PiCK

Strategy Wobbles as STRC Stays Below Par, Reviving Fears of Four-Year Crypto Bust

Summary

- Strategy, the world’s largest corporate Bitcoin holder, has seen its preferred stock STRC trade below par, lifting its annual dividend rate to 11.5% and fueling concern over shareholder dilution and cash strain.

- Industry concerns are growing over a Bitcoin bear market, cash-flow risk, a four-year crash cycle, and even the possibility of Terra-Luna 2.0, with some saying Strategy faces pressure to sell Bitcoin or raise additional funds.

- Some experts, however, say it is a stretch to equate STRC with Luna-Terra, adding that despite weaker fundraising efficiency, Strategy is unlikely to sell its 840,000 Bitcoin all at once.

Forecast Trend Report by Period

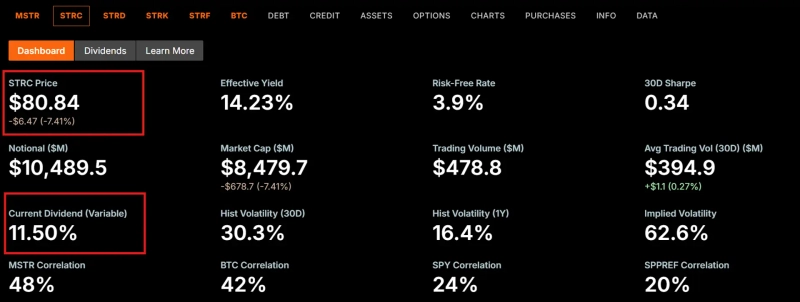

STRC remains below par for an extended stretch

Warnings mount over cash-flow risk

Some raise fears of a second Terra-Luna

Others say the concern is excessive

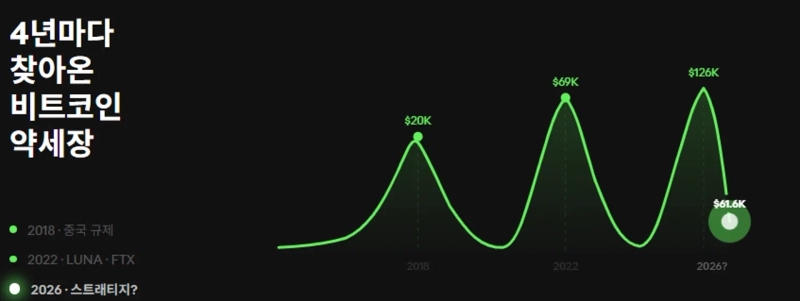

Concern is mounting around Strategy, the world’s largest corporate holder of Bitcoin, as the cryptocurrency’s slump drags on. Some investors are questioning whether the crypto market’s four-year crash cycle is resurfacing.

Yahoo Finance data showed Strategy’s preferred stock STRC closed at $75.69 on Nasdaq on June 25, down 6.37% from the previous session.

STRC is a dividend-paying preferred stock Strategy launched in July 2025 to fund Bitcoin purchases. It was issued with a $100 par value and a 9.0% annual dividend. The structure allows the company to raise the dividend rate if the shares trade below par to attract buyers. With Bitcoin in a downtrend since October 2025, STRC’s annual dividend rate has risen to 11.5%.

The issue is that STRC continues to trade below par despite repeated dividend increases. Bitcoin’s prolonged weakness has weighed on the stock. STRC held at its $100 par value through May 14, but has traded below that level for 30 straight trading days since May 15.

That is fueling market concern. When STRC trades below par, Strategy must issue more preferred shares to raise the same amount of money, diluting shareholder value in the process. For example, the company previously needed to sell 10 million STRC shares to raise $1 billion. At current prices, it would need to issue 12.5 million shares to raise the same amount through STRC.

A larger preferred issuance would also increase Strategy’s dividend bill. The company’s annual dividend obligation to STRC investors now stands at $1.2 billion. That could add to its cash burden.

Even so, Strategy appears committed to continuing the strategy. Chief Executive Officer Phong Le bought 1 million STRC shares on June 23 and declared he would not sell until STRC returns to par.

Coincidence or not? Could the four-year crash cycle return?

As Strategy, the publicly traded company with the world’s largest Bitcoin holdings, comes under pressure, fear is spreading in the crypto community that a rout like the one the industry suffered four years ago could return. Influencer Kyle Chasse wrote on X that some market participants worry Strategy could drag Bitcoin lower with it. Some are calling it “Terra-Luna 2.0,” he added.

The crypto market has experienced bear markets on a four-year cycle.

In 2022, the market tumbled after the Terra-Luna collapse was followed by the bankruptcy of FTX. Bitcoin fell more than 70% from its then-record high of $69,000 in November 2021 to the $15,000 range.

The market also suffered a bear phase in 2018, eight years earlier, as remarks by former South Korean Justice Minister Park Sang-ki about shutting crypto exchanges, China’s mining ban and bearish views from prominent global scholars hit sentiment.

As of 2026, Bitcoin is again trading near the low end of its cycle. At 5:20 p.m. on June 26, it traded at $59,185, down 2.57% from a day earlier, according to CoinMarketCap. That is about 54% below its all-time high of $126,272 reached in October 2025.

Industry outlooks diverge

A number of industry experts have recently raised concerns about Strategy’s business structure.

Zach Pandl, head of research at Grayscale, said on a recent podcast that Strategy’s problem is not Bitcoin but cash flow. Bitcoin does not generate interest income. If its price does not rise, the only ways to pay preferred dividends are to sell Bitcoin or raise fresh funds, and neither is desirable.

On-chain data firm CryptoQuant also recommended that Strategy halt Bitcoin purchases for now and focus on building cash reserves. Julio Moreno, the firm’s head of research, said dividend obligations are rising quickly while cash holdings are shrinking. Restoring cash reserves and dividend-paying capacity before resuming Bitcoin purchases would be the most direct way to rebuild market confidence.

Others argue the concern around Strategy is overdone.

Mark Palmer, an analyst at Benchmark Research, wrote in a report that comparing STRC with Luna and Terra is inappropriate. STRC has a $100 par value, but it is not a stablecoin that guarantees that price. The current situation reflects weaker fundraising efficiency, not a collapse of the business model itself.

Kim Min-seung, head of the Korbit Research Center, said the dividend burden tied to STRC does appear to have grown. Even so, he said, Strategy is unlikely to dump its roughly 840,000 Bitcoin holdings on the market all at once.

Uk Jin

wook9629@bloomingbit.ioH3LLO, World! I am Uk Jin.