"Bitcoin proves resilience and profitability … reaches $300,000 within a year"

Summary

- "Bitcoin" has increased investor interest due to expanded touchpoints with institutional finance, and it was stated to show high resilience and profitability in the long term.

- The U.S. expansion of stablecoin policy and digital asset discussions have strategic significance for maintaining dollar dominance and complementing Treasury demand.

- Introducing a domestic won stablecoin is necessary for securing monetary sovereignty and enhancing global competitiveness, but it was noted that introducing it without sufficient regulatory preparation could cause financial market disruption.

Recently, as discussions on digital currencies and stablecoins at home and abroad have rapidly spread, experts gathered in one place to review the financial environment and policy responses. Attendees emphasized that technological innovation, financial stability, and regulatory readiness must be considered simultaneously, and that stablecoins will become a core infrastructure for international payments and securing monetary sovereignty beyond being mere virtual assets

[Market] Money Talk

The global financial order is rapidly being reorganized by the adoption of blockchain and digital currencies. The listing of Bitcoin exchange-traded funds (ETFs), the spread of stablecoins, and discussions on central bank digital currencies (CBDCs) in various countries are shaking the bank-centered financial system and opening a new paradigm.

Blockchain and digital currency experts such as Kim Jong-seung, CEO of Excrypton; Kim Pil-gyu, Senior Research Fellow at the Korea Capital Market Institute; and Jung Yoo-shin, Professor of Business Administration at Sogang University (in alphabetical order) gathered to analyze Bitcoin investment strategies, CBDCs, and the feasibility and social impact of introducing a won-denominated stablecoin from multiple angles. They emphasized that technological innovation, financial stability, and regulatory readiness must be considered simultaneously.

\- Stablecoins have been in the spotlight recently. Please briefly tell us how you felt about coins moving from the margins to the center.

Jung Yoo-shin, Professor, Department of Business Administration, Sogang University (hereafter Professor Jung) "While teaching the course 'History of Finance,' I viewed technological development and infrastructure changes from a historical perspective. I see the current process as a change in the bank-centered financial system. The fact that the U.S. chose stablecoins is related to the threat to dollar dominance caused by digitalization and the emergence of CBDCs. During the Russia–Ukraine war, Russia's banks were excluded from the interbank payment network (SWIFT), yet the Russian economy operated without banks. This led the U.S. to realistically accept the digital dollar. It also shifted policy toward strategically utilizing stablecoins. I view liquidity stages as M0 (central bank) through M5 (digital assets). Up to M3 (capital markets) can be controlled by the banking system, but from M4 (derivatives & securitized assets) there are limits to banks alone, and M5 requires blockchain/on-chain systems. New financial infrastructure should include both banks and blockchain."

