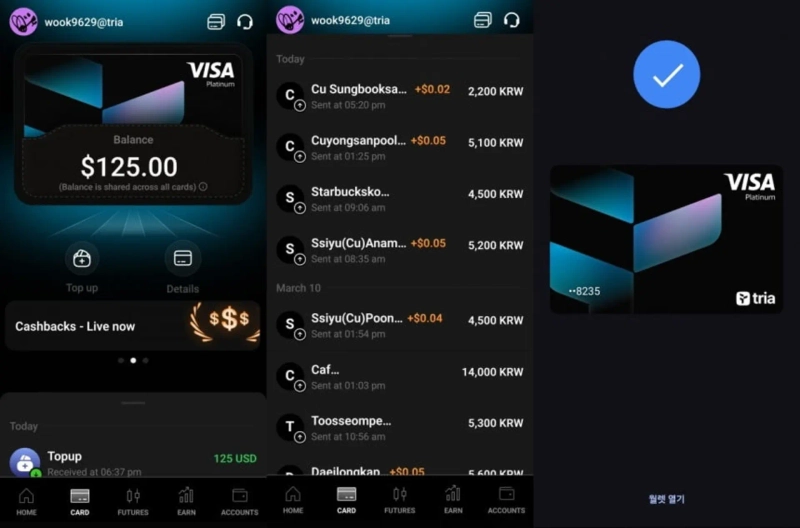

I decided to try a coin card myself. On an industry contact’s recommendation, I obtained a Visa card linked to a blockchain project called TRIA for about $20. After downloading the app and completing customer verification (KYC), a virtual card was issued immediately. I then deposited Solana worth about $125 into TRIA’s digital wallet and topped up the virtual card.

There were limitations in the process. I could not add the card to Samsung Pay, which I use. After checking, TRIA cards were available only on Apple Pay and Google Pay. Fortunately, I was able to register it on Google Pay, which I used during a business trip.

After visiting a Starbucks store in Gangnam-gu, Seoul, I opened the Google Pay app and held my phone to the payment terminal, and the payment went through right away. While it varied depending on the terminal environment, coin cards could be used at most merchants (convenience stores, cafes, etc.) that support Apple Pay.

Using Visa and Mastercard payment rails

Digital assets are spreading beyond being a mere investment vehicle into the real economy. Coin cards launched through partnerships between global payment networks such as Visa and Mastercard and blockchain infrastructure firms were confirmed to be usable at many merchants in Korea.

A coin card is a payment method that uses blockchain technology to link a card with a digital-asset wallet. It works by converting the user’s digital assets into fiat currency for payment.

The payment itself is processed through Visa’s and Mastercard’s existing card networks. The conversion of digital assets into cash uses a blockchain-based “real-time FX (Real-time On/Off ramp)” function.

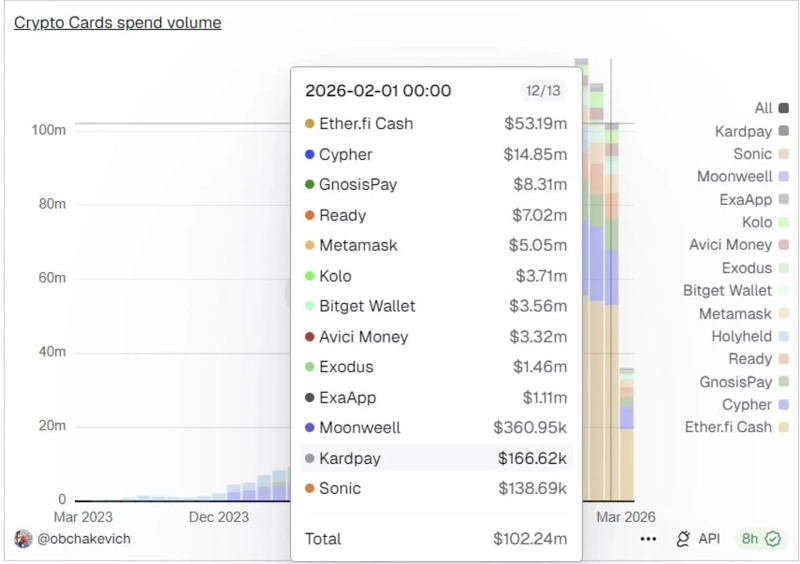

The market is also expanding rapidly. Global digital-asset exchanges such as Crypto.com, Bybit and Coinbase have already launched various coin cards, and projects including TRIA, Cypher, KAST, EtherFi (ETHFI) and READY are rolling out card services one after another.

