Europe Property Slump Deals Blow to South Korea’s ‘National REIT’ as JR Global Defaults, Freezing $139 Million of Retail Money

Summary

- JR Global REIT became the first listed REIT to default, and with trading suspended and a delisting review under way, about 200 billion won ($139 million) in retail investor assets has been frozen.

- REIT ETFs holding the stock, including TIGER Real Estate Infrastructure and PLUS K-REIT, can no longer rebalance, while a wider NAV gap and weaker liquidity provision have made it harder to trade at fair value.

- JR Global REIT was pushed toward insolvency despite remaining profitable, hit by high interest rates, a surging won-euro exchange rate, a drop in European property values and a cash trap, underscoring the need to reexamine the listed REIT market’s overall risk-management framework.

Forecast Trend Report by Period

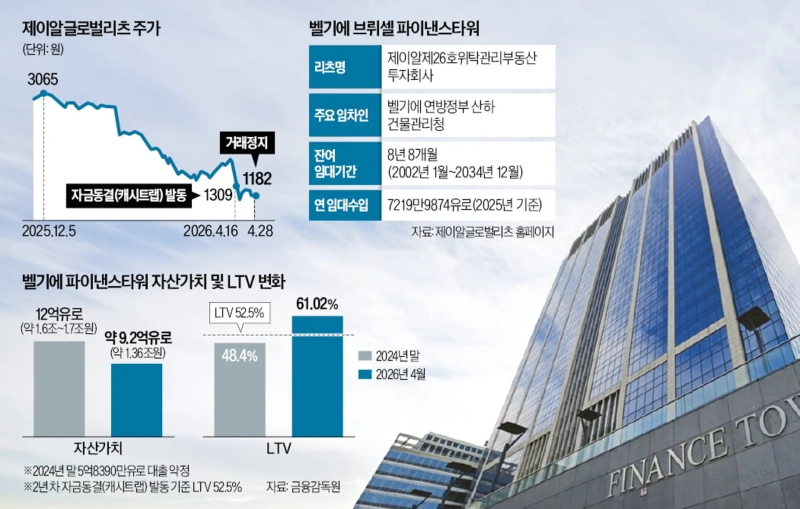

JR Global REIT made a high-profile stock market debut in 2020 as South Korea’s first publicly offered REIT focused on overseas real estate. Once dubbed a “national REIT” on the back of annual dividend yields in the 7% range and the Belgian government as a blue-chip tenant, it has now earned the distinction of becoming the first listed REIT in South Korea to default. The episode is fueling concern that distrust could spread across the broader listed REIT market.

Shockwaves Spread to REIT ETFs

As of the end of last year, 28,200 retail shareholders owned JR Global REIT shares, holding 73.63% of the company, according to the securities industry on April 28. Mirae Asset Global Investments held 8.51% through client accounts, while Samsung Asset Management held 5.05%. Including indirect holdings through REIT ETFs, individual investors account for about 90% of ownership. Based on the company’s current market capitalization, roughly 200 billion won ($139 million) in retail investor assets has effectively been frozen. Investors cannot sell their shares until a decision is made on delisting or the rehabilitation process is completed.

Shareholders face a long wait to recover funds. If the Autonomous Restructuring Support program is activated, a court can postpone the start of formal rehabilitation proceedings for as long as three months while creditors negotiate. If those talks fail and the company enters full court-led rehabilitation, approval of a restructuring plan typically takes more than a year.

Investors in REIT ETFs also face fallout. ETFs that hold JR Global REIT, including TIGER Real Estate Infrastructure and PLUS K-REIT, cannot rebalance their portfolios. If the trading suspension clouds valuation of the underlying asset, the gap between an ETF’s net asset value and its market price can widen and liquidity provision can shrink. That makes it harder for investors to trade ETF shares at fair value.

Bonds issued by JR Global REIT can still be traded, though finding buyers is likely to be difficult. The company’s credit rating was downgraded last month to BBB+ from A-. It was cut again to speculative-grade BB+ on April 27 and then to D, indicating default, on April 28. JR Global REIT has 389 billion won ($271 million) in marketable debt, including 40 billion won ($27.8 million) in short-term electronic debt and 339 billion won ($236 million) in public bonds. Much of that is understood to be held by retail investors.

Profitable on Paper, Undone by Rates, Foreign Exchange and Lenders

As of the end of last year, JR Global REIT remained profitable. It had 99.4 billion won ($69.1 million) in cash and cash equivalents and posted net profit of 16.2 billion won ($11.3 million). But an asset freeze, or cash trap, imposed by a Belgian financial company choked off funding flows and pushed the REIT toward insolvency despite positive earnings.

High interest rates and the surge in the won-euro exchange rate are at the heart of the crisis. When JR Global REIT acquired Belgium’s Finance Tower, the interest rate on secured loans from a Belgian financial company was only in the 1% range. During refinancing at the end of 2024, that jumped to 4% to 5%. As European property values fell and the loan-to-value ratio climbed, the local lending group triggered a cash trap on April 16, requiring rent and other cash flow to be used first to repay the Belgian financial company’s loans.

The company was also hit by settlement costs tied to currency hedges as the won-euro exchange rate soared. JR Global REIT had hedged 100% of its investment. Over the past three years, the exchange rate rose more than 27% to about 1,720 won per euro from around 1,350 won, generating roughly 100 billion won ($69.6 million) in settlement costs.

JR Global REIT has started legal action, including a challenge in a UK court, arguing that the Belgian financial company undervalued Finance Tower. It has also said it will sell a Manhattan building in the US to reduce its debt burden.

Market watchers warn the episode could spread risk aversion across the listed REIT sector. The combined market capitalization of South Korea’s 25 listed REITs stands at 10.7 trillion won ($7.44 billion). “A funding structure built in an era of low interest rates has run into structural limits in a high-rate environment,” an investment banking industry official said. “This is the time to reexamine the risk-management framework for the REIT market as a whole.”

Choi Seok-cheol and Bae Jeong-cheol, Korea Economic Daily reporters, dolsoi@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.