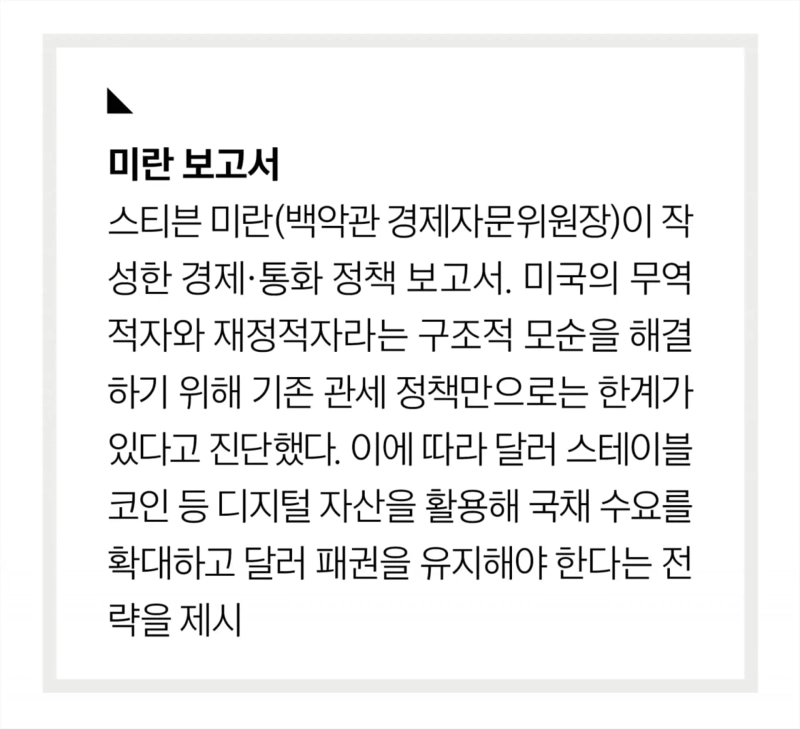

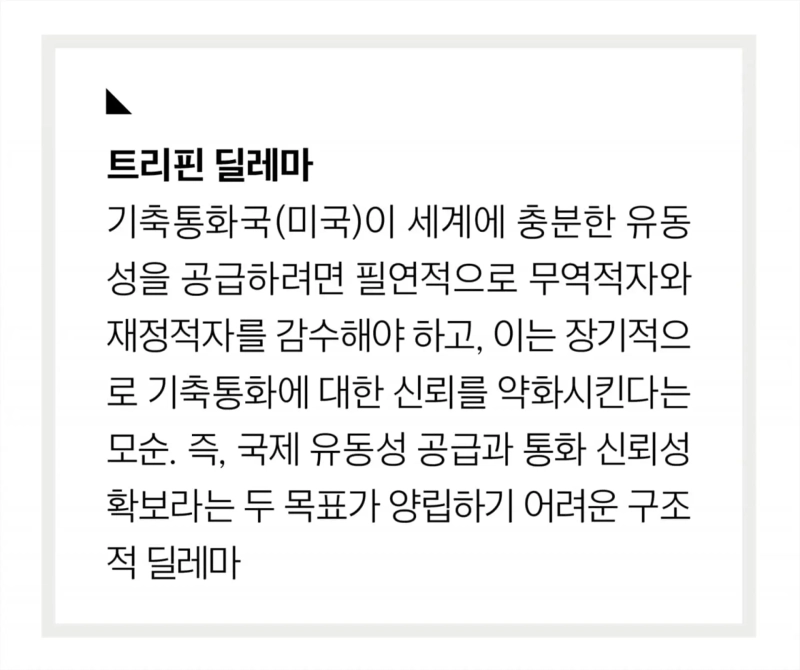

Kim Jong-seung, CEO of Excrypton (hereafter CEO Kim) "U.S. digital asset policy changed significantly around the Trump administration. I think the background includes a strong sense of crisis about the dollar system. The reserve currency system began with the 1944 Bretton Woods system. At that time, some proposed a supranational currency called 'Bancor,' while others supported making the dollar, linked to gold, the reserve currency. The dollar-centered system was maintained for over 80 years, but the U.S. has faced a structural contradiction requiring it to accept fiscal deficits and deteriorating trade balances to supply global liquidity. In the 1960s, Yale professor Robert Triffin pointed out the 'Triffin dilemma,' which remains unresolved. According to a recent report by Steven Mnuchin, Chair of the White House Council of Economic Advisers, the U.S. proposed tariffs to break through this contradiction. But tariffs create discord between countries and are not an ultimate solution. Therefore, I think it is important that the U.S. began seriously discussing digital assets as a way to overcome this limit."

Kim Pil-gyu, Senior Research Fellow, Korea Capital Market Institute (hereafter Senior Researcher Kim) "We are analyzing issues that may arise when stablecoin companies hold Korean won. Currently, Korea lacks short-term government bonds. There are no one-year bonds, and issuance of two-year bonds began in 2021. The Ministry of Economy and Finance is reviewing the introduction of one-year issuance, but issuing three-month bills is difficult due to restrictions on expanding issuance scale under the National Finance Act. In a research institute seminar comparing Bitcoin prices and stock prices, generational differences in investment patterns were clearly observed. Before 2020, stock prices and Bitcoin prices moved differently, but since 2021 they have moved in the same direction. This suggests that Bitcoin has begun to be incorporated into the institutional sphere. With touchpoints with institutional finance expanding through ETF launches, investor interest has surged. To support such changes, the importance of payment means like stablecoins and CBDCs is increasing. Personally, I distinguish that crypto assets like Bitcoin have the character of financial investment products, while stablecoins and CBDCs have the nature of currencies supporting payments."

