PiCK

"It hit a record high 37 times, and again?"…Why retail investors are 'excited' [Bin Nan-sae's Flawlessly Wall Street]

Summary

- Wall Street firms including Goldman Sachs highlighted five 2026 investment themes such as AI and copper, and emphasized reducing US exposure and the importance of regional and sector diversification.

- Wall Street said that under a dovish Fed next year, cyclical stocks and commodities — especially copper — could structurally benefit.

- Given concentration risk and high valuations in the US market, diversification into non-US assets such as Europe, along with managing persistent inflation and an AI bubble risk, will be key.

"AI and the US alone aren't enough"…Five investment points for 2026

Investment themes picked by Goldman Sachs

① AI, the end of the opening act

② Inflation < Growth

③ Copper, the new gold

④ Diversify investments outside the US

⑤ Europe approaching an inflection point

The AI tech-stock correction triggered by Oracle and Broadcom, the US federal government shutdown delaying the release of employment and inflation data, the Bank of Japan's rate hikes, and the largest options expiry in history — after a tumultuous week, the US stock market is rekindling hopes for a year-end rally.

On Wall Street, there is disagreement over whether the US market can set new record highs again in the remaining seven trading days or whether Santa has already come and gone. This year the S&P 500 set new record highs a total of 37 times. The most recent record was 6901 (closing basis) on the 11th. Yardeni Research, which had projected a year-end S&P 500 target of 7000 from the start of the year, said, "Considering the rotation where money is moving out of the Magnificent 7 into other sectors, this year's high may end at 6901."

Of course, there are many voices expecting further gains through year-end. Scott Lubner, head of equities & derivatives strategy at Citadel Securities, said, "Since 1928 the S&P 500 has risen in late December with a 75% probability, and the average return was 1.3%," adding, "Viewed in two-week segments, this is historically one of the periods with the highest rates of increase."

Even if short-term outlooks diverge, Wall Street's view of the US market for 2026 is overwhelmingly optimistic. The story is that the bull market will continue for a fourth consecutive year. However, forecasts for the magnitude of gains vary widely by house. Bank of America sees 7100 by next year-end, JPMorgan 7500, Goldman Sachs 7600, Deutsche Bank 8000, and Oppenheimer 8100.

Against this backdrop, Mark Wilson, head of Goldman Sachs' equities franchise, summarized five key investment themes to watch in 2026. Other major Wall Street houses largely share similar views. The key point is that investors should not just increase exposure to US and AI stocks indiscriminately, but must pick winners and diversify by region, asset class, and sector.

① The 'mindless AI rally' phase is over

The first theme is that the second act of the AI trade has begun. Wilson of Goldman Sachs says we are moving beyond the 'buy anything AI' phase where everything rose simply because it was tied to AI.

This does not mean AI is a bubble or that the AI story is over. While bubble elements exist, Wall Street's consensus is that it's too early to worry about a full bubble collapse. Given that AI is seen as a modern space race and a frontline of geopolitical competition, private investment in AI and government policy support are likely to expand next year.

But the early phase where the AI theme and hype alone drove gains is ending; investors now must select companies that will actually generate revenue and profits and structurally benefit from AI. Debates about AI overinvestment, funding, and profitability — central to bubble concerns — will continue. Conversely, companies that pass stricter scrutiny by more discerning investors may have greater upside.

That is why Wilson stresses, "Now is the best time to dollar-cost into long-term innovation." Short-term volatility will continue, but it is an effective strategy to steadily dollar-cost into technology and innovation companies with structural growth drivers from a long-term perspective. "If building data centers in space — once sci-fi not long ago — is the kind of innovation that could be realized by today's large-scale AI investment, then now is the time."

Wilson identifies structural AI winners as companies in semiconductors and computing hardware, data centers, power — the infrastructure enabling AI development — and firms that successfully incorporate AI into their businesses to drive real productivity gains.

Mag 7 concentration eases

In this context, Wall Street commonly expects the dominance of the Magnificent Seven (Mag 7), which drove gains in recent years, to weaken next year. More precisely, the flow of funds that concentrated only in large tech stocks may change.

