Rocket Lab Extends Reach Into Satellites as Countdown to Profitability Begins

Summary

- Rocket Lab shares rose 27.4% over the past month and surged 365% over the past year, while South Korean investors were net buyers of $64.5 million this month.

- Rocket Lab is expanding its dominance in the small-rocket market with Electron and is strengthening its satellite manufacturing capabilities and European expansion through the Mynaric acquisition.

- Wall Street expects Rocket Lab to turn profitable next year if development of Neutron succeeds and revenue expands, while Stifel raised its price target to $105 and many brokerages maintain buy ratings.

Forecast Trend Report by Period

Hot Pick! Overseas Stocks

Rocket Lab Shares Rise 27% in a Month

Mynaric Deal Bolsters Satellite Capabilities

South Korean Investors Buy $64.5 Million This Month

Stifel Raises Price Target to $105

Neutron Emerges as Falcon 9 Challenger

Its Success May Decide When Losses End

Rocket Lab shares are regaining momentum as space and defense companies draw renewed investor attention following talk of a SpaceX listing and launch activity by Blue Origin. The company is expanding beyond launch services into satellite manufacturing, recasting itself as a broader space platform provider. If it completes development of its next-generation Neutron rocket, its position in the private space market could strengthen further. Investors are also watching for a turn to profitability, which could drive a faster increase in the company’s valuation.

Dominating the Small-Launch Market

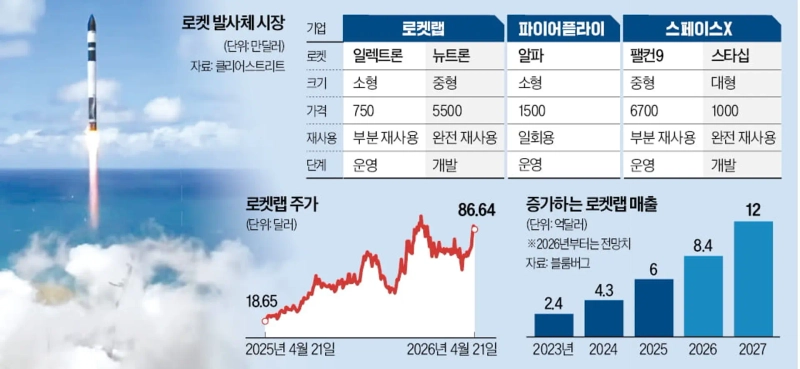

As of April 21, Rocket Lab shares had climbed 27.4% over the past month on the Nasdaq market. The stock has surged 365% over the past year, though this year’s gains had slowed enough for some investors to view the shares as entering a correction. The stock, which fell into the $60 range earlier this year, was recently trading in the $86 range as signs of a rebound emerged.

Interest from South Korean investors is also growing. According to Seibro, the Korea Securities Depository’s securities information service, domestic investors were net buyers of $64.5 million of Rocket Lab shares this month. That ranked eighth among overseas stocks by net purchases.

Rocket Lab has maintained a stable business built around its Electron small launch vehicle. Over the past several years, most rivals in the small-launch market have seen their businesses weaken. UK satellite launch company Virgin Orbit filed for bankruptcy in 2023, while Astra went private.

Rocket Lab is expanding its dominance in the small-launch market. Clear Street described the company as effectively the only operator with meaningful scale in the segment. Launch activity has also continued to increase. Rocket Lab completed 21 launches last year, the highest annual total in its history. Through March this year, it had already carried out at least six successful launches, putting it on pace to surpass that record.

Its vertically integrated model, spanning satellite manufacturing, communications and launches, is another factor supporting the stock. This month, Rocket Lab acquired German optical communications company Mynaric for $155.3 million. Investors welcomed the deal because it gives Rocket Lab high-capacity data transmission technology needed for projects run by the US Space Development Agency. The company also plans to use the acquisition to strengthen its satellite manufacturing capabilities and expand into Europe.

Can It Turn a Profit?

The challenge is that Rocket Lab remains unprofitable. The company posted a net loss of $198.2 million last year. In the first quarter of this year, it is projected to report an adjusted EBITDA loss of $21 million to $27 million. Wall Street expects Rocket Lab to turn profitable next year.

The key variable is whether development of the mid-size Neutron rocket succeeds. Neutron is a reusable medium-lift rocket viewed as a rival to SpaceX’s Falcon 9. Its launch cost is estimated at about $55 million, below Falcon 9’s roughly $67 million. The average selling price per launch is five to six times higher than for Electron, the company’s small rocket. Some analysts estimate Neutron could generate $928 million in annual revenue by 2030 if Rocket Lab launches it 16 times a year.

Neutron’s first launch had originally been scheduled for the first quarter of this year, but was pushed back to the fourth quarter. The delay is viewed as less risky because it stemmed from manufacturing-process issues rather than a design flaw.

Financial performance has continued to improve. Revenue rose to a record $602 million last year. Backlog increased 73% to $1.85 billion, and 37% of that total is set to be recognized as revenue within a year. Brokerages have responded by raising price targets. Stifel this month increased its target price on Rocket Lab to $105 from $90. According to Bloomberg, 12 of the 17 firms covering Rocket Lab rate the stock a buy, while five recommend holding it.

Han Myung-hyun, Hankyung.com reporter, wise@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.