\- Can you explain the recently passed 'Genius Act'?

Professor Jung "The core of creating a digital asset, that is, a virtual asset ecosystem, is the stablecoin. Bitcoin started as money but was classified as an asset due to high price volatility; with the advent of stablecoins, it settled as a medium of exchange. Stablecoins began in the virtual asset realm but, with technological and infrastructure development, have spread to the entire financial area such as remittance and payments. Especially through international remittance cases, it has been confirmed that they can function as money. The bill was prepared so that stablecoins can be established not merely as a medium of exchange but as a currency usable in various financial transactions such as payments and remittances."

Senior Researcher Kim "So far, stablecoins have been mainly used in coin trading, accounting for about 90% of total transactions. In terms of universality, they cannot yet be said to be widely used. Stablecoins can be broadly divided into three types. First, fiat-backed; second, crypto-collateralized; third, algorithmic. The Genius Act mainly focuses on fiat-backed types. Corporations are already using stablecoins to back up commerce and are gradually expanding universality. In the past, stablecoins might have been seen simply as for coin trading, but usage is expanding. Although it will take time, they may gradually take root in people's daily lives."

CEO Kim "Looking at several mentions by the U.S. Treasury Secretary about dollar stablecoins, the U.S. is paying attention to them for bond market and interest rate stability. Dollar stablecoins focus their reserve assets on U.S. Treasuries, dollar cash, and short-term government bonds. Government-issued money market funds (MMFs) are included, but most are Treasuries. An interesting point is that stablecoins can be effective in lowering bond yields, which contributes to easing the fiscal deficit. If combined with tariff policies, the U.S. could maintain the structure of supplying dollar liquidity globally while improving the trade balance. Stablecoins also have a liquidity-creation effect, for example reducing a traditional three-day settlement to within an hour. Ultimately, dollar stablecoins can play a strategic role combined with tariff policy to improve the U.S. trade balance and maintain dollar dominance. However, dollar-denominated stablecoins cannot completely solve structural contradictions like the Triffin dilemma. Diversification of reserve assets will be needed, and Bitcoin may be included as a representative alternative in that process."

\- If dollar stablecoins are introduced, I'm curious whether trust can be guaranteed regarding various collateral values.

Professor Jung "I think dollar stablecoins should be approached within the dollar supply-demand structure. Combined with tariff policy, they can alleviate problems the U.S. faces, such as the interest burden on Treasuries and fiscal deficits, and can meaningfully support the collateral value of U.S. Treasuries. Also, through stablecoin-based dollar exchange rate management, unnecessary fluctuations from dollar strength can be adjusted immediately, and necessary dollars in terms of trade and capital accounts can be supplemented. Stablecoins are not simple virtual asset trading but can be used as financial and trade payment means, effectively covering reductions in dollar demand linked to tariff barriers. China cannot immediately follow with on-chain-based stablecoins due to financial vulnerabilities, so the U.S. will likely retain policy advantages for the time being. The U.S. also takes on new institutional risks, but I think the policies currently being implemented are very wisely designed."

Senior Researcher Kim "One core problem the U.S. faced even before Trump was the composition of Treasury investors. Countries like Japan and China hold many Treasuries, so diversifying Treasury demand was important. With stablecoins' introduction, reserve assets will absorb a substantial portion of Treasury demand, and last year U.S. short-term Treasury (T-bill) issuance reached a record high. The existence of stablecoins can complement such Treasury demand and, combined with policies like gift tax laws, may help alleviate several issues the U.S. faces."

\- How will the dollar's value be in the future stablecoin era?