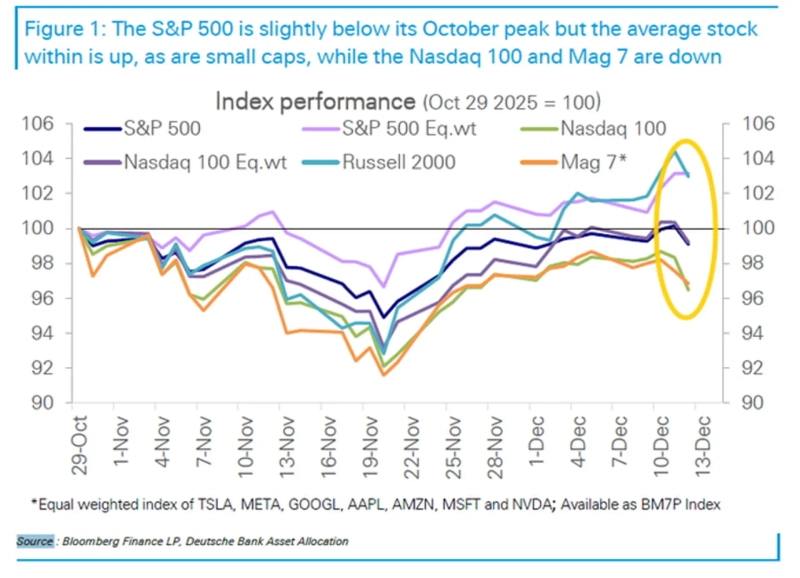

According to Deutsche Bank, since November the S&P 500 equal-weighted index and the small-cap Russell 2000 have outperformed the market-cap-weighted S&P 500, the Mag 7, and the Nasdaq 100. Even within the Mag 7 and large tech firms, investors' judgments on AI competitiveness diverge, and investors have rapidly taken profits in companies they feel are excessively overvalued.

This doesn't mean Mag 7 stocks will necessarily underperform. As companies leading innovation in the AI era, unless an AI bubble bursts or a bear market arrives, investor preference for Mag 7 is unlikely to vanish overnight. But whereas Mag 7-centric tech stocks have almost monopolized gains so far, the rally is more likely to spread to other sectors, according to Wall Street. That would reduce concentration risk in the US market and could lead to a healthier rally.

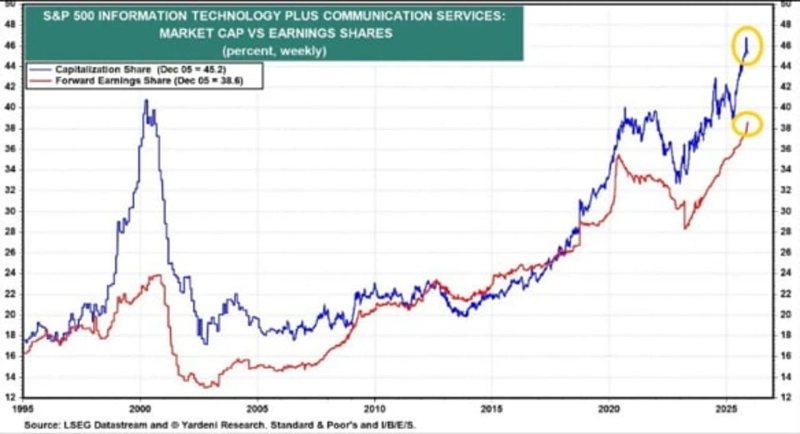

Earlier this month Yardeni Research downgraded its stance on the Mag 7 and the S&P 500 IT & communication services sectors from 'overweight' to 'neutral,' saying, "These two segments account for a record-high 45.2% by market cap and 38.6% by forward P/E within the S&P 500," and "As concentration has increased, risk-adjusted reward has fallen, so there is no incentive to increase weight further."

They are not advocating selling tech stocks, but rather that new investments are better allocated to undervalued sectors. Wall Street is increasingly recommending overweight positions in financials, industrials, and healthcare — sectors that are relatively undervalued (healthcare) or stand to benefit from Trump administration fiscal expansion, manufacturing investment incentives, and US central bank rate cuts (financials and industrials).