According to Dune Analytics, global total payment volume for coin cards amounted to $102.24 million (about KRW 150 billion) as of February. That is about a fivefold surge from the same month a year earlier.

Benefits include low fees and global usability

Listening to actual users, the reasons for using coin cards were clear.

The biggest reason is the “usability of held assets.” Most digital-asset investors must sell their holdings on an exchange, convert them into Korean won, and then withdraw the funds in order to use them. This process can entail verification steps and fee burdens.

Coin cards, by contrast, can be used for payments immediately simply by depositing digital assets into a card-dedicated account, reducing the need for such steps.

An industry source in Korea’s digital-asset sector, identified only as A, said, “I hold quite a lot of digital assets for investment purposes,” adding, “Previously, I had to convert digital assets into won every time to pay my card bill, but I started using a coin card because it lets me skip that process.”

Low fees and global usability are also cited as advantages. With conventional overseas cards, multiple intermediaries often participate in the payment process, pushing fees higher. Coin cards, however, are viewed as having secured cost competitiveness by simplifying the settlement structure.

As a result, coin card use is already spreading among industry professionals who travel abroad frequently. Another industry source, identified only as B, said, “If Apple Pay works overseas, you can also pay with a coin card,” adding, “From hotel stays to meals, I’m paying with a coin card without needing to exchange currency separately.”

In addition, cashback of 4.5–10%—higher than typical debit cards—and airdrop points paid based on spending performance are cited as advantages of coin cards.

FSS: “Hard to regulate under current law”… concerns over reverse discrimination

Because most coin cards are issued overseas, they are not included in Korea’s financial regulators’ licensing framework. Regulators have also stated that it is not easy to regulate them directly under current laws and regulations, because overseas operators that provide services without establishing a domestic branch are not subject to supervision.

Although the services nominally target overseas users, as in the reporter’s case, domestic users can also easily obtain and use cards through mobile apps.

An industry source explained, “On the surface, it may look like digital assets are being used directly for payments, but in reality, at the time of payment the operator purchases the user’s digital assets, pays out fiat currency, and then the payment proceeds,” adding, “It is effectively the same as domestic users using a card issued overseas.”

Still, concerns have been raised that such a structure could lead to “reverse discrimination” against domestic card companies. Cho Jae-woo, an associate professor at Hansung University, said, “Overseas digital-asset firms are targeting the Korean market via card networks,” adding, “With institutionalization delayed, domestic players are in a difficult position to respond.”

He added, “For a domestic card company to provide the same service to Korean customers, it may also need to obtain a domestic virtual asset service provider (VASP) license.”

Korea’s finance sector also moves to respond

Korea’s finance sector is also moving into payment businesses that leverage digital assets. The strategy is interpreted as an effort to build digital-asset-based payment infrastructure and secure market competitiveness.

Hana Financial Group earlier this month announced a service targeting foreign customers in partnership with Circle, the issuer of USDC, and exchange Crypto.com. It offers certain benefits when users top up a Crypto.com prepaid card with USDC and use it at domestic merchants.

Fintech firms are also entering the field. Danal recently said it will launch next month a digital-asset payment service for foreign visitors to Korea in cooperation with digital-asset payment platform Binance Pay and Circle. The service is expected to be applied first to the foreigner prepaid card “KONDA.”

Moves at the industry level are also continuing. The Credit Finance Association last January launched the “Stablecoin Phase 2 Task Force (TF)” and prepared a draft set of integrated guidelines for card companies. More recently, it said it will conduct a three-month “stablecoin card-network payment technology proof of concept (PoC)” starting next month in cooperation with Lambda256, a Dunamu subsidiary.

Uk Jin

wook9629@bloomingbit.ioH3LLO, World! I am Uk Jin.