CEO Kim "I expect the U.S. will deliberately continue to intervene in the dollar's value. Looking at what was mentioned in the 'Mar-a-Lago agreement,' even if it is not realistic for countries to directly negotiate exchange rates as in the past, similar attempts will continue. If the strong dollar trend continues, the U.S. will find it difficult to escape that trap, so it will have to pursue a weak-dollar policy indirectly. Regardless of dollar stablecoins, the U.S. must transition this policy. The 'Miran report' mentioned this context several times. Personally, I judge that the currency spike observed until early this year will not reoccur."

Senior Researcher Kim "Stablecoins should not be seen too narrowly. With their introduction and linkage to reserve assets, unlike endlessly issued currencies, they will be managed in a decentralized manner. In the past, central banks controlled all currency, but now currency-like types are increasing according to the number of users and demand. If money supply increases, the dollar value may fall, but the correlation is not large. The U.S. intends to pursue a weaker dollar to protect domestic industries, and stablecoins are expected to have some influence."

Professor Jung "Essentially, structurally the U.S. will further deepen its trade deficit, making dollar weakness inevitable. Dollar weakness via market mechanisms is needed to resolve deficits, but as the reserve currency, the U.S. cannot tolerate losing the dollar's status. Therefore, it must strike a balance without abruptly changing the dollar's value, and adjust by means other than price mechanisms. That is, through tariff cooperation or negotiation to maintain dollar value and resolve trade deficits via non-price factors. At the same time, a structure is formed where stablecoins connect to maintain global dollar demand and ease fiscal deficit burdens. In the long term, the dollar may trend weaker, but stablecoins defend against sudden weakness. In terms of liquidity, stablecoins can provide dollars more flexibly and quickly. This is possible without direct intervention in foreign exchange markets, and the dollar can maintain strength for a certain period. Dollar demand will persist, and while moving toward weakness in the long term with liquidity, excessive concern is unnecessary."

\- In the U.S., if private stablecoins adopt monetary functions, the status of the central bank could be weakened.

Senior Researcher Kim "Central banks in any country maintain a negative stance toward stablecoins because they are strongly attached to centralized currency supply. One insight I had while studying stablecoins is that, similar to past free banking (where private banks freely issued currency), currency can be supplied in various ways. In Hong Kong, for example, structures issuing currency under regulation still exist. The Genius Act's basic spirit appears to center on using stablecoins with regulation while reducing CBDC. However, from a central bank's perspective, they remain very negative about the emergence of a new currency that they do not control."

\- When the Trump administration pursued stablecoins, did the U.S. effectively abandon the CBDC issue, or is it considering both?

CEO Kim "The U.S. showing a negative stance toward CBDC is largely about checking movements by China and Europe. Since BIS-led CBDC projects are ultimately progressing centered on Europe and China, it is important for the U.S. to counterbalance that. The 'Agora project' that the U.S. participated in includes seven countries, including Korea, with the International Institute of Finance (IIF) taking the role of private financial institutions. The U.S. does not simply abandon CBDC but appears to be continuously preparing CBDC projects while countering Europe and China."

\- How might CBDC merge with dollar stablecoins?

Professor Jung "There is a 'deposit token (JPMD) project' recently launched by JPMorgan. The difference between this project and dollar stablecoins is clear. First, deposit tokens are subject to deposit insurance laws, while stablecoins are not. Regarding reserve assets, deposit tokens hold 100% stablecoins. From a financial institution's perspective, JPMorgan is exploring entry into the dollar stablecoin market while attempting to issue deposit tokens using existing infrastructure. When issuing deposit tokens, wholesale CBDC would be used for settlement between financial institutions. Therefore, the U.S. is more likely to adopt wholesale CBDC rather than retail CBDC, and related projects are expected to continue."

\- Where do you see Bitcoin's price in a year, and should one invest now?

Professor Jung "On a one-year basis, I expect around $300,000."

