Oil prices surge as ceasefire recedes… Could it become a ‘Hormuz moment’ that shakes U.S. hegemony?

Summary

- It said WTI and Brent prices have surged in the global oil market and backwardation has intensified, heightening concerns over a near-term supply shortage.

- It reported that Iran’s demand for transit fees in yuan or coins, along with the widening shift away from dollar settlement in crude-trade payments, is deepening cracks in the petrodollar system.

- It said markets are betting on a prolonged Middle East war, with analysis pointing both to the possibility of further oil price gains and to short-term spike factors tied to short squeezes.

Forecast Trend Report by Period

‘Anomaly signals’ in the international crude market

WTI May contract posts the widest gap vs. June

Driven by mounting fears of a near-term supply crunch

Like the ‘Suez moment’ that broke British primacy

Cracks in dollar-based trading erode U.S. influence

In October 1956, Britain formed a coalition with France and Israel and invaded Egypt after Cairo nationalized the Suez Canal—then managed by the UK—in July that year. What initially favored the coalition flipped when Egypt blocked the canal by sinking dozens of ships. Unable to find a solution, Britain and its partners withdrew from Egypt in humiliation after just nine days. The episode is the so-called “Suez moment,” widely seen as signaling the end of Britain’s already waning hegemony.

As the Middle East war drags on longer than expected, forecasts are spreading that an “American version of the Suez moment” may be approaching. With international oil prices surging—and even cracks emerging in the “petrodollar” (dollar-denominated crude trading)—Washington’s standing is being shaken.

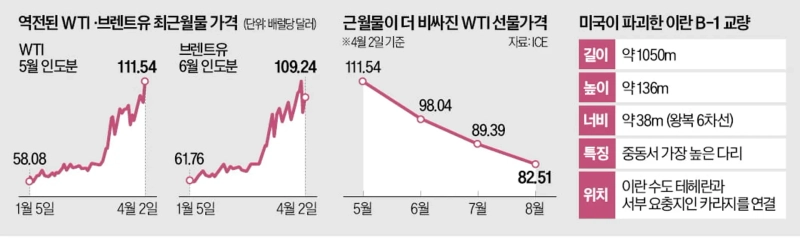

◇Oil prices post the biggest spike since 2020

America’s predicament is visible in the “anomaly signals” coming from the global oil market. West Texas Intermediate (WTI) for May delivery closed on April 2 (local time) up 11.41% at $111.54 a barrel. It was the largest one-day jump since April 2020, when oil prices rose amid the spread of COVID-19. On the same day, Brent crude’s front-month June contract settled up 7.91% at $109.03 a barrel. The move flipped the relationship between the two benchmarks: since the outbreak of the war, front-month WTI had traded more than $10 a barrel cheaper than Brent.

The “backwardation” structure—where the front month trades above the next month—also deepened. Reuters reported that “WTI’s May contract traded intraday at about a $15.70-a-barrel premium to the June contract, the largest on record.” In oil futures, “contango” (later-dated contracts priced higher than near-dated ones) is typically the norm, reflecting storage, insurance and financing costs as time to maturity increases.

Such market turmoil is not what the U.S. had intended. Market participants interpret it as a backlash to the fading conviction that “the war could end soon.” Another driver behind the spike is seen in global companies diversifying their supply chains toward WTI on expectations that it will take time for the oil market to normalize.

Cracks in the petrodollar era are also cited as a factor threatening U.S. primacy. Iran, which had said it would allow passage only for tankers settling crude payments in yuan, has recently moved to demand a $1-per-barrel transit fee payable in yuan or coins. With China’s clout growing among Middle Eastern producers—and roughly 20% of crude-trade payments already moving away from dollar settlement—Iran’s shift is seen as a direct blow to the petrodollar, analysts say.

◇A replay of the humiliation from 70 years ago?

Many scholars cite “economic pressure” as the direct cause of the Suez moment. Egypt’s closure of the canal sent shipping freight rates soaring and transmitted shockwaves through the global economy. Disillusioned by Britain’s unilateral military action, the U.S. blocked International Monetary Fund (IMF) support for the UK and France. Investors anticipating Britain’s defeat pulled funds from London markets, and the pound plunged, shaking its reserve-currency status.

In this war, the U.S. also initially showcased overwhelming air power, intelligence capabilities and early operational strength, but fractures with allies have surfaced. U.S. President Donald Trump is seeking an “exit strategy” without resolving the Strait of Hormuz problem. Fawaz Gerges, a professor at the London School of Economics (LSE), predicted that “once the aftereffects of the Middle East war subside, the already ongoing move toward a more multipolar global power structure will accelerate further.”

Markets appear to be betting that the Middle East war will be prolonged. Rebecca Babin, a senior energy trader at CIBC Private Wealth, told The Wall Street Journal (WSJ) that “the Middle East situation seems more likely to drift toward further escalation than de-escalation.”

Still, some argue the oil-price surge may prove short-lived. One futures trader said that losses on short positions built on ceasefire expectations may have widened, triggering large-scale “short squeezes” as traders bought futures to cover and close positions.

Washington=Lee Sang-eun, correspondent / Hwang Jeong-su / Kim Dong-hyun, reporters selee@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.