U.S. Destroys Trade Norms... 'Trump Round' Looms Over Investors [Global Money X-File]

Summary

- After the U.S. declared the end of the WTO system and began leading a new trade order—the 'Trump Round'—the political risk premium has emerged as a major factor in global asset markets.

- Trade uncertainty and tariffs have resulted in stock market volatility and higher ERP (Equity Risk Premium), a preference for safe assets, and wider corporate credit spreads.

- With the intensification of U.S.-China tensions, the commodities market, especially gold and rare earths, has seen pronounced effects. Global investors have responded with more defensive portfolios and a shift to policy-benefiting sectors.

The Invoice of the 'Trump Round' Era

④ Assetization of 'Political Risk'

With the United States announcing the end of the World Trade Organization (WTO) system, the volatility in asset prices is expected to increase. This is because the U.S. is leading a new trade order, so-called the 'Trump Round.' According to analysts, global investors now need to factor in a 'political risk premium' when constructing their investment portfolios.

'Direct Hit' to Global Asset Markets

According to Reuters on the 15th, USTR Representative Jamieson Greer published an op-ed on the 7th that declared the end of the WTO and the launch of the 'Trump Round.' This officially marked a fundamental paradigm shift in the multilateral trading order that has supported the world economy for about 80 years since WWII. It goes beyond a mere shift in trade policy. Analysts say this is a signal of a seismic shift in the global economic operating system—from 'efficiency' to a focus on 'security and national interests.'

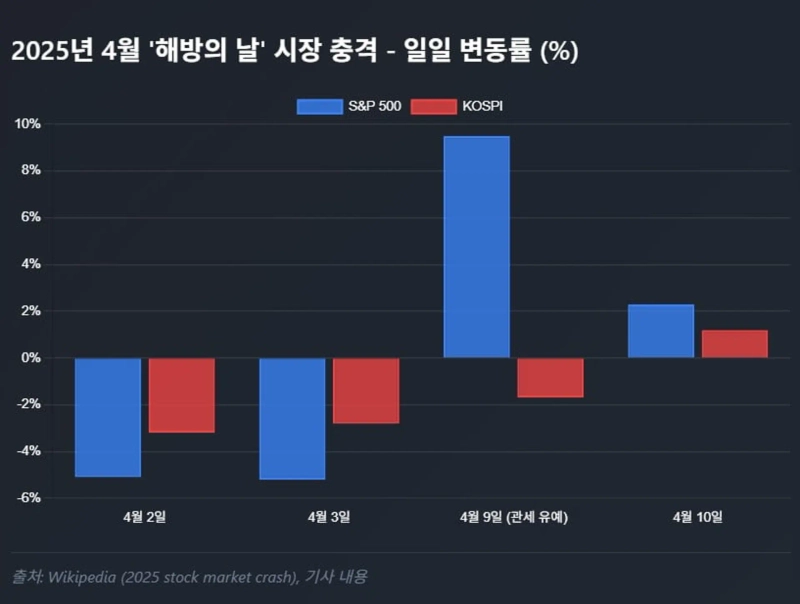

Previously, the 'Trump Round' had already delivered a direct hit to the global asset market. This was starkly revealed during the global stock market crash in early April. When the Trump administration announced sweeping tariffs, over $10 trillion in global market capitalization evaporated almost instantly. Major markets experienced the worst plunge since the COVID-19 outbreak in 2020. The S&P 500 Index nosedived by more than 10% in just two days, its biggest drop since March 2020—comparable to the shocks in the 1987 and 2008 financial crises.

The risk compensation demanded by investors also showed up in government bond yield spreads and currency values. For example, due to the Trump administration's excessive tariff policy, the dollar weakened relative to the interest rate differential in Q2. This was the result of overseas investors avoiding dollar-denominated assets to escape tariff risks.

