Summary

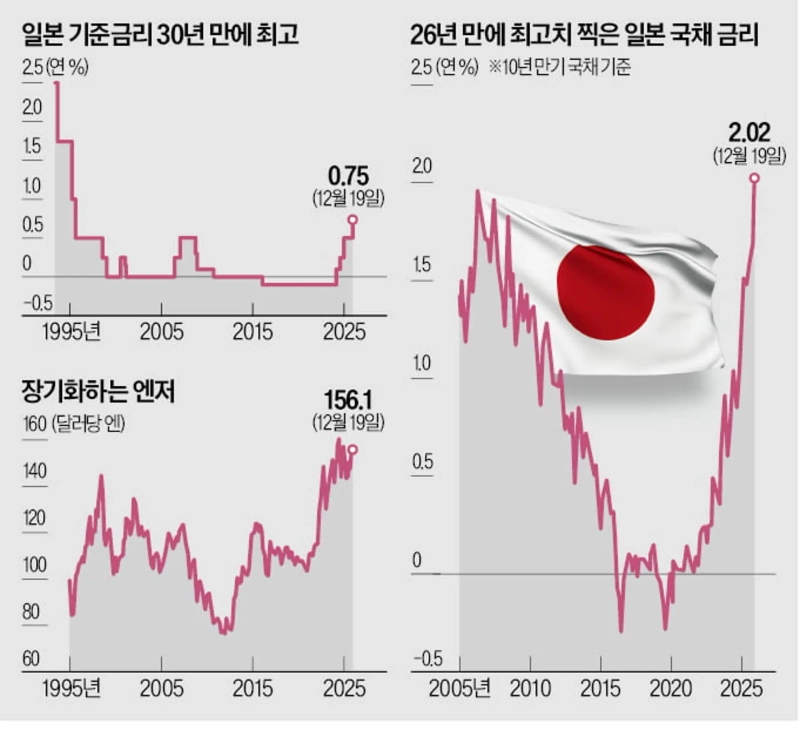

- The Bank of Japan raised its policy rate to an annual 0.75%, pushing Japan's 10-year government bond yields into the 2% range.

- Pressure from a weak yen persists, with the dollar-yen rate exceeding 156 per dollar, maintaining yen weakness.

- BOJ Governor Kazuo Ueda signaled he intends to maintain an upward bias on policy rates into next year.

BOJ raises policy rate to an annual 0.75% for the first time in 11 months

Concerns about fiscal deterioration add pressure

10-year government bond yields rise to the 2% range

Despite Ueda hinting at further hikes,

yen exceeds 156 per dollar

Markets on alert for possible 'yen carry' liquidations

The yield on Japan's 10-year government bond rose to 2.02% on the 19th, the highest level in 26 years since 1999. With growing concerns about fiscal deterioration under the Sanae Takaichi administration, which favors expansionary fiscal policy, and the Bank of Japan raising its policy rate to an annual 0.75% that day, the rise in government bond yields (and the fall in bond prices) accelerated. With Japanese interest rates rising, attention is focused on whether the yen carry trade—borrowing yen at low rates to invest in higher-yielding assets—will be liquidated.

◇"Limited impact on stock markets"

When the BOJ surprised markets with a rate hike in July last year, concerns about a U.S. economic slowdown led to large-scale liquidations of yen carry trade funds and global financial markets fell into panic. On August 5 of that year, Japan's Nikkei plunged 12.4%, recording its largest-ever one-day drop, and the KOSPI also fell 8.77%.

However, on the day the BOJ raised its policy rate to the highest level in 30 years, the Nikkei rose 1.03% from the previous day. The KOSPI also gained 0.65%. The BOJ's rate hike had already been priced into markets, and the yen's weakness—trading around 156 per dollar—also contributed to the rise in Japanese stocks.

Seung-won Kang, a researcher at NH Investment & Securities, noted, "Last year, just before yen carry trade liquidations, yen short positions (betting on a weak yen) were near historic highs, but now the situation is rather yen long (betting on a strong yen)," suggesting that concerns about yen carry trade liquidations are overblown.

◇Prolonged weak yen

The key issue is the weak yen. Despite the rate hike that day, the dollar-yen rate exceeded 156 per dollar. In the foreign exchange market, the conventional wisdom that "narrowing U.S.-Japan interest rate differentials = yen appreciation" does not seem to hold. Although the rate gap between the U.S. and Japan has narrowed to its smallest level in about three years due to U.S. rate cuts and Japanese rate hikes this year, the dollar-yen rate is almost unchanged from the start of the year.

One reason is that real interest rates adjusted for Japanese inflation remain negative. Structural factors also play a role. Japan's trade balance has recorded deficits for four consecutive years through last year, and this year it posted a deficit of 1.5 trillion yen through October. The fact that most import payments must be made in dollars puts pressure on the yen.

Retail investors' overseas investments through the Nippon Individual Savings Account (NISA) are also increasing selling pressure on the yen. There are views that fiscal expansion under the Takaichi administration could undermine confidence in the yen. Even if fiscal spending spurs economic growth, there is typically a one- to two-year lag, during which downward pressure on the yen could persist.

If the BOJ aggressively raises its policy rate next year to curb the weak yen, the possibility of yen carry trade liquidations could resurface. Last year, the Bank of Korea estimated the total yen carry trade balance at 506.6 trillion yen, with funds at high risk of liquidation amounting to 32.7 trillion yen.

◇"More hikes next year"

BOJ Governor Kazuo Ueda said at a press conference that "we will continue to adjust the degree of monetary easing depending on economic, price, and financial conditions." He added that "real interest rates adjusted for inflation are still extremely low in some areas," indicating his intention to maintain an upward bias in rates beyond next year.

On the "neutral rate"—a level that neither stimulates nor restrains the economy—Governor Ueda said, "estimates vary considerably" and that it is "difficult to specify in advance." He did note, however, that the current policy rate level is "still somewhat below the estimated lower bound of the neutral rate," suggesting room for further rate increases. Regarding the impact of the weak yen on inflation, he said, "several Policy Board members have recently pointed out the possibility that the yen's weakness could affect prices." On the sharp rise in government bond yields, he said he "would refrain from detailed comments on short-term movements," but emphasized that the BOJ would "act flexibly and, if necessary, conduct operations (open market operations)."

Tokyo=Kim Il-gyu, correspondent black0419@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.