It wasn’t a safe haven—it was an ATM… Why gold plunged as oil and rates jumped [Bin Nansaee’s Wall Street, No Gaps]

Summary

- Gold plunged amid war, a surge in oil prices, and fears of higher rates for longer, but Wall Street said it views the move as selling to secure liquidity.

- Wall Street said economic fundamentals are weaker than in 2022, making Fed rate hikes unlikely, and maintained the view that rate cuts will ultimately resume.

- Prominent Wall Street figures said gold’s structural investment rationale remains intact, citing geopolitical risk, inflation, and erosion of institutional trust.

Forecast Trend Report by Period

As the war between the U.S. and Israel and Iran intensifies, markets are being gripped by turmoil with no visibility ahead. Even on Wall Street—where optimism had been stronger in the early days of the conflict—sentiment has clearly shifted over the past week. According to Goldman Sachs and JPMorgan, institutional investors on the 18th (local time) unleashed the largest one-day net selling since the 2022 bear market, moving into full-scale position reductions. Retail flows that had been propping up declines through dip-buying also fell, with this week’s inflows down 15% from the prior week. The S&P 500, which had been holding around -4% off its peak even two weeks after the war began, fell 1.5% on the 20th (local time) alone, while the Nasdaq dropped 2%, breaking a three-year trendline.

The abrupt collapse in optimism also reflects a string of major central banks—(more or less forced)—showing their hawkish claws over the past week. Of course, the main culprit is oil. The Reserve Bank of Australia raised rates citing the war-driven surge in oil prices, and the U.S. central bank (Fed) held rates while keeping its dot-plot projection of one cut this year, but Chair Jerome Powell blocked dovish expectations, saying, “If we don’t see progress on inflation, we won’t be able to cut rates.” In other words, the Fed was more wary of inflation risks than a weakening labor market.

Even the Bank of Japan, scarred by decades of deflation, said it would “respond with a focus on the war if it emerges as a major risk” (BOJ Governor Kazuo Ueda). After that, the Bank of England and the European Union (EU) central bank also signaled they could move to tighten as early as April to tackle inflation, sending global bond markets sharply lower.

The U.S. 2-year Treasury yield, which was 3.37% before the Iran war and 3.65% before the FOMC, surged to 3.89% on the 20th (bond prices fell). It rose above the current policy rate (3.625%), effectively pricing in the possibility of a rate hike. The market’s list of worries—once dominated by oil—has now added rates. Neil Dutta, an economist at Renaissance Macro, said, “Rate cuts driven by good news are no longer something we can expect,” adding, “Even if the unemployment rate rises, the Fed doesn’t appear likely to step in immediately,” and “It feels like another backstop for the economy has disappeared.”

In this environment, another asset plunged alongside Treasuries: gold. On the 20th, gold futures fell to $4,574.9, down 9.6% in a week—the biggest weekly drop since September 2011. Conventional wisdom would suggest that with heightened geopolitical risk and oil-driven inflation fears, gold—long seen as a “safe haven” and an “inflation hedge”—should rise. Instead, the market is moving in the opposite direction.

Gold, more a liquidity asset than a safe haven

The first reason gold is plunging after the war is, simply, that it had “risen too much.” Even after the recent selloff, gold is up 41.5% over the past year.

With volatility exploding across all asset prices—oil, equities, rates—and liquidity stress emerging, some investors scrambling to raise cash appear to be selling gold first, as it has posted the strongest returns and remains highly liquid. Yardeni Research said, “Gold is facing profit-taking pressure after a sharp run-up,” adding, “Investors in the Middle East also seem to be selling gold to secure U.S. dollars.”

In particular, hedge funds with heavy leverage are reportedly selling gold to offset losses in an increasingly volatile rates market and to meet forced deleveraging. Ahead of the war, hedge funds had built large leveraged positions betting on a renewed widening in the gap between long- and short-term rates (steepening). The thesis was that the Fed would keep cutting rates (short-term rates would fall), while long-term rates would be unable to come down due to heavier debt burdens and inflation fears—therefore the term spread would widen.