Although the U.S.-Europe interest differential (2-year basis) widened by 0.4%p since early April, the dollar actually shed over 6%. This means a risk premium was added in the U.S. due to foreign outflows and hedging demand. However, after the dramatic U.S.-EU trade deal at the end of July eased the worst of the tariff war, the trade anxiety premium attached to the dollar partially dissipated. These trends show that global investor sentiment has become much more sensitive to political decisions. The collapse of trade norms and unilateral tariffs have become new risk premiums for global capital markets.

Global Pension Funds Also Adjust Portfolios

Amid unprecedented trade uncertainty, major pension funds and sovereign wealth funds around the world are seeking portfolio adjustments. Previously, the National Pension Service of Korea increased its investment in industries with less tariff risk in Q1, ahead of the U.S. tariff announcement. Having sold off most U.S. content and media stocks until last year, it made massive purchases early this year. It acquired 3.58 million shares of Warner Bros. Discovery in Q1, considered a 'safe zone' amid the U.S.-China tariff war. Warner Bros. Discovery operates in movies and OTT content, sectors largely unaffected by tariffs.

Other global investment institutions are also strengthening their defensive portfolio stances. Nicolai Tangen, CEO of the Norwegian Sovereign Wealth Fund, told Reuters, "Nowadays, 'hot wars,' 'cold wars,' 'trade wars,' and 'tech wars' are breaking out simultaneously, with decoupling now the top market risk for the world economy." He warned, "Clashes between superpowers such as the U.S. and China are making growth sluggish and inflation and uncertainty mount—a very negative scenario is becoming a reality." Canada Pension Plan (CPP) and others are also reported to be reassessing investments in regions with geopolitical risk exposure, such as China, or increasing assets related to U.S. infrastructure and reshoring.

The power struggle between the U.S. and China is expected to continue putting pressure on global asset markets. In a recent report, the World Bank estimated that trade fragmentation could reduce emerging market growth rates by 1 percentage point over the next decade. The IMF also expressed concerns that "the global economic system is being reset for the first time in 80 years," raising worries of a drop in potential long-term growth.

In the stock market, high volatility appears inevitable. Each time tariffs or political decisions arise between the U.S. and China, sharp spikes and plummets in stock prices are expected to recur. On April 2, when the U.S. declared reciprocal tariffs on the world, U.S. stocks suffered their biggest drop in two days since March 2020. Days later, with news of some tariff delays, there was a 9.5% surge in a single day—echoing the wild swings of the financial crisis era. Going forward, technical rebounds are likely on positive negotiation news, while deep drops will follow worsening tensions.

With the Trump administration brokering deals with the EU and Japan this month, the previously weak dollar has rebounded and stock indices rose in relief rallies. However, critical issues with China remain unresolved. Tariff hikes or supply chain decoupling could be announced at any time. Reuters strategist Peter Apps diagnosed, "Trump's 'trade tsunami' is shaking up geopolitics," and "the U.S. is using tariffs as diplomatic and security tools, trying to line up allies, causing global investment landscapes to shift."

In this environment, investors are rotating into sectors with resilient earnings or likely policy support. In the U.S. market, defense, reshoring manufacturing, and infrastructure-related stocks are expected to show relative strength. In the Korean market, defense and some domestic stocks performed well during the trade dispute phase, attracting foreign and institutional inflows.

Companies Revise Earnings Outlook Down

However, many companies are postponing investment plans, and with sagging trade, greater earnings uncertainty drives up Equity Risk Premium (ERP). ERP refers to the extra return investors require to invest in the stock market over risk-free assets, such as government bonds. For example, in Q3 this year, earnings forecasts for major companies worldwide were significantly downgraded. Despite lower valuations, concerns remain that investor sentiment may not improve quickly, prolonging a low-PER market.

Gilles Moëc, Chief Economist at AXA Group in the U.S., commented, "Even amid political headwinds, Trump is driving the trade war to U.S. advantage," and noted that U.S. company profits are being protected at opponents’ expense. This could lead to weak stock performance in export-dependent economies like Korea and relatively strong performance for U.S. domestic stocks.