CEO Kim "Looking at past 10+ years of data, even if purchased at an all-time high, it has always recovered within four years. Even the lowest return over a 2–3 year period was over 16%. That is, regardless of when you buy, even if prices fall temporarily, recovery likelihood is high, and in terms of returns it has been more stable than other financial products. As of May 10 this year, analyzing Bitcoin prices shows the longest time for an investor to recover their purchase price was 3 years and 3 months, i.e., 1,188 days. Also, when held for five years, the lowest return was 16.89% and the highest return reached 14,038%. Long-term, it has shown considerable resilience and profitability."

Senior Researcher Kim "Previously Bitcoin moved freely in a market completely separate from the stock market, but recently, with related financial investment products and ETFs emerging, correlation with stocks has greatly increased. The question is who influences whom. Does Bitcoin affect the stock market, or does the stock market pull Bitcoin up? Investors seem to expect higher returns from Bitcoin than recent stock returns."

Professor Jung "We need to see how Bitcoin and blockchain-based systems will combine with existing financial infrastructure. Currently, only a very small proportion, about 2–3% of total financial transactions, occur on blockchain, but I expect this to expand to about 5% by next year. In this process, blockchain networks will operate and various transactions will occur, with Bitcoin playing a central role. Similar to how total value in real estate gets distributed over a certain period and region, blockchain infrastructure will gradually expand. The direction is clear, but the actual timing and speed will take time."

\- How do you view the possibility that Bitcoin investment could weaken workers' motivation to work?

Professor Jung "It's important that finance and the real economy meet. When finance and the real economy meet, money can flow into productive functions rather than bubbles or mere money games. There is the primary market (issuance market) and the secondary market (circulation market); if it stays only in the secondary market, bubbles can form. Therefore, coins should be connected to the issuance market and used as productive fundraising tools. Currently coins are not assets representing a company's ownership but are assets themselves, but they can be connected as a means of fundraising. I think the fusion of the existing joint-stock company system and coins is in progress."

Senior Researcher Kim "We are considering ways to introduce stablecoins as international coins linked to real economy and connected to the productive parts of the primary market. For example, tokenizing government bonds could diversify investors and promote active trading. Although correlation between the stock market and coins has increased, tasks remain to link them productively to work and production."

Professor Jung "From a fundraising perspective, fundraising using tokenized securities and real assets is already underway. Now, on-chain tokenization allows assigning value to illiquid assets and raising funds. From a global perspective, the secondary market has reached a level where it can be used productively rather than as a mere money game. In other words, productive fundraising through coins is already being realized."

\- At this point, is introducing a won stablecoin appropriate, and what responses are needed?

Professor Jung "I think it must be introduced unconditionally. Since the Genius Act has already been enacted, stablecoins are not simple coins. If there is a digital dollar, there must be a digital won, and it should operate on-chain rather than within the banking system. Whether it is used is something we can induce, and this can legally resolve issues of monetary sovereignty and exchange rates. Regulatory issues like customer due diligence (KYC) can be sufficiently addressed on existing blockchains like Ethereum, and if domestic authorities coordinate internationally with financial authorities, it can be implemented without problem. Using a digital won can make transactions transparent and immediate in large corporations and international trade, reducing delays and costs due to exchange rate fluctuations. Properly utilized, it can create strategic opportunities in international capital markets."

CEO Kim "I think reviews of the impact of a won stablecoin on monetary policy and foreign exchange policy are not yet sufficient. While discussion of introduction is positive, rushing to implement without thorough discussion of impacts on central bank monetary policy, foreign exchange policy, and potential market disruption in financial markets is negative."

Senior Researcher Kim "Proponents of introducing a won stablecoin emphasize advantages such as increasing the use of the won in global digital competition, mitigating weakening of monetary sovereignty, and supporting won-based coin trading. However, if introduced without proper regulation, it could cause major disruption. I support the introduction of legislation, but a thorough regulatory approach is necessary. Rather than introducing it immediately in the absence of regulatory or legal frameworks and causing market disruption, we should prepare related regulatory systems and systems first."

Han Sang-chun, international finance correspondent and editorial writer at The Korea Economic Daily | Compiled by Reporter Lee Hyun-ju | Photo by Reporter Lee Seung-jae

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.