PiCK

A pledge by President Lee—but Bitcoin spot ETFs remain in limbo as the framework act stalls

Summary

- Delays in discussions on the Digital Asset Framework Act are making it difficult to introduce spot crypto ETFs, and passage in the first half of this year may also be challenging.

- It said that the framework act is needed for virtual assets to be incorporated as underlying assets within the regulated financial system and to create grounds for building custody and OTC infrastructure.

- It warned that if legislation is delayed, Korea could fall behind in competition with major countries such as the U.S., where the spot ETF market worth hundreds of trillions of won has formed, and that domestic market competitiveness could weaken.

Forecast Trend Report by Period

As talks on the Digital Asset Framework Act stall

the rollout of crypto ETFs is also being repeatedly delayed

the U.S. has already built a market worth ‘hundreds of trillions of won’

Industry: “Preparations may have to come to a complete stop”

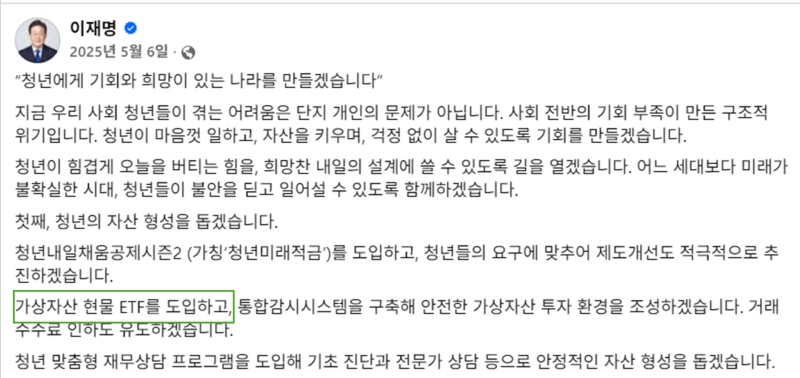

The introduction of domestic spot exchange-traded funds (ETFs) for virtual assets (cryptocurrencies)—a campaign pledge by President Lee Jae-myung—is being delayed. The war involving Iran has pushed back, time and again, legislation of the Digital Asset Framework Act, which is intended to provide a legal basis for spot crypto ETFs.

According to political circles on the 2nd (Korea time), the Digital Asset Framework Act was not placed on the agenda of the Legislation Review Subcommittee of the National Policy Committee meeting held on the 31st of last month. Even the Democratic Party’s party-government policy consultative meeting on the bill, originally slated for last month, was postponed, leaving key contentious issues—such as limits on controlling shareholders’ stakes in crypto exchanges—unresolved. A Democratic Party official said, “With many urgent issues related to the Middle East conflict, discussions (on the framework act) are being delayed,” adding, “There is internal consensus that the act should be processed quickly, but given the circumstances, passage in the first half of this year may be difficult.”

With matters unfolding this way, the rollout of spot crypto ETFs has also fallen into a fog of uncertainty. Legally, ETFs must track assets that are recognized as eligible underlying assets, but virtual assets are not recognized as underlying assets under current law. In other words, without a framework act, introducing spot crypto ETFs is effectively impossible. A look at the National Assembly’s legislative docket shows that versions of the Digital Asset Framework Act introduced by Democratic Party lawmakers Min Byung-duk and Park Sang-hyuk, and by People Power Party lawmaker Kim Jae-seop, explicitly state grounds for incorporating virtual assets as underlying assets within the regulated financial system.

Custody and OTC overhauls are also tasks

Overhauling custody (safekeeping) and the over-the-counter (OTC) trading framework is also cited as a key task. For a Korean asset manager to run a spot crypto ETF, it must actually hold the virtual assets that serve as underlying assets, such as Bitcoin (BTC) and Ethereum (ETH). From the asset manager’s perspective, this requires institutional-grade custody infrastructure to store purchased crypto securely, as well as an OTC system that can buy large amounts of crypto without causing market shock.

The problem is that, under the “separation of finance and commerce” principle, there is also insufficient legal basis for businesses that store and trade crypto assets. The industry expects that enactment of the framework act would establish an institutional foundation for building crypto custody and OTC infrastructure. Indeed, most of the lawmaker-sponsored framework bills already submitted to the National Assembly specify provisions to subdivide related business categories—such as trading, brokerage, custody, and management of digital assets—and to introduce a licensing regime by sector.

Industry fears: “We’ll miss a ‘300 trillion won’ market”

Of course, even if the framework act is enacted, that does not mean spot ETFs can be launched immediately. There are many elements to prepare beyond legal grounds, including crypto price and index calculation systems and the liquidity provision structure.

Still, as the framework act could be the starting point for introducing spot crypto ETFs, calls are growing for swift legislation. Cho Jin-seok, CEO of Korea Digital Asset (KODA), said, “The very first step toward introducing spot ETFs is enacting the framework act,” adding, “If bill discussions are delayed, the industry will have no choice but to halt preparations (for related businesses).” He said, “Asset managers and related businesses are also preparing (for crypto ETFs) with the ruling party’s pledge in mind, but the continued legislative delays are deeply disappointing.”

There is also concern that the later the launch, the weaker Korea’s market competitiveness will become. The U.S. spot Bitcoin ETF industry has already grown into a market worth $100 billion (about 152 trillion won). That is the result achieved in just two years since trading first began in 2024. In September last year, when the crypto market entered a bull phase, the market size even came close to $200 billion (about 300 trillion won) at one point.

Major economies are also moving quickly to introduce spot crypto ETFs. Hong Kong, aiming to become Asia’s “crypto hub,” introduced spot crypto ETFs early in 2024, and the U.K. approved trading of spot crypto products via the exchange-traded note (ETN) structure. Japan is pushing institutional reforms with a goal of introduction by 2028.

A financial industry official said, “Because virtual assets are global assets, without spot ETFs we cannot compete fairly with overseas markets,” adding, “If the current lack of institutional foundations continues, the competitiveness of the domestic market will inevitably decline.” The official added, “Compared with other crypto products such as security token offerings (STOs), spot ETFs have a relatively simple structure and strong investor demand; once the relevant laws are put in order, a market could form quickly in Korea as well.”

Uk Jin

wook9629@bloomingbit.ioH3LLO, World! I am Uk Jin.