Preference for safe assets and spreading of credit risks will likely occur simultaneously. If global trade worries intensify, investors may flock to safe-haven assets such as U.S. or German government bonds, putting downward pressure on interest rates (raising bond prices). On the other hand, import price increases and inflationary pressure from tariffs could restrain central bank policies, putting upward pressure on long-term rates. The trade dispute could drive short-term rates lower on recession fears, while inflation risk pushes long-term rates higher—a so-called 'yield curve flattening/inversion.' Fed Chair Jerome Powell warned last April, "Uncertainty has become unusually high due to tariffs and industrial policies, which could stoke inflation while slowing growth."

In the credit bond markets, corporate spread widening is inevitable. This refers to the spread between corporate bond yields and government bond (or risk-free asset) yields expanding as companies raise funds. Manufacturers squeezed by tariff-induced cost pressures and companies in highly trade-dependent countries are facing extra risk premiums, further widening their credit spreads. So far, global credit markets remain relatively stable: investment grade bond spreads have only expanded moderately. However, if the trade war spills over into a currency war or financial retaliation, global dollar liquidity could tighten and credit lines could be blocked.

Commodity Markets Also Affected

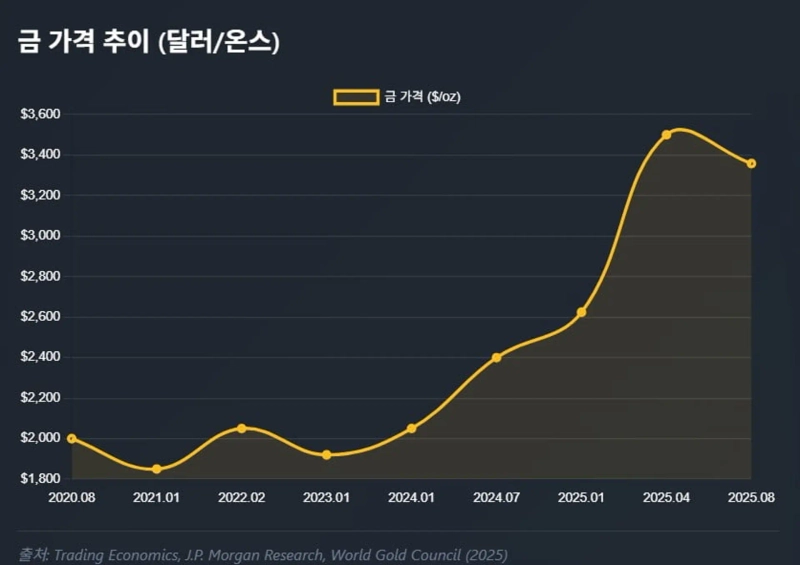

Trade conflict is expected to have diverging effects on commodity markets. Oil and other energy prices are closely linked to geopolitical risk. If global growth slows further due to worsening U.S.-China tensions, declining oil demand could place downward pressure on prices. Industrial metals are also expected to weaken, with demand reduced by trade slowdown and a slowing Chinese economy. However, if China retaliates against U.S. tariffs by restricting rare earth exports, certain commodity prices could soar.

Gold prices have climbed to all-time highs in recent months. Each time U.S.-China tensions escalate, gold is highlighted as a traditional safe haven. Central banks around the world have also shown a structural buying trend, increasing gold allocations at the expense of dollar reserves.

Ray Dalio, Chairman of Bridgewater Associates, warned, "Right now, we are at an extremely critical crossroads, and a situation much worse than a recession could arise." He analyzed that "tariffs are like throwing rocks into the production system," with trade conflict, debt, and hegemonic rivalry all causing a major shift in the global economic order.

[Global Money X-File highlights important but little-known patterns in the world’s money flows. For your convenience, subscribe to the reporter's page for essential global economic news.]

Reporter: Kim Joo-wan kjwan@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.