U.S. SEC begins easing virtual-asset regulations…pushes safe-harbor and system reform

Summary

- The U.S. SEC announced it had formalized a regulatory-relief agenda that includes virtual assets, safe-harbor provisions, and institutional reform.

- The agenda reportedly includes clarifying regulations for the issuance and sale of virtual assets, the introduction of specific exemptive rules, reflecting virtual-asset trading on alternative trading systems and national securities exchanges, and easing broker-dealer reporting obligations.

- It said that with the SEC shifting to a virtual-asset-friendly stance, regulatory burdens are expected to decrease, market certainty to increase, and the investment environment to improve.

The U.S. Securities and Exchange Commission (SEC) has formalized a policy of easing regulations on virtual assets (cryptocurrencies). Unlike the past, when conservative regulation drew heavy criticism, the new agenda largely includes safe-harbor provisions (clauses in laws or regulations that state certain conduct is not considered a violation of a particular rule) and a comprehensive overhaul of the regulatory framework to support projects.

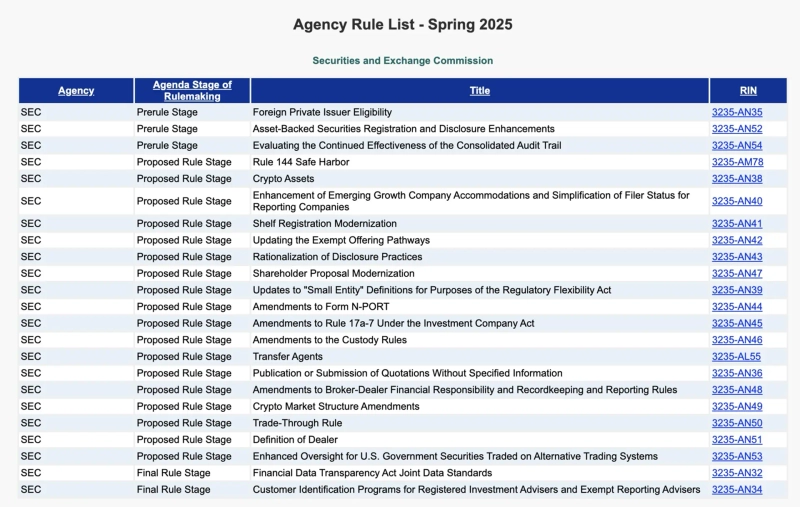

On the 4th (local time), Cointelegraph reported that the SEC released draft proposals for about 20 rulemakings in its "Spring 2025 regulatory agenda." The SEC's agenda aims to clarify the regulatory framework for the issuance and sale of virtual assets to provide greater certainty to the market.

The agenda included specific exemptive rules for the issuance and sale of virtual assets, the introduction of safe-harbor rules, and amendments to the Securities Exchange Act reflecting virtual-asset trading on alternative trading systems (ATS) and national securities exchanges. This is expected to reduce regulatory burdens for virtual-asset firms and mitigate legal risks.

It also proposed revising broker-dealer financial responsibility rules to relax reporting obligations for virtual-asset firms. The industry has argued that those rules effectively imposed customer identification (KYC) and anti-money laundering (AML) requirements on virtual-asset networks, creating an excessive burden.

A proposal to amend the Investment Advisers Act of 1940 also drew attention. As recently as eight months ago, the SEC sought to apply stricter custody rules to digital assets, but this time it has revised them to accommodate virtual assets.

However, the proposal is still at the agenda stage; public hearings, comment collection, and review procedures remain before any actual implementation. Nonetheless, it is clear that the SEC has shifted to a virtual-asset-friendly stance since former Chair Gary Gensler's resignation in January. Chair Paul Atkins may exercise some authority to shape the interpretation and enforcement of virtual-asset-related rules, making future changes noteworthy.

Doohyun Hwang

cow5361@bloomingbit.ioKEEP CALM AND HODL🍀