"Real estate has swallowed the economy"…Housing-cost-driven global shock [Global Money X-Files]

Summary

- It reported that rising house prices and housing costs in major countries are weakening household purchasing power and leading to a slowdown in consumption.

- Despite high interest rates and supply shortages, real estate prices have not fallen, making the entry barrier for first-time homebuyers extremely high.

- It pointed out that Korea's household debt and ratio of house prices to income have reached record levels, burdening the economic and investment environment.

Recently, housing costs have been having an increasing impact on national economies worldwide. In the past, real estate was seen as a byproduct of economic growth or a variable dependent on interest rates. However, since the mid-2020s, there is analysis that real estate has become an independent macroeconomic variable that shakes wages, prices, and the political landscape.

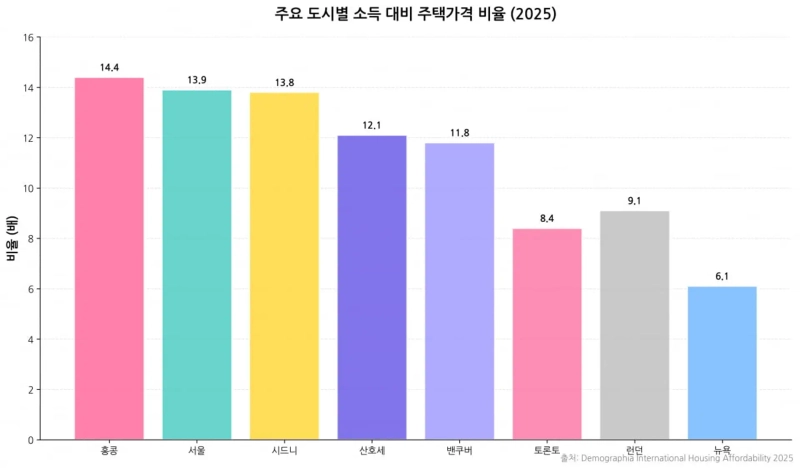

Zero cities with 'affordable' housing prices

On the 18th, the "Demographia International Housing Affordability Survey 2025" reported that among 95 major markets surveyed, as of last year's third quarter there was not a single city evaluated as having 'affordable' housing prices. Hong Kong recorded a ratio of house prices to median income of 14.4 times, maintaining its position as the world's least affordable city to buy a home.

Sydney (13.8 times), Vancouver (11.8 times), and San Jose (12.1 times) followed. This means a median-income household in those cities would have to save for 12–14 years without spending a penny to buy a house. Statistically, it has become impossible to climb the asset ladder through labor income alone.

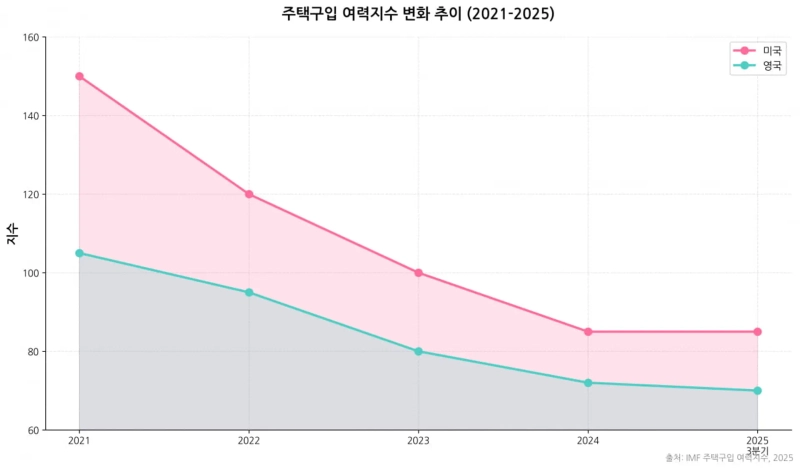

Other surveys also show globally unaffordable housing price increases. According to the IMF's "Housing Affordability Index" data analyzing 40 countries, the U.S. housing affordability index fell from about 150 in 2021 to the mid-80s in mid-last year.

The U.K. likewise plunged from 105 to the low 70s over the same period. This is a lower overall housing purchasing power than in the pre-2007–2008 global financial crisis bubble period. It means the purchasing power of the middle class accumulated over the past decade has evaporated in three years.

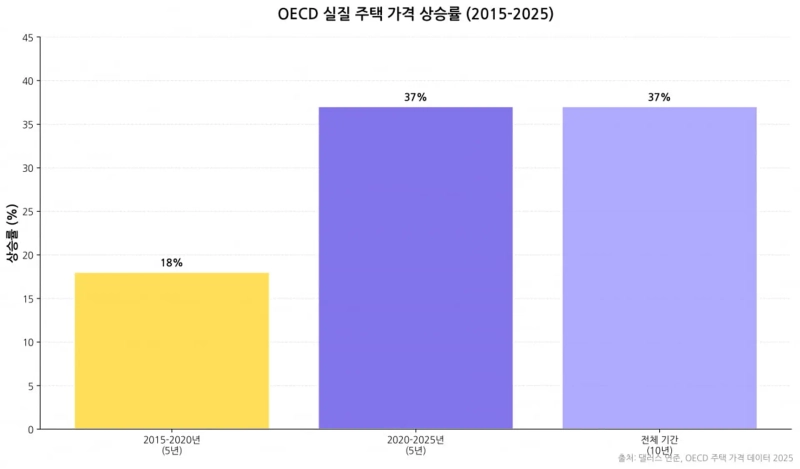

What is the direct cause? Long-term time-series analyses by the IMF and the OECD show that real house prices in OECD member countries rose 37% over the past 10 years through 2025. By contrast, the ratio of house prices to income rose by an average of 16%. It can be interpreted that the massive liquidity supplied worldwide during the pandemic flowed into asset markets, especially real estate.

Deniz Igan, a senior economist at the IMF, wrote in a "Finance and Development" piece that "housing shortages and strong household formation demand offset high borrowing costs," and "the pandemic and its aftermath have caused the worst housing affordability crisis in a decade, and this is provoking broad social anger beyond a mere economic problem."

The cause of sticky inflation

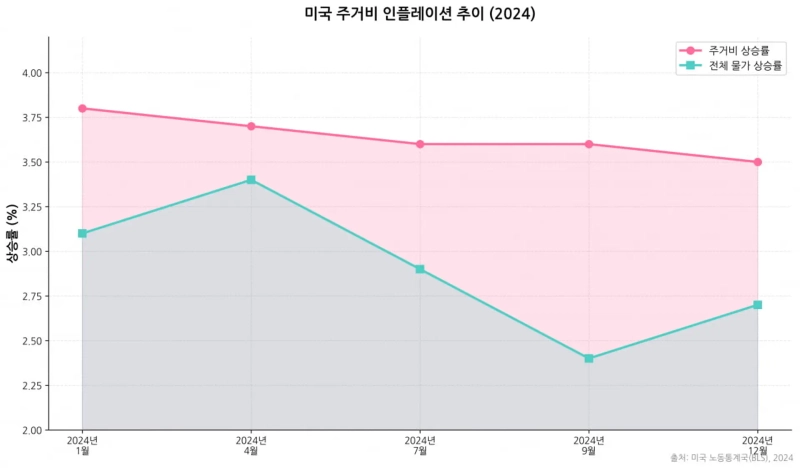

One macroeconomic feature this year is cited as the "stickiness" of inflation. Volatile items like energy and food prices have returned to stability. But the main reason the consumer price index (CPI) is not easily falling to central banks' 2% target is housing costs.

According to the U.S. Bureau of Labor Statistics (BLS), as of last September the housing component of the CPI rose 3.6% year on year, outpacing the overall inflation rate. Housing accounts for more than about 30% of the overall price basket. Once it rises, analysts say it is hard to bring down due to downward rigidity.

There is also a statistical lag. An analytical model from the Federal Reserve Bank of Minneapolis shows that changes in market rents take about 12–18 months to be reflected in the official CPI. There are analyses showing it can be more than 18 months. In other words, last year's rent increases are belatedly pushing up price indicators at the end of 2025.

Steven Myron, a Fed official, recently said, "Housing cost inflation reflects imbalances from two to four years ago more than current supply and demand," adding, "we should be looking at 2027, not 2022, when setting policy." He warned that if central banks maintain excessive tightening based on past data, it could trigger a real economic downturn.

Some point to structural causes combining the so-called 'legacy of liquidity' and 'supply chain disruptions.' The usual rule that higher interest rates should reduce house prices by increasing borrowing costs has been broken. The 'lock-in effect' is also distorting the market. Homeowners who obtained mortgages at past rates in the low 3% range are refusing to move and pulling listings off the market in a high-rate environment, and this supply shortage is defending prices from falling.

According to Freddie Mac, as of the 11th the U.S. 30-year fixed mortgage rate stood at 6.22%. Although slightly down from the 2023 peak, it is still about twice the pre-pandemic level. The National Association of Realtors (NAR) reported that existing home inventory in October was 1.52 million units, up 10.9% year on year.

However, that is only about 4.4 months of supply, falling short of the normal market equilibrium of 6 months. Even if rates go down, local supply shortages and already elevated house prices mean first-time homebuyers still face high entry barriers.

Households strained by housing costs

Rising housing costs affect the entire industrial ecosystem. In particular, analysts point to a pronounced 'crowding out' effect in the consumer goods sector. Soaring housing costs are sucking up households' disposable income and suppressing other consumption. The OECD defines housing cost overburden as 'exceeding 40% of disposable income.' A significant portion of young people in major cities in advanced economies now exceed this threshold.

According to real estate platform Zillow, the U.S. average rent as of November 30 was 1925 dollars, up 2.2% year on year. As 'rent-poor' households tighten their belts, domestic consumer industries such as retail, dining out, and travel are taking a direct hit. Raphael Bostic, president of the Federal Reserve Bank of Atlanta, said, "Core price levels have risen about 20% over the past five years," adding, "this is inflicting severe pain on low- and middle-income households."

Interpretations differ on the economic effects of rising housing costs. Some argue that rising house prices still stimulate consumption through a 'wealth effect' for homeowners. They say this preserves retirement funds for older homeowners and that silver consumption based on that supports the economy.

Critical economists, on the other hand, argue that "the housing bubble is crowding out productive investment." They claim bank lending is focused on buying and selling existing real estate assets rather than corporate capital expenditure or R&D, eroding the productivity of the overall economy.

A Princeton University study pointed out that "rising house prices create a wealth effect for homeowners, but for the unhoused (renters) they are a decisive factor leading to decisions to forgo childbirth, which ultimately lowers the potential growth rate of society as a whole."

In Korea, housing costs are identified as the most vulnerable link. Household debt, a unique private financial system centered on the jeonse (key-money deposit) system, extreme concentration in the Seoul metropolitan area, and one of the world's lowest fertility rates have combined to form an unprecedented complex crisis.

According to the Ministry of Land, Infrastructure and Transport's "2024 Housing Survey," as of 2023 Seoul's ratio of house prices to income was 13.9 times. This means one would have to save for 13.9 years without spending a penny to buy a house. By the Demographia report's standard, this level is on par with Hong Kong (14.4 times) and Sydney (13.8 times). Seoul has become a city where it is harder to buy a house than London (9.1 times) or New York.

Housing price increases have also raised household debt. The Bank of Korea reports that household debt reached 1,952.8 trillion won as of the end of June, setting a record high. The IMF noted in its 2025 Article IV report on Korea that "Korea's household debt stands at 92.6% of GDP, and the high share of variable-rate debt is exacerbating the downturn in consumption."

Joo-wan Kim kjwan@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.