But once the war broke out and fears of central-bank tightening pushed short-term yields sharply higher, markets moved against those bets. The spread between 30-year and 2-year U.S. Treasury yields narrowed to below 1% point on the 18th, the tightest since last July. Facing forced liquidations, hedge funds respond to margin calls (demands for additional collateral after declines in collateral value) by selling what they can sell fastest—and what has built up the most unrealized gains—starting with gold. That dynamic was also behind the simultaneous sharp narrowing in the term spread and the plunge in gold on the 18th.

Bank of America’s fund manager survey for the first week of March showed the most crowded trade remained “long gold (35%).” At the same time, according to Goldman Sachs, the most sold asset globally since the outbreak of the war was Japanese equities, and the second was gold. If so, it’s less that gold has lost its appeal and more that in an extremely volatile market, gold has been used as a “cash machine (ATM)” to raise cash—triggering a wave of selling.

“The era of easy cuts is over”

The rapidly fading expectation of rate cuts from central banks has also brought a “higher for longer” scenario to the forefront—another headwind for gold.

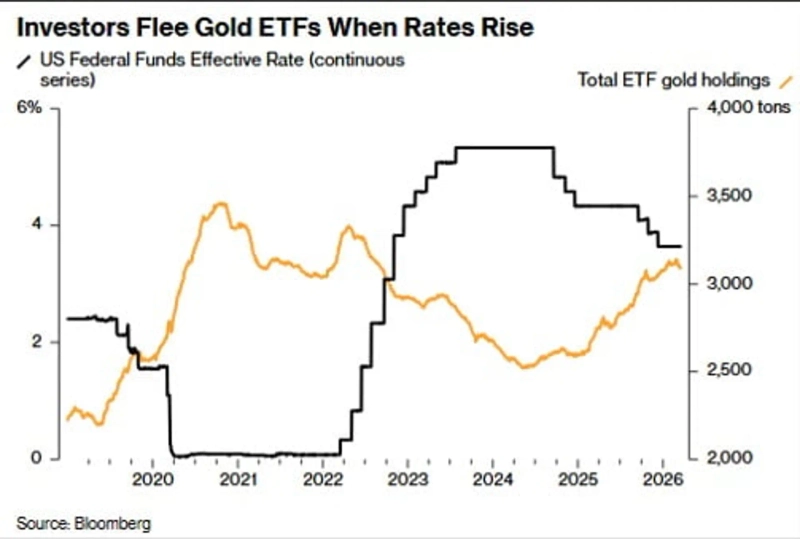

Historically, gold has shown an inverse correlation with real interest rates. Gold is a safe haven, but it is also a “non-yielding asset.” Because gold does not generate cash flows such as interest or dividends, it becomes relatively less attractive when policy rates stay high and real rates rise. That means the boost to gold demand as a safe haven from war may be outweighed by the drag from rising oil and interest rates.

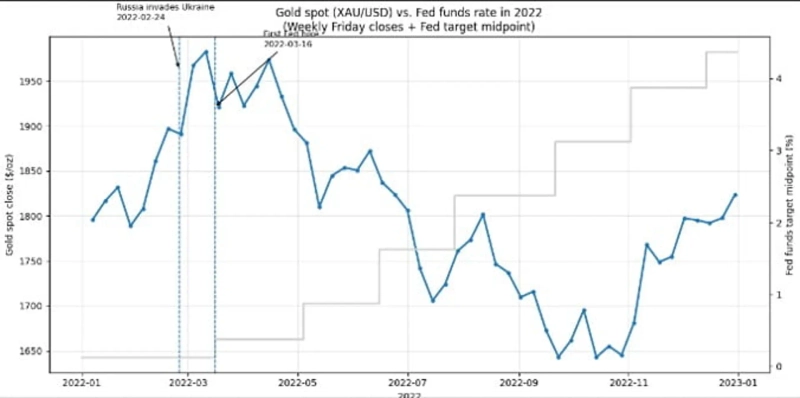

That was also the case during Russia’s invasion of Ukraine in 2022. Gold briefly jumped right after the war began, but then fell for seven straight months as the Fed embarked on consecutive rate hikes to rein in inflation. It only rebounded after talk emerged that the Fed might slow the pace of hikes. The same dynamics are at work today as oil’s surge revives fears of tighter policy.

Nick Timiraos, a Wall Street Journal reporter often described as an unofficial Fed mouthpiece, wrote after this March FOMC that “the era of ‘easy’ rate cuts may be over.” Through last year, the Fed kept cutting rates under the banner of “policy recalibration,” even when inflation was above 2%, but now it may be difficult to cut unless inflation clearly falls or the labor market clearly deteriorates.

Even if cuts resume, the magnitude may be smaller than previously expected. In this quarter’s economic projections, the Fed raised the median estimate of the longer-run (neutral) rate (3.0→3.125%) and the longer-run GDP growth rate (1.8→2.0%). The upward revision to the longer-run growth estimate is the first in six years. It signals an assessment that productivity gains have lifted the U.S. economy’s potential growth rate—and therefore the neutral rate the economy can tolerate.

The neutral rate is the “normal” rate the economy can bear—one that neither stokes inflation nor restrains growth. Put simply, because the Fed adjusts the policy rate toward that neutral level, a higher neutral-rate estimate implies the Fed will have less room to cut rates over the long term than before.

Markets are now confronting the prospect that the ultra-low-rate era familiar since the global financial crisis is fading, and that rates higher than previously expected could persist for longer. In that process, both interest rates and gold prices have seen heightened volatility.

Wall Street: “Rate-hike forecasts are nonsense”

So will the Fed really hold rates all year—or even hike? Fed funds futures markets, which had expected 2–3 cuts this year before the war, now price an 80% probability of no change and a 5.3% probability of a hike.

But on Wall Street, many argue that “now is different from 2022.” Then and now, war and surging energy prices have fueled inflation fears, but judging by the labor market, household savings rate, and aggregate demand, economic fundamentals are weaker than in 2022.

The key argument is that the Fed, with its dual mandate of maximum employment and price stability, cannot raise rates focusing only on inflation while the labor market is cooling. JPMorgan said, “It is difficult for central banks to respond to a geopolitical supply shock with tightening when growth risks are also present.” Citi said, “Ultimately, a rising unemployment rate will move the Fed,” maintaining its forecast for three cuts this year. Of course, these views implicitly assume the Iran war will not drag on beyond April–May.

Michael Hartnett, chief investment strategist at Bank of America (photo), said, “The idea that the Fed will hike rates is nonsense,” adding, “Cuts may be delayed by the oil spike, but ultimately we think the Fed will cut. We all live in a world where we’ve become far too used to the Fed stepping in whenever markets run into trouble—the ‘Quantitative Easing Generation (Gen QE).’” The point is that because of an unsustainable debt structure and the risk of market breakdown, the Fed has become constrained from overtightening.

Implicit as well is the notion that while everyone knows rates need to rise to correct today’s distorted “debt economy” and curb excessive asset inflation, it is questionable whether central banks have the will to prescribe that “bitter medicine” given the political costs and the risk of an equity-market collapse.

Is the gold bull market over?

Despite gold’s extreme volatility since the war, Wall Street has not abandoned the case for a structural allocation to gold. George Noble, known as “Peter Lynch’s assistant,” said, “Considering out-of-control fiscal and monetary policy, sticky inflation, intensifying geopolitical tensions, and the current energy shock, it’s even harder to turn bearish on gold.”

Stanley Druckenmiller argues gold is needed as a hedge against geopolitical risk, while Ray Dalio says investors should hold gold as protection against a decline in trust in traditional financial assets—including paper currencies—in an era of “capital war.” Goldman Sachs views gold as a “store of value that does not rely on institutional trust.” In other words, it recommends holding gold not as a tool for aggressively compounding wealth, but as a traditional store of value to hedge against the erosion of fiat currency.

By Bin Nansaee binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.