Nine sidecar triggers since the war broke out… “Retail investors, load up on these stocks” [Case Study by Han Kyung-woo]

Summary

- Brokerages said that with the Middle East war and rising oil prices limiting rate declines, investors should focus on stocks with upward earnings revisions and standout undervaluation appeal.

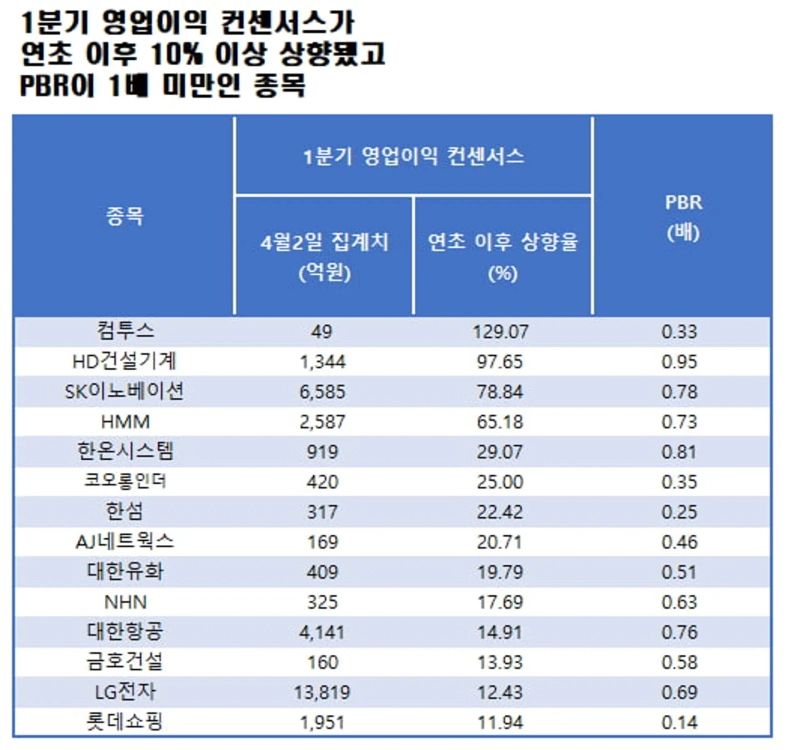

- FnGuide selected 14 stocks whose first-quarter operating profit consensus was revised up by more than 10% and whose PBR is below 1x, citing them as names with strong PBR appeal.

- Beneficiaries of the Middle East war such as SK Innovation, HMM and Korean Air were cited, with global oil prices, the Shanghai Containerized Freight Index, and spillover gains from disruptions to Middle East airport operations identified as drivers of earnings improvement.

Forecast Trend Report by Period

‘Trump risk’ persists

Consider strong earnings and undervalued names

Nine sidecar triggers since the outbreak of the Middle East war

“Oil-driven rate declines likely limited… focus on PBR appeal”

With uncertainty lingering from the U.S.-Iran war, Korea’s stock market is heading into next week’s earnings season. Brokerages are advising investors to position for names where earnings estimates have been revised up and undervaluation stands out amid heightened volatility.

According to financial data provider FnGuide on the 4th, the combined consensus (average brokerage forecast) for operating profit of KOSPI constituents in the first quarter this year stands at 132.048 trillion won. A consensus has formed that this would represent a 93.48% increase from the first quarter of last year. Over the past month, the consensus has been revised up by 1.57%. Despite concerns over fallout from the Middle East war, expectations for Korean corporate earnings have risen.

Contrary to the earnings outlook, stock prices swung sharply. Last week alone (March 30–April 3), a temporary suspension of program buy/sell orders (buy/sell sidecar) was triggered once each in the KOSPI and KOSDAQ markets.

On April 1, when hopes grew that the Middle East war was moving toward a resolution, the KOSPI surged 8.44%. The next day, on the 2nd, it plunged 4.47% after U.S. President Donald Trump unleashed a “bombshell” in a national address. In March as well, amid concerns over the war’s impact, the KOSPI market saw buy-side sidecars triggered three times and sell-side sidecars four times.

The most direct channel through which the Middle East war is shaking equities is global oil prices. Since the war broke out, international crude prices have been hovering around the $100-a-barrel level for West Texas Intermediate (WTI). If soaring oil prices stoke inflation, the U.S. Federal Reserve’s policy rate cuts that the stock market had been anticipating become more distant. Tighter liquidity is also negative for equities, while concerns are mounting that elevated interest rates could dent the economy.

Yoo Myung-gan, an analyst at Mirae Asset Securities, said, “Given that inflation pressures from rising oil prices make it highly likely that rate declines will remain limited for the time being, valuation metrics may become more important,” adding, “A strategy focused on sectors with clear earnings improvement or strong price-to-book (PBR) appeal would be advantageous.”

Hankyung.com, using FnGuide’s DataGuide service, selected 14 stocks that met both criteria: △their first-quarter operating profit consensus had been revised up by at least 10% since the start of the year through the 3rd, and △their PBR based on end-of-last-year financial statements was below 1. The screen identified names with improving earnings outlooks and attractive PBR valuations.

Middle East war beneficiaries such as SK Innovation, HMM and Daehan Petrochemical draw attention first. Compared with the start of the year, their first-quarter operating profit consensus has been revised up by 78.84%, 65.18% and 19.79%, respectively.

In the case of SK Innovation, higher global oil prices directly expand profit scale, as the value of previously purchased crude rises, generating inventory valuation gains. However, inventory valuation gains are book profits with no cash inflow. The currently tallied first-quarter operating profit consensus is 658.5 billion won.

HMM’s share price has not swung as sharply as other shipping names in this phase of the Middle East war. However, the Shanghai Containerized Freight Index, which directly affects container carriers’ performance, has surged 37% since the war began. Jeong Yeon-seung, an analyst at NH Investment & Securities, said, “While there are concerns about demand slowing for container transport due to the war, for now supply issues stemming from operational disruptions are having a bigger impact, making cost pass-through possible.”

Korean Air is also being classified as a beneficiary of the Middle East war. Since the start of the year, its first-quarter operating profit consensus has been revised up by 14.91% to 40.9 billion won. Choi Ji-woon, an analyst at Yuanta Securities, said, “Operational disruptions at Middle East airports due to the war led to a reshuffling of demand toward Asian hub airports such as Incheon International Airport,” adding, “As a spillover benefit, demand for Korean Air’s U.S. and Europe routes has expanded.”

Han Kyung-woo, Hankyung.com reporter case@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.