Jackson Hole Meeting from the 21st… How Will Fed’s Monetary Policy Change? [Hansang Chun’s International Economy Analysis]

Summary

- It is expected that the upcoming Jackson Hole Meeting, starting on the 21st, will involve in-depth discussions on Fed independence, interest rate policy, and directions for monetary policy.

- The pressure from President Trump and key officials for rate cuts, and the possibility of a policy pivot resumption, could have a significant impact on the market as the Fed’s policy stance changes.

- After this meeting, the likelihood of interest rate changes and a monetary policy shift will rise, making it important for economic agents, including stock investors, to prepare accordingly.

Both Trump and Besant

Shake-Up with "Lower the Interest Rate"

Re-examining Economic Indicators to Reduce the Gap with the Real Economy

Anticipation of Reviewing Indicators

Interest in Possible Pivot Resumption

Bank of Korea Also Needs Consideration

From the 21st, the 'Jackson Hole Meeting' will be held for three days and two nights in Jackson Hole, a small resort town in Wyoming, USA. This year, with the significant variable of 'President Donald Trump', it is expected that many current issues beyond the main topic of ‘labor market structural transformation’ will be on the agenda.

First, it is likely that the discussion will start with how to maintain the independence of the Fed, which has been regarded as vital since its establishment in 1913. This is because President Trump’s surprise visit to the Fed, personnel reshuffles, and requests for lower interest rates have accelerated attempts to shake the Fed’s independence. Even Treasury Secretary Scott Besant is putting pressure to lower rates.

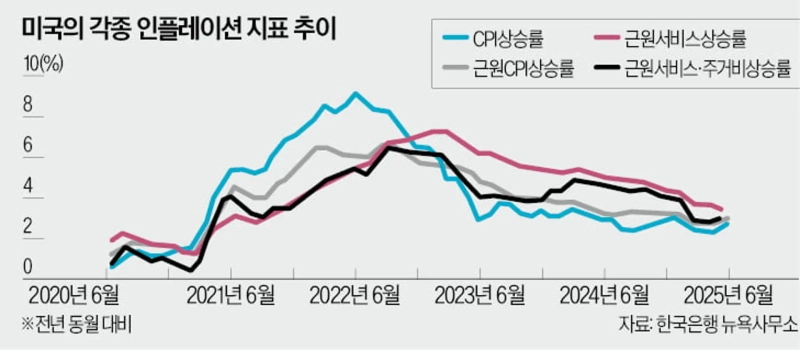

Second is the Fed’s goal reset discussion. The Fed, which has prioritized price stability as its primary goal, added employment creation as a secondary goal in 2012. However, with the weakening of the Phillips relationship between inflation and employment—the foundation of the two mandates—there has been confusion in rate changes. Lately, even trust in employment statistics has fallen due to changes in statistical conditions.

Third, a review of how economic indicators are measured. For monetary policy to be operated based on these indicators, economic data needs to quickly and accurately reflect reality. At the very least, forecast indicators need to accurately reflect trends. The absolute error rate, which is the difference between projections and actual results, should be within 30%. At present, none of these requirements are being met.

Fourth, a key agenda is enhancing the forecasting ability of the Fed’s econometric team (Ferbus). In the era of the 'new abnormal', economic outlooks (SEP) produced by models inevitably have lower predictive power. This is due to the weakened continuity of time-series data, necessitating greater use of dummy variables. Since COVID-19, it is time to consider adopting innovative approaches such as the ‘cube’ method of the Economic Cycle Research Institute (ECRI), known for its accuracy in forecasting.

Fifth, reviewing the usefulness of the dot plot. From Trump’s first term, the politicization of FOMC members has been an ongoing issue, becoming more severe in his second term. If the dot plot, which is intended to communicate members’ free interest rate projections based on knowledge and experience, simply reflects Trump’s preferences, it loses meaning.

Sixth, there may be consideration of abolishing the Average Inflation Targeting (AIT) introduced as a temporary measure. In a transitional period where the main cause of inflation shifts from aggregate demand to aggregate supply, making interest rate adjustments based solely on prices at a single point in time is risky. The AIT was introduced under the belief that using the average inflation rate over a certain period would be safer. Five years have passed since the end of the COVID-19 crisis—it is now time to naturally discuss the abolition of AIT.

Seventh, the benchmark interest rate, which has been under long-term review, is now up for change. This is due to the recurring puzzle surrounding the Federal Funds Rate (FFR) used as the benchmark by the Fed. For example, after reducing the benchmark by 1 percentage point since last September, the 10-year Treasury yield rose by 0.8 percentage points. There is attention on whether the ON RRP, used as a supplementary indicator since 2015, will be adopted as a new benchmark.

Eighth, discussions arising from the passage of the GENIUS Act will also be a main topic. If stablecoins based on DeFi become common, what will happen to Central Bank Digital Currencies (CBDCs)? There will likely be intense debate over whether to abolish or coexist. Decisions may also be made on who takes the seiniorage (profit from currency issuance).

Ninth, there is interest in whether hints will be given for resuming the pivot (monetary policy shift) from the September FOMC. The delayed pivot since last September was halted this year due to clarity issues caused by the Trump administration’s tariffs. At Jackson Hole, participants are expected to engage in heated debates over how to assess tariff impacts and whether to accept Trump’s demands for lower rates.

It is rather the Bank of Korea that may need to contemplate the issues discussed at this year’s Jackson Hole. As many changes, including rate shifts, are expected to follow, economic agents including equity investors should remain vigilant.

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.