② A dovish Fed and the 'reflation' trade

Second, Wall Street expects next year's Fed policy to be more dovish, prioritizing growth and preventing labor market slowdown over strictly controlling inflation. Consequently, many forecast relative weakness in the dollar.

Wilson of Goldman Sachs sees Kevin Hassett, chair of the White House Council of Economic Advisers and a close aide to President Trump, as the most likely candidate to become Fed chair in May next year. He predicts the Fed will cut rates twice in the first half of next year. In line with the Trump administration, the Fed may pursue policies that support nominal growth even if inflation rises somewhat — effectively "running it hot."

Goldman Sachs expects US growth next year of 2.8%, above the Bloomberg consensus of 2.5%. They conclude that a combination of lower tariff burdens, tax cuts, and easier financial conditions could accelerate growth.

As a result, a reflation trade — where accommodative monetary policy and fiscal stimulus combine to push up growth and prices — is already underway. Cyclicals such as financials, industrials, energy, and consumer discretionary have outperformed defensive stocks. Precious metals and commodities like gold, silver, and copper have strengthened as many investors anticipate higher inflation and a weaker dollar.

③ Copper, the new gold

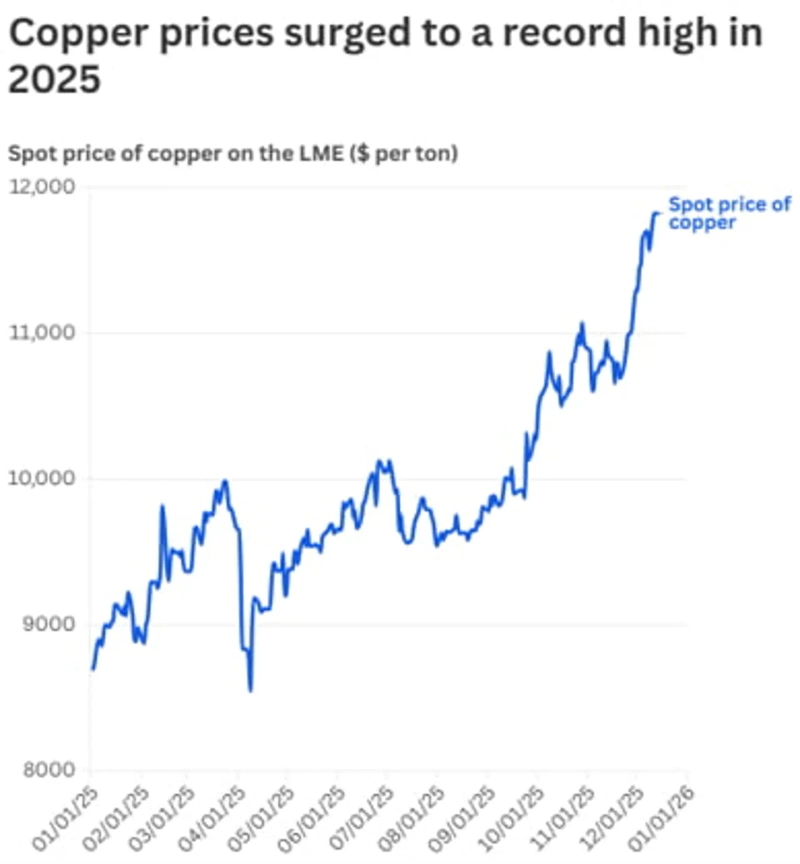

Wilson at Goldman Sachs is particularly bullish on copper within the commodity rally. With AI investment expanding, copper is being revalued not just as a cyclical commodity but as an essential resource for AI infrastructure — for power grids, cooling infrastructure, and more. Wilson says 60% of the incremental copper demand through 2030 is expected to come from global power infrastructure investment.

Fears that the US could impose tariffs on refined copper imports from 2027 have further prompted recent stockpiling of copper. Copper inventories have been depleted and prices have risen. The London Metal Exchange (LME) copper spot price has climbed nearly 40% year-to-date and about 10% in the last month alone.

Despite this, limited new mines and cautious development by mining companies constrain supply elasticity, supporting bullish copper forecasts. Citi recently raised its early-next-year copper price forecast to $13,000–$15,000 per ton. However, commodities are highly volatile and there is caution over possible short-term overheating.

④ Diversification outside the US is essential

A recurring point in Wall Street's outlook reports is 'global rebalancing.' Given structural dollar weakness and the relatively high valuations of the US market after three years of a bull market, diversifying portfolios into non-US regions is expected to be an essential investment theme next year.

Wilson says, "The valuation of the US equity market relative to other global markets is at a 25-year high and index concentration is extremely high," adding, "It is becoming increasingly difficult for the US market to sustain excess returns." He noted that this year the UK and French markets have outperformed the Nasdaq in dollar terms.

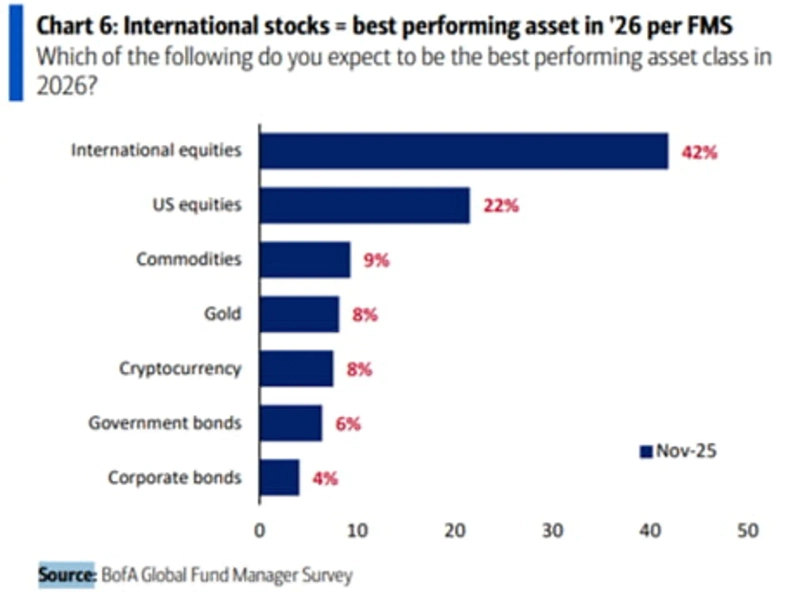

Wall Street generally expects this trend to continue next year. According to Bank of America's global fund manager survey, non-US equities (42%) were picked as the asset likely to perform best next year, with US equities at 22% in second place. A year earlier, US equities, Russell 2000, and the US dollar were the top picks. Bank of America strategist Hartnett said the 'global rebalancing' theme has overtaken 'US exceptionalism' because US trade, industrial, and foreign policies have prompted fiscal stimulus in other countries such as China (demand stimulus), Europe (defense buildup), and Japan (ending deflation and promoting growth).

Goldman Sachs' 10-year outlook projects average annual returns of 6.5% for US equities, 11% for emerging markets including China, and 10% for Asia excluding Japan.

⑤ Pay attention to Europe too

Among regions frequently mentioned for diversification are Korea, China, Japan, and Europe. Wilson at Goldman Sachs says investors should also pay attention to Europe — "don't sleep on European equities." He argues that the eurozone, long mired in bureaucracy and low growth, is finally poised for an inflection point.

His rationale is interesting. He believes the Trump administration's increasingly unilateral stance toward Europe could force Europe into policies that boost growth. The National Security Strategy (NSS) released by the Trump administration on the 4th stated, "The era in which the US sustained the world order as Atlas is over," and set long-term strategies including using tariffs for reshoring, reindustrialization, securing energy dominance, and shifting burdens onto allies. The report criticized Europe's policies on freedom of expression and immigration, bluntly questioning whether European allies can maintain long-term reliability as US partners.

Wilson argues that faced with weaker US security support, tariffs, intensified competition from China, and energy shocks, Europe will be compelled to drive real measures like increased investment and deregulation to achieve economic and strategic self-reliance. Given relatively low valuations in European equities, investors seeking diversification outside the US should not ignore Europe.

Of course, there are many counterarguments to European optimism. Europe lags in AI innovation, and as JPMorgan CEO Jamie Dimon notes, anti-business regulation in Europe, differing national interests within the eurozone, and entrenched bureaucracy are not problems that can be fixed overnight.

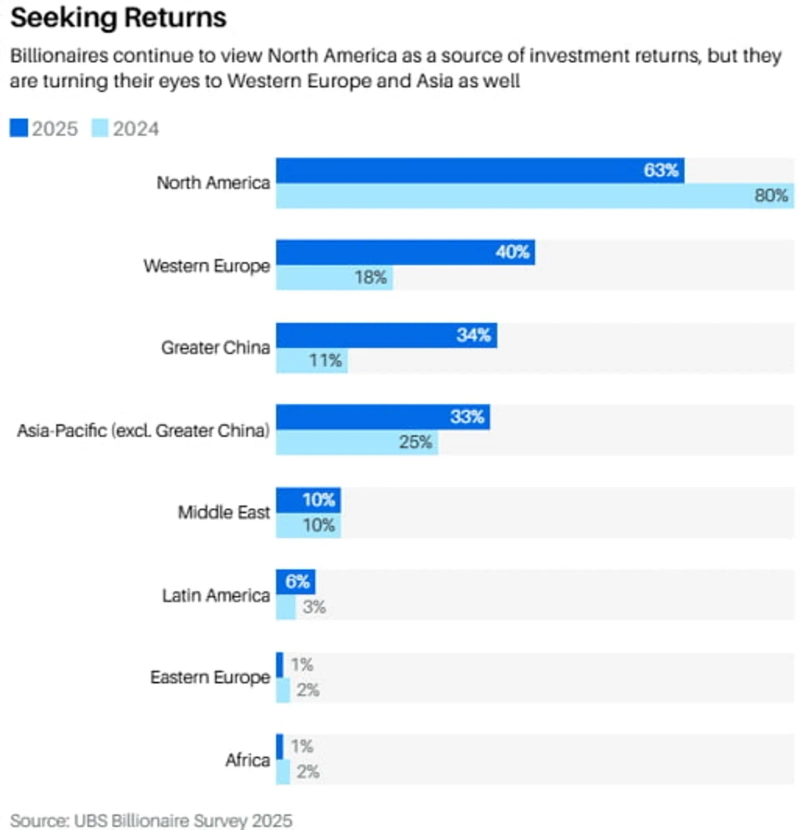

Still, global wealthy individuals' interest in Europe is clearly rising. In a UBS survey of 87 billionaire clients, 63% picked North America (1st) and 40% picked Western Europe (2nd, multiple answers allowed) as the regions expected to deliver the highest returns in the next 12 months. A year earlier, North America was an overwhelming 80% as 1st and Western Europe was 18% as 3rd, indicating growing interest in European equities.

Investment risks in 2026

So what risks should investors watch next year? First, sticky inflation. If reflationary policies keep inflation higher than the Fed's target for an extended period, the Fed's room to cut rates may be narrower than markets expect.

Even if political pressure leads the Fed to cut rates, long-term yields — determined by the bond market rather than short-term policy rates — could remain high. Global fiscal deficits and currency debasement would exacerbate this. Rising long-term rates raise expected returns for equity investors and constrain valuation expansion. Companies without earnings or with weak cash flows could see greater downside risk.

Second, the ongoing debate over an AI bubble. Unlike the 2000 dot-com collapse, today's AI-led companies have earnings growth supporting stock gains, and repeated bubble concerns have led to self-correcting forces that curb speculative investments in unprofitable firms.

Nevertheless, questions remain about some AI companies' funding capacity and the potential fragility of the private credit markets that have financed large AI data-center loans. Each time, AI-related stock volatility could recur around companies with large external financing needs, as happened with Oracle.

Deutsche Bank warned that "AI and power demand, policy and geopolitical shifts, capital costs, and fiscal factors are elements that can, with small changes, completely alter the macroeconomic and market regime," adding, "Next year may be a year in which it is hard to rely on a single scenario. Markets could move much more dramatically up and down due to unforeseen variables, so risk management strategies are more necessary than ever."

New York=Bin Nan-sae, correspondent